Urals crude prices have climbed back to around USD 50 per barrel, well below the price cap level of USD 60. The East Siberia–Pacific Ocean (ESPO) price, mainly applying to Chinese purchases, has recovered from USD 65 to over USD 70.

The rise in Urals prices shows the importance of lowering the price cap to a level that eliminates Kremlin’s excess profits from oil exports, USD 30 per barrel. The fact that reported prices for shipments to China continue to exceed the price cap shows the importance of strengthening the enforcement of the price cap.

The week of 27 March to 2 April 2023, the EU continued at the fourth place as an importer of Russian fossil fuels, with China, Turkey and India making up the top 3 and South Korea at the fifth place.

China’s imports consisted of crude oil, coal, oil products & chemicals and pipeline gas. Turkey imported oil products & chemicals, pipeline gas, coal and crude oil. India imported crude oil and coal. EU imported pipeline oil and gas, LNG and oil products & chemicals. South Korea imported crude oil, coal and LNG.

Two of the top five ports importing Russian fossil fuels were in China, two in India, and one in Turkey. Crude oil dominated as the imported commodity.

The top EU importer countries last week were Slovakia, Belgium, Czech Republic, Malta and Hungary.

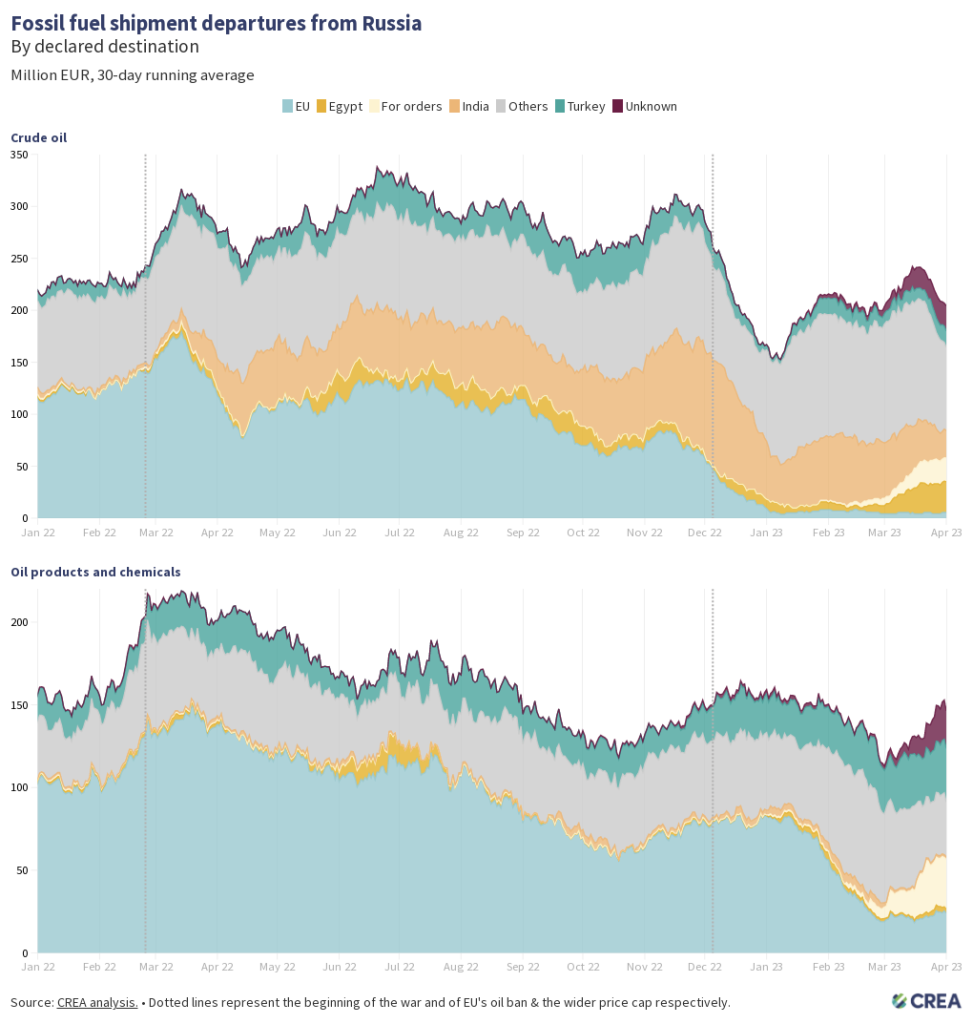

Russia’s revenues from crude oil shipments continued their fall last week after climbing in early March. The revenues from oil products & chemicals rose.

The share of tankers covered by the price cap in crude oil shipments out of Russia was rather stable at close to 60%. For oil products & chemicals, the coverage of the price cap coalition was above 70%. The shares of ownership and insurance of vessels carrying Russian crude and oil products&chemicals within the price cap coalition are much higher for shipments departing from Russia’s Arctic, Baltic and Black sea ports, but much lower for shipments departing from Pacific ports.

The amount of oil products on water showed a short-term drop in the past week, but has been building up since early February. The LNG glut keeps building up. With all of these commodities the share of shipments “for orders” has widened, indicating Russia is struggling to find buyers.

Shipments in the last week

The weekly update of Russian fossil fuel exports was prepared by Meri Pukarinen, Europe-Russia Policy Officer, CREA; and Jan Lietava, Data Scientist/Engineer, CREA.

| Note on methodology: Dates featured are the date the arrival of the shipment was captured by our algorithm. 80% of arrivals for shipments are found within four days of the arrival port call in the specific port. For our oil products and chemicals commodity group, please note this contains a wider range of items than just those specified in the current sanctions, as of 2022‑02‑05. More information at: https://energyandcleanair.org/ |