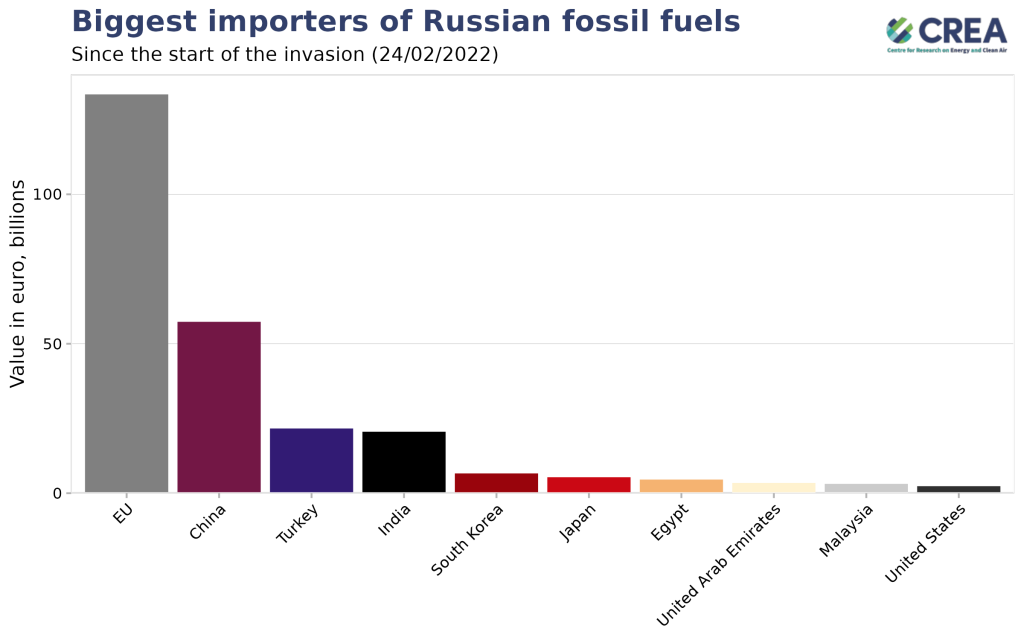

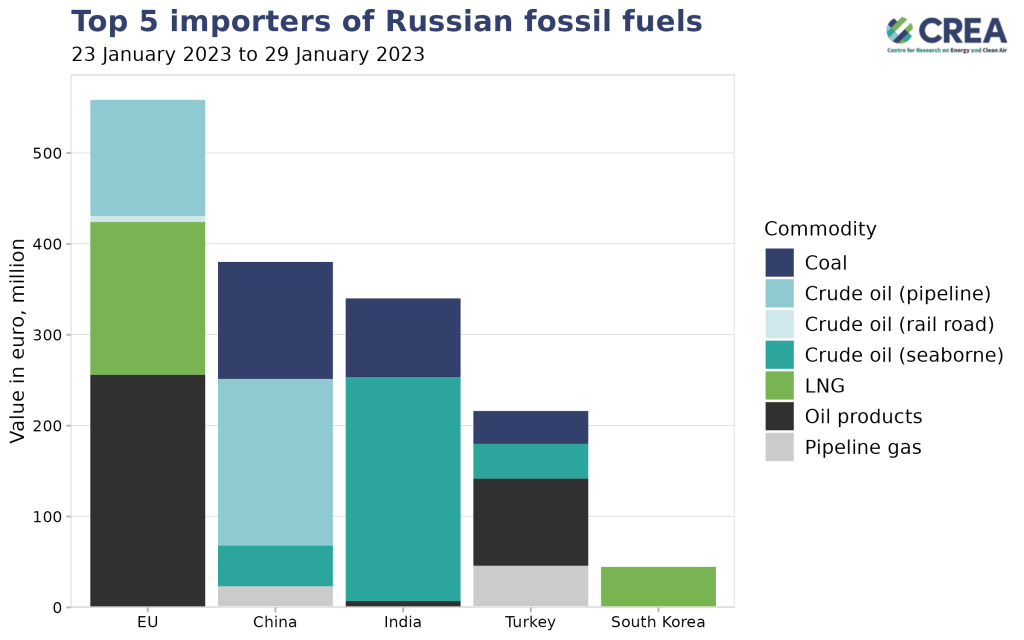

The week of 23 to 29 January 2023, the EU was the largest importer of Russian fossil fuels. The top five other importers were China, India, Turkey and South Korea.

In a change from the past weeks, the EU resumed LNG imports from Russia — shipments had been stranded as EU storages are nearly full and demand has fallen significantly, but in the past two weeks the glut began to be absorbed regardless. Other EU imports were oil products, imports of which are still allowed until 5 February, as well as crude oil via pipeline or rail. China imported a mix of crude oil, coal and pipeline gas. India’s imports consisted of crude oil, coal and oil products. Turkey imported a mix of oil products, pipeline gas, crude oil and coal. South Korea’s imports consisted of LNG.

Three of the the top five ports importing Russian fossil fuels were in Asia, with crude oil and coal as the imported commodities. Two of the top five ports were in Europe, importing LNG.

The top five EU importer countries last week were Spain, Germany, Belgium, the Netherlands and Latvia.

The value of crude oil shipments from Russia rose in the past week, as both volumes and prices rebounded, underlining the urgency of revising down the price cap. The largest increases were in shipments to Egypt and unknown destinations — these could be unsold cargoes still looking for buyers or ships that are not declaring their destination. The value of shipments of oil products stayed rather stable.

The share of tankers covered by the price cap in crude oil shipments out of Russia has still stayed above 60%. For oil products and chemicals, the coverage of the price cap coalition remains high at over 70%. These high shares illustrate the leverage the price cap coalition has to ratchet down the price cap.

Oil-on-water for crude oil is falling across different destinations. Oil products on water have seen a small increase due to shipments “for orders” and to “others”. Despite resumed imports, there remains a glut of tankers loaded with Russian LNG. Urals crude prices were around USD 55 per barrel, having inched closer to the price cap level of USD 60 but remaining below it. However, the East Siberia–Pacific Ocean (ESPO) price, mainly applying to Chinese purchases, has remained above the price cap at USD 75.

Shipments in the last week

The weekly update of Russian fossil fuel exports was prepared by Meri Pukarinen, Europe-Russia Policy Officer, CREA; and Jan Lietava, Data Scientist/Engineer, CREA.