Key findings

- The volume of Russia’s fossil fuel exports fell in September to its lowest monthly level recorded since Russia’s full-scale invasion of Ukraine. However, revenues increased month-on-month for the second month in a row due to rising oil prices and the failure of Ukraine’s allies to revise and enforce the price cap on Russia’s oil exports.

- Russia’s monthly exports of seaborne crude oil fell 3% in volume terms, but revenues rose 10% in September on the prior month.

- According to the Russian Ministry of Finance, September saw a 24% and 34% increase in revenues from the Mineral Extraction Tax and Export Duty, respectively.

- Due to increasing crude oil prices, Russia’s earnings have experienced a monthly growth of 3% in September 2023 compared with August, despite a 5% month-on-month decrease in the volume of Russia’s fossil fuel exports.

- Revenues from seaborne oil products declined in September (-54%), influenced by Russia’s partial and temporary ban on the export of gasoline and diesel to cope with a domestic market shortage.

- The most significant month-on-month increase in the value of Russia’s fossil fuel exports was observed in LNG, which experienced a 48% growth compared to August.

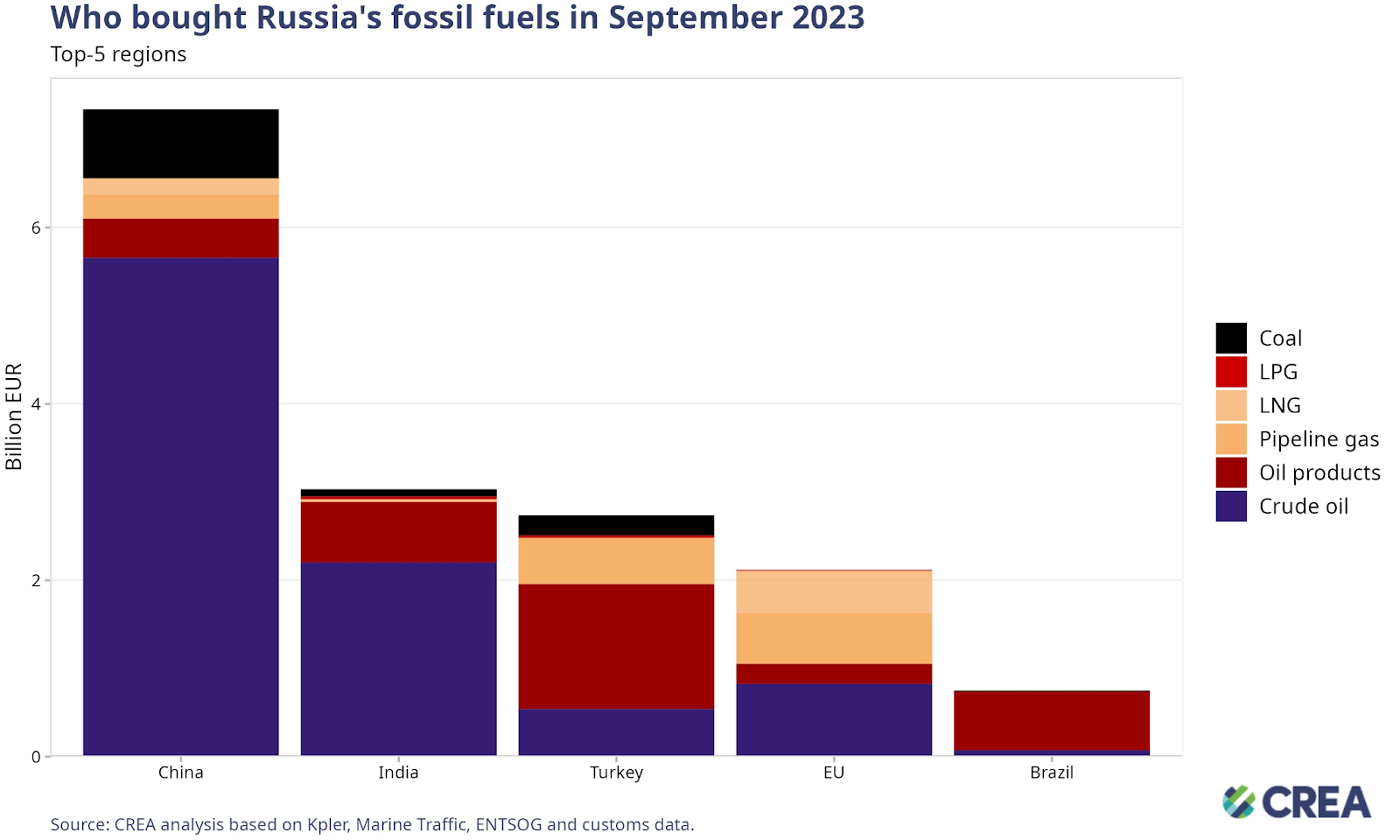

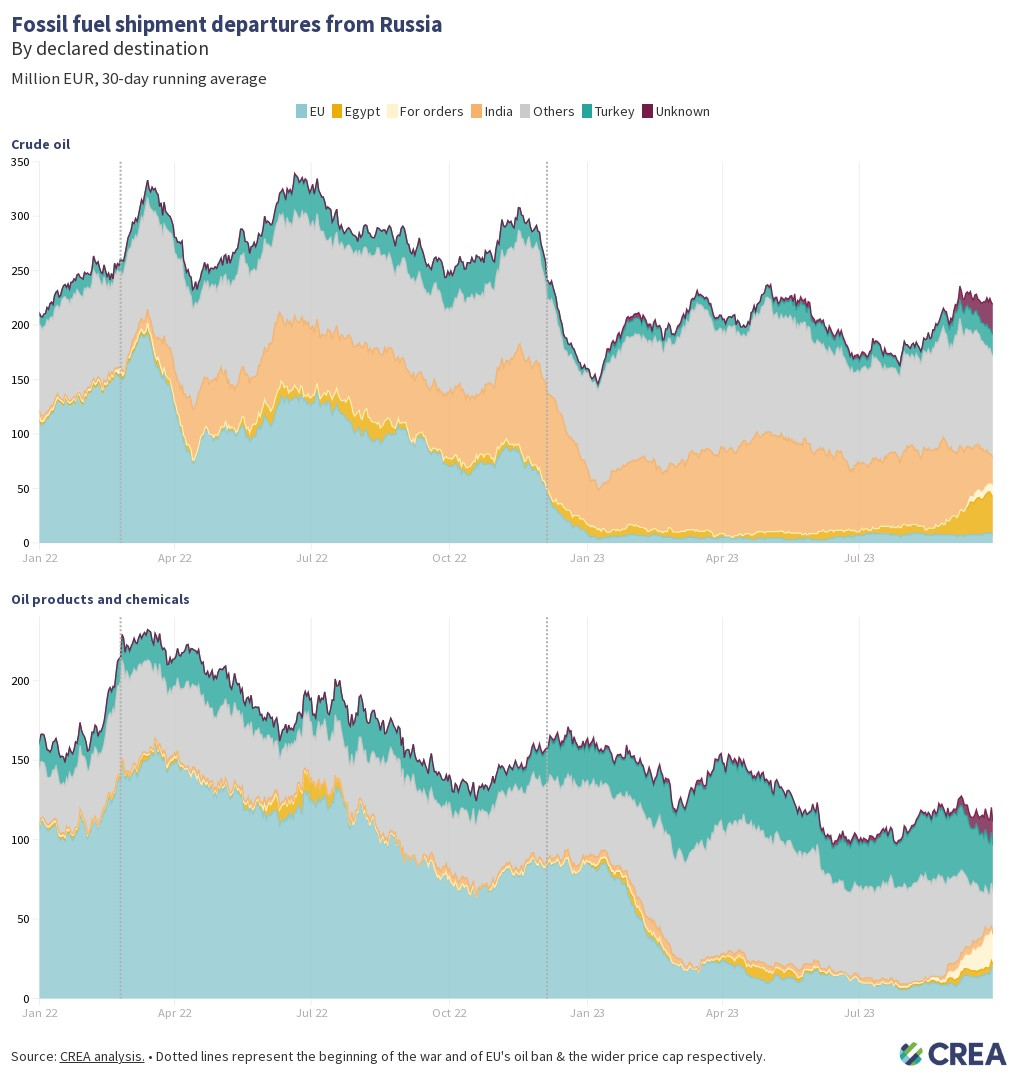

- China was the largest importer of Russian fossil fuels, followed by India, Turkey, the EU, and Brazil in September.

- Month-on-month, imports of Russian seaborne crude oil to China marginally increased by 2% in volume terms, and revenues increased by 25%, primarily importing Eastern Siberia–Pacific Ocean (ESPO) grade.

- In September, India’s monthly import volume of Russian crude oil decreased by 13% compared to the prior month, while month-on-month, Russia’s revenue from crude oil exports to India dropped by 20%.

- The European and G7 shipping industry plays a significant role in transporting Russian oil. The percentage of tankers subject to the price cap transporting crude oil shipments from Russia remained at approximately 50% in September. However, for oil products and chemicals, the coverage of tankers under the price cap saw a slight decrease of 3% in September compared to the previous month.

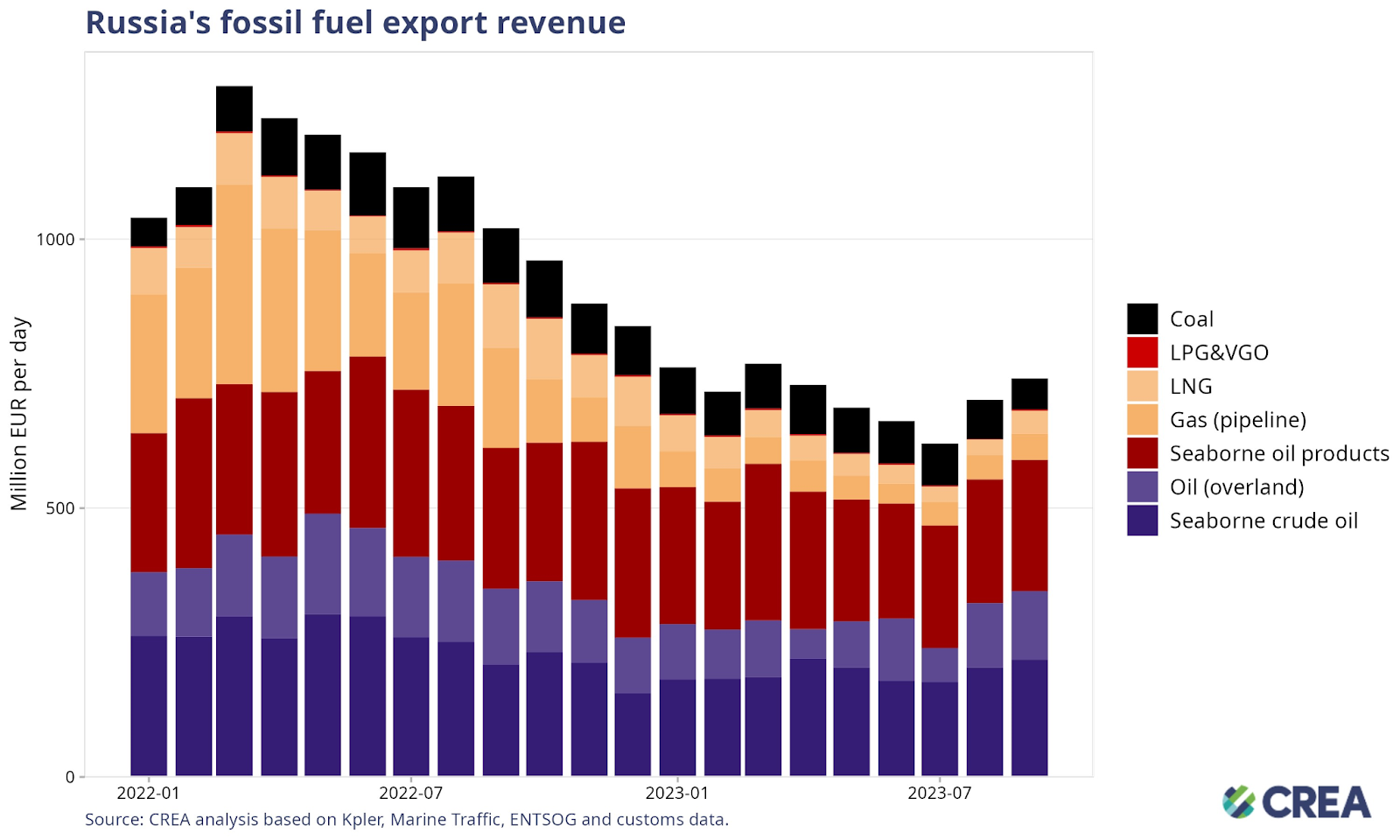

Trends in total revenue

- Russia experienced its lowest volume of fossil fuel exports in September since the start of the year. The volumes of crude oil, oil products, and coal fell compared with August, while LNG increased.

- Despite the decrease in volume, revenues from fossil fuels have increased for the second consecutive month. In September, crude oil prices remained high while month-on-month exported volumes have fallen 11 thousand tonnes (-3%).

- Despite a 5% month-on-month decrease in the volume of Russia’s fossil fuel exports, Russia’s earnings have experienced a monthly growth of 3% in September 2023 compared with August.

- In September, the most substantial month-on-month increase in the value of Russia’s fossil fuel exports was seen in LNG, experiencing a surge of EUR 14 mn per day (+48%). Revenues from pipeline gas increased by EUR 4 mn per day (+7%). LNG and pipeline gas revenues have risen for the second and third consecutive months.

- In September, Russia’s seaborne crude oil exports saw a notable increase of EUR 19 mn per day (+10%), marking the second consecutive month of growth, followed by pipeline oil, which rose by EUR 8 mn per day (+6%), experiencing growth for the second successive month.

- For the second consecutive month, revenues from seaborne oil products have declined. Compared to August, there was a decrease of EUR 10 mn per day, which accounts for a 5% reduction in monthly revenues. The drop was influenced by Russia’s partial and temporary ban on the export of gasoline and diesel to cope with a domestic market shortage.

- For the fifth consecutive month, Russia’s coal exports have declined. September, in particular, saw a substantial drop, with a daily decrease of EUR 14 mn (-20%) compared to August.

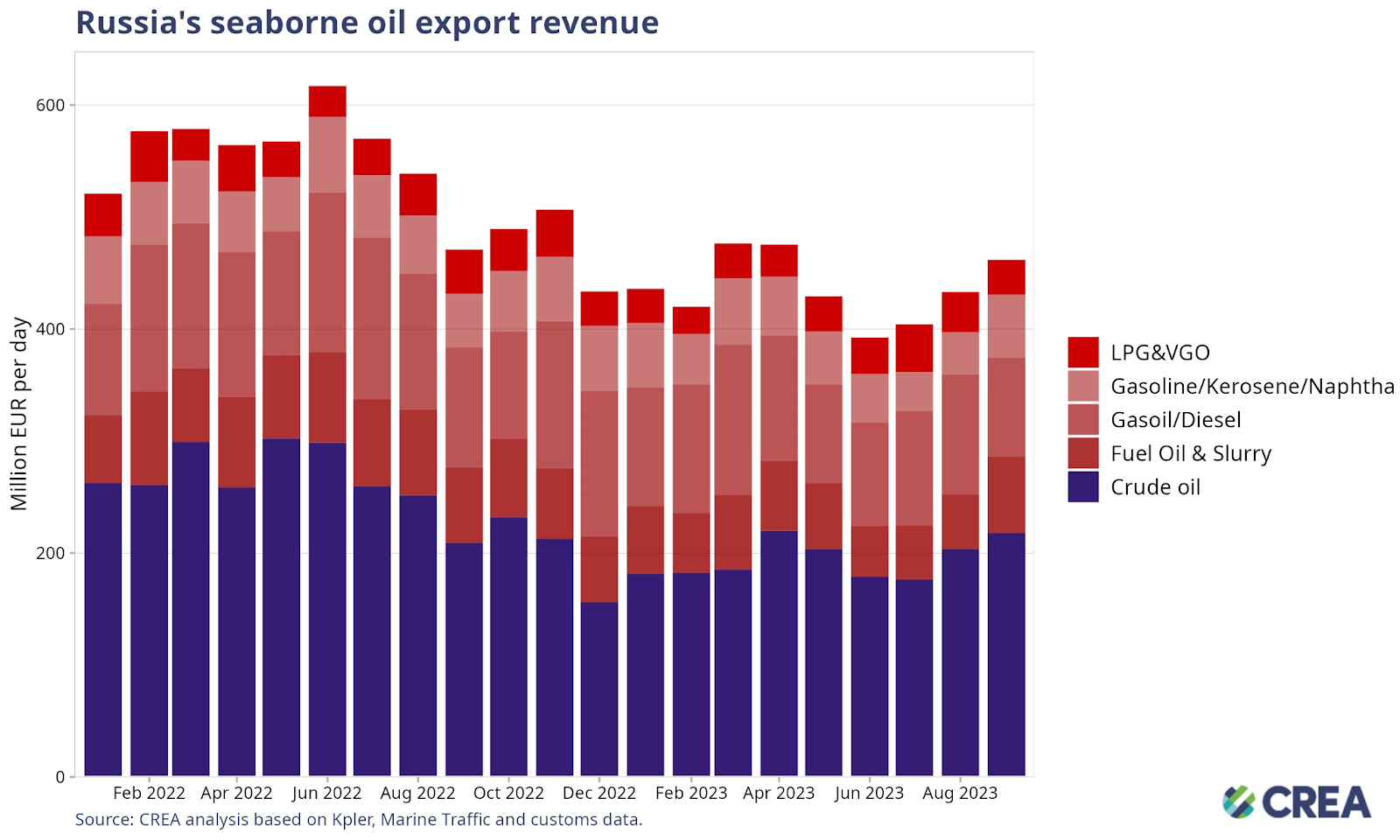

- In September, Russian seaborne oil export volumes reached their lowest level this year. This decline has been consistent since reaching its peak in March. Despite decreasing volumes, revenues have risen for the fourth consecutive month.

- The decline in seaborne oil volumes may be attributed to Russia’s pledge to curtail oil exports in both August and September.

- Despite a decrease in oil exports, Russia is experiencing an increase in revenues, primarily due to the upward trend in oil prices. According to the Russian Ministry of Finance, September saw a 15% month-on-month rise in revenues from fossil fuels, and a 24% and 34% increase in revenues from the Mineral Extraction Tax and from the Export Duty, respectively.

- On a monthly basis, Russia’s oil exports saw an increase of EUR 9 mn per day, marking a 2% rise compared to August.

- Seaborne crude oil export earnings in September rose by 10% or EUR 19 mn per day compared to the prior month.

- Sales of gasoil and diesel decreased by EUR 21 mn per day in September compared to the prior month, equivalent to a 21% decrease. The decline in diesel revenues can be linked to a reduction in exports, driven by the increased demand for diesel within Russia. Notably, the Russian government implemented a complete ban on diesel exports on September 21, which was subsequently lifted in October.

- Russia’s export value of gasoline, kerosine and naphtha oil products rose by 30% or EUR 10 mn per day in September compared to August.

- Fuel oil and slurry export earnings increased by 19%, equivalent to EUR 8 mn per day in September compared to August.

- Finally, Russia’s export earnings from LPG and vacuum gas oil (VGO) fell by EUR 8 mn per day or 27% in September compared to the prior month.

Who is buying Russia’s fossil fuels?

- In September, the primary export markets for seaborne Russian oil were India, which received 38% of all Russian oil exports, followed by China at 34%, and Turkey at 8% by volume.

- In volume terms, India’s monthly seaborne crude oil imports stayed at the same level compared to August. Russian seaborne oil exports to India saw a 13% decrease during the same period. The primary imported grade from Russia was Urals. A decline in Russian sales to India was compensated by increased purchases from Iraq (+15%) and Saudi Arabia (+4%). The surge in Iraq’s oil imports can be attributed to the ongoing negotiations between India and Iraq regarding a potential discount on the price of Iraqi oil.

- The reduction in India’s imports from Russia is primarily linked to a diminishing discount for Russia’s flagship grade, Urals, offered to Indian buyers. Consequently, Russia’s revenues from exports to India experienced a 20% decrease in September.

- Month-on-month, Russian seaborne crude oil exports to China saw a 15% increase compared to August in volume terms, with ESPO being the primary imported grade. The most substantial rise in China’s seaborne crude oil imports was from Saudi Arabia (+15%), Oman (+20%), and the United Arab Emirates (+25%). It’s worth mentioning that 22% of China’s import decrease originated from unidentified destinations. The slight rise in China’s crude oil imports can be attributed to the Chinese government’s reluctance to issue new quotas for clean product exports and crude oil imports. New quotas would help Chinese oil companies take advantage of hefty margins stimulated by Russia’s temporary export ban to sell gasoil overseas.

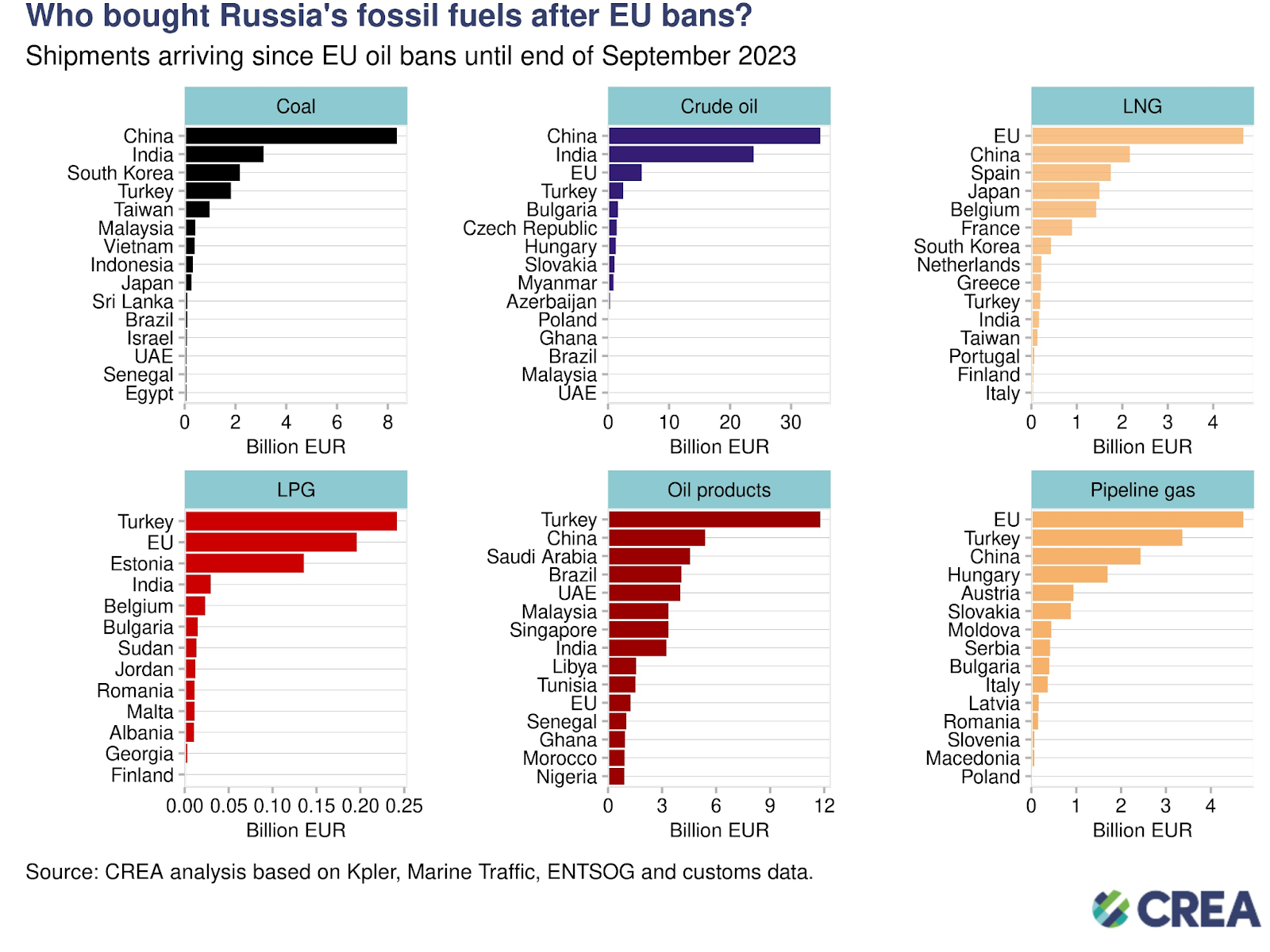

- Coal: As of September 2023, China was the largest buyer (purchasing 45% of Russia’s coal exports), followed by India (17%), and South Korea (12%), since the EU import ban on Russian crude oil was implemented (5 December 2022).

- Crude oil: China was the largest buyer (purchasing 47% of Russia’s crude oil exports), followed by India (32%), the EU (7%) and Turkey (3%). EU imports of crude oil since 5 December 2022 arrived via sea to Bulgaria and via pipeline for the Czech Republic, Slovakia and Hungary. Bulgaria has received an exemption to the Russian oil import ban and pipeline oil into the EU is also non-sanctioned.

- LNG: since 5 December 2022, the EU was the largest buyer (purchasing 50% of Russia’s LNG exports), followed by China (23%) and Japan (16%). No sanctions are imposed on Russian LNG shipments to the EU.

- LPG: Turkey was the largest buyer (purchasing 34% of Russia’s LPG exports), closely followed by the EU (28%). No sanctions are imposed by the EU on LPG imports from Russia.

- Oil products: since the EU import ban on Russian crude oil was implemented, Turkey was the largest buyer (purchasing 25% of Russia’s oil products), followed by China (12%) and Saudi Arabia (10%). EU sanctions on seaborne Russian oil products were implemented on 5 February 2023, oil via pipeline is only partially sanctioned.

- Pipeline gas: The EU was the largest buyer (purchasing 41% of Russia’s pipeline gas), followed by Turkey (29%) and China (21%). No sanctions are imposed on Russian gas via pipeline into the EU.

- In September, China stood out as the top importer of Russian fossil fuels, accounting for 46% of the total imports. India secured the second position by purchasing 20% of Russia’s fossil fuels. Turkey came in third, importing 17% of Russian fossil fuels. Meanwhile, the EU and Brazil contributed 13% and 4% to total Russian fossil fuel imports for the same period.

- Of China’s total imports of Russian fossil fuels, crude oil comprised the most considerable proportion, constituting a 77% share. Coal emerged as Russia’s second most imported fossil fuel, making up 10% of China’s total. In third place, there was a diverse category comprising oil products, 7%, and LNG and pipeline gas collectively accounting for 6% of China’s total Russian fossil fuel imports.

- India ranked as the second-largest importer of fossil fuels from Russia in September. Crude oil accounted for 82% of India’s total fossil fuel imports from Russia. Oil products ranked in second place, with a share of 14%, while Russian coal imports represented 2% of the total. LPG and LNG combined share was 2%.

- Turkey remained the third-largest importer of Russian fossil fuels. In September, Turkey’s imports from Russia comprised various fossil fuels, with a significant share of 51% attributed to oil products. Additionally, 19% of Turkey’s total imports from Russia included pipeline gas, while crude oil and coal contributed 21% and 8%, respectively. A smaller portion of 1% represented Turkey’s imports of LPG from the total imports of Russian fossil fuels.

- In September, the EU ranked as the fourth-largest purchaser of Russian fossil fuels. Of the EU’s total Russian fossil fuel imports during this period, 39% consisted of crude oil (Bulgaria imported Russian seaborne crude as it has an exemption to the EU imports ban, and other Member States import crude oil via pipeline). Additionally, pipeline gas accounted for 27% of the EU’s total imports of Russian fossil fuels, while LNG constituted 21%. In September, oil products and liquefied petroleum gas (LPG) made up 12% and 1% of the EU’s Russian fossil fuel imports, respectively.

- In September, Brazil remained the fifth-largest importer of Russian fossil fuels globally. Petroleum products constituted the majority, making up 88% of the total Russian fossil fuel imports, while crude oil accounted for 10%, and coal represented 2%.

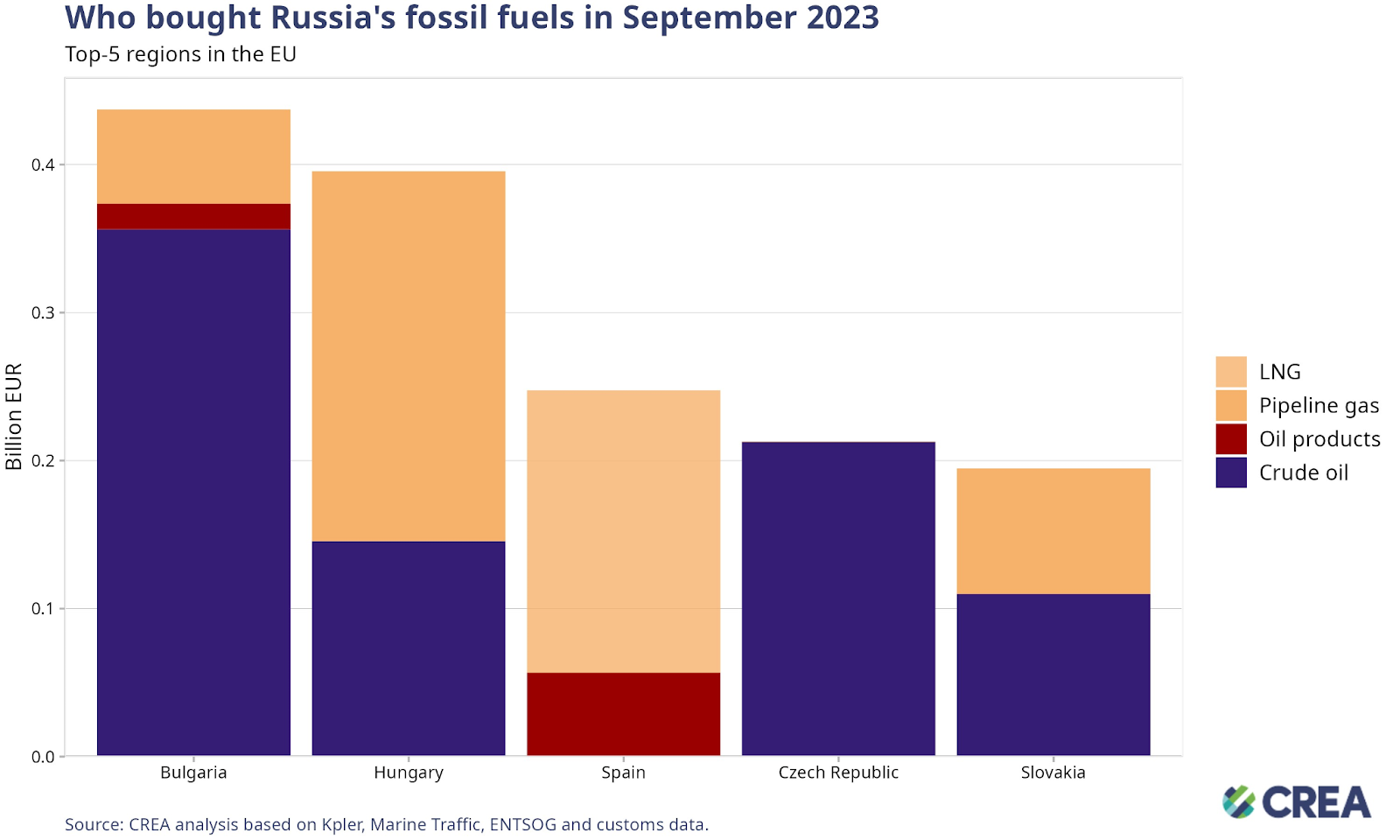

- Landlocked Central and Eastern European countries received Russian natural gas via pipeline through Ukraine and TurkStream, and crude oil was obtained via the Druzhba oil pipeline. The EU has not banned Russian natural gas and crude oil via the Druzhba south branch.

- The month-on-month volume of Russian oil exported to Bulgaria increased by 13%. Bulgaria has been granted an exception for the importation of Russian oil. All the oil originating from Russia and transported to Bulgaria ultimately finds its way to the Neftochim Burgas refinery, the largest refinery in the Balkan peninsula, owned by the Russian company Lukoil. The Parliament of Bulgaria recently voted that this refinery will continue its operations with Russian oil until 30 September 2024, after which the exception will be entirely lifted. During this period, the refinery must progressively shift towards using oil from different sources. Starting November 2024, the facility will be mandated to process non-Russian sourced oil exclusively.

- In terms of quantity, the monthly imports of Russian fossil gas to Hungary dropped by 14% compared to August. The drop marks the third consecutive month of declining Russian fossil gas imports to Hungary. The reason behind this continuous decrease in fossil gas imports to Hungary is twofold. First, the underground gas storage facilities in the country are nearly at full capacity, reaching almost 96% of their total volume, as reported by Gas Infrastructure Europe (GIE) data. Second, there is lower gas consumption due to seasonal factors, according to data from CREA. Hungary has taken steps to reduce its reliance on Russian gas by announcing an agreement with Poland to transport gas from a newly constructed LNG terminal in Poland.

- In September, Spain’s total LNG imports increased by 22% compared to August, while the month-on-month LNG imports from Russia saw a significant rise of 25%. In September, Spain’s send-out from LNG terminals to the gas system increased by 10% compared to August. Concurrently, there was an uptick in gas exports to France, according to data from European Network of Transmission System Operators for Gas (ENTSOG).

- Despite the Czech Republic’s ongoing imports of Russian oil, Mero, the entity responsible for the Czech section of the Druzhba pipeline and the IKL pipeline, has started implementing oil transportation and storage plans until 2025. They aim to attain complete independence from Russian oil by 2025 through investments in the Transalpine oil pipeline system.

- In September, Slovakia’s natural gas imports rose by 20% from August. Meanwhile, Russian gas imports spiked by 30% in the same period. Slovakia is actively working to reduce its reliance on Russian gas. Last year, it took substantial steps towards diversification, including opening an interconnector with Poland for access to Polish and Lithuanian gas. This September, Slovakia signed an agreement with ExxonMobil for LNG supply from Croatia or Italy. These initiatives reflect Slovakia’s commitment to diversifying its gas sources and decreasing dependence on Russian imports.

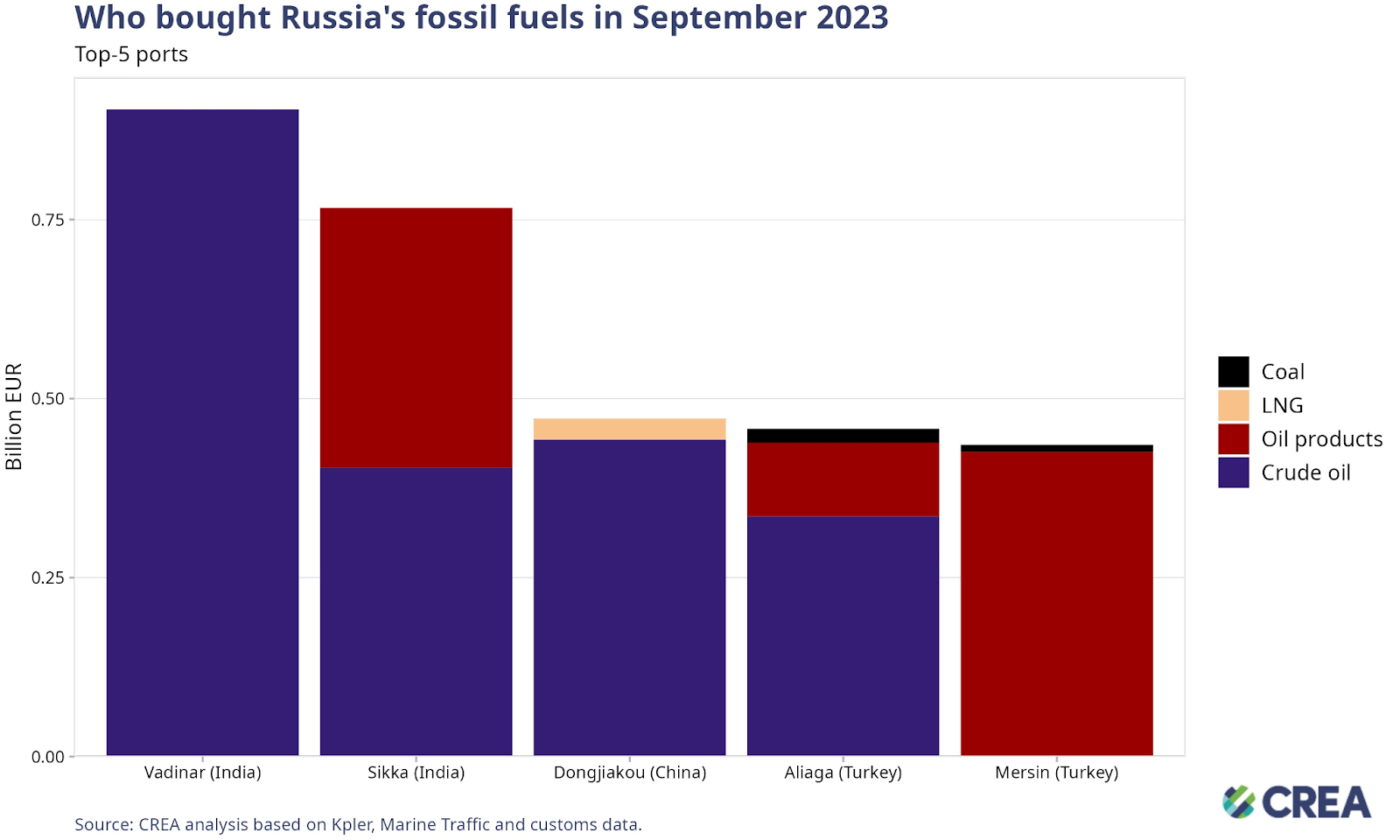

- In September, the port of Vadinar became the largest port for importing Russian fossil fuels, with imports exceeding a substantial monthly total of EUR 0.9 billion.

- The other top ports importing Russian fossil fuels from Russia in September were Sikka (India), Dongjiakou (China), Aliaga (Turkey), and Mersin (Turkey).

How are oil prices developing?

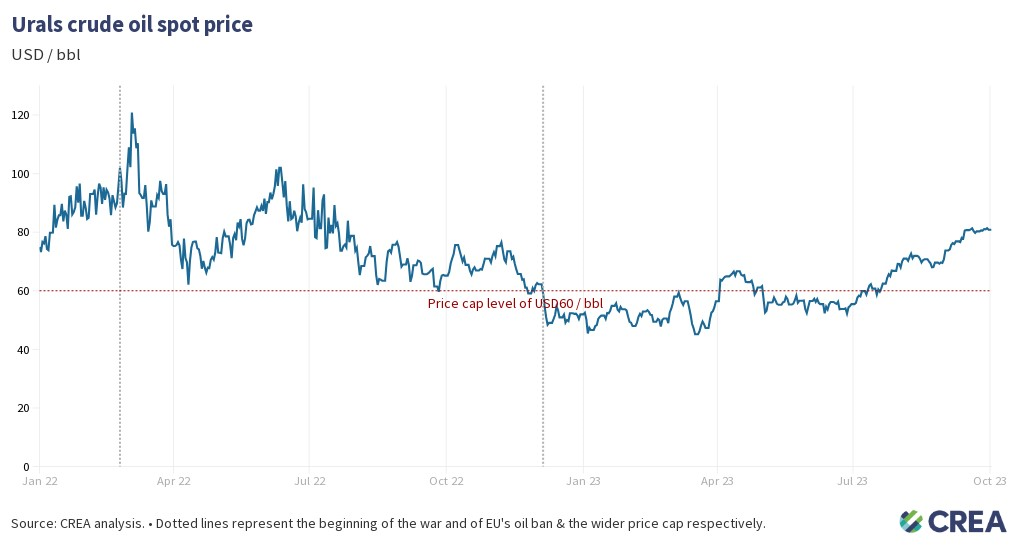

- Urals crude prices have stayed above the oil price cap (60 USD) since the middle of July. In September, the average price for Russian Urals was USD 78.1 per barrel, and increased by 10.4% compared with August.

- The prices for the East Siberia–Pacific Ocean (ESPO) and Sokol blends, primarily associated with Asian markets, showed an 8% increase in September compared to levels in August. These prices consistently remained above the specified price cap level for the entire month.

- Throughout this period, vessels owned or insured by G7 and European nations persisted in loading Russian oil at all ports within Russia. These occurrences serve as compelling evidence of violations against the price cap policy.

- The first reports have appeared showing the US starting an investigation of oil traders that could have breached the oil price cap policy. The EU should similarly undertake investigations of insurers, vessels owners, traders, etc. that appear to have violated the policy.

Russia remains highly reliant on European and G7 shipping industry

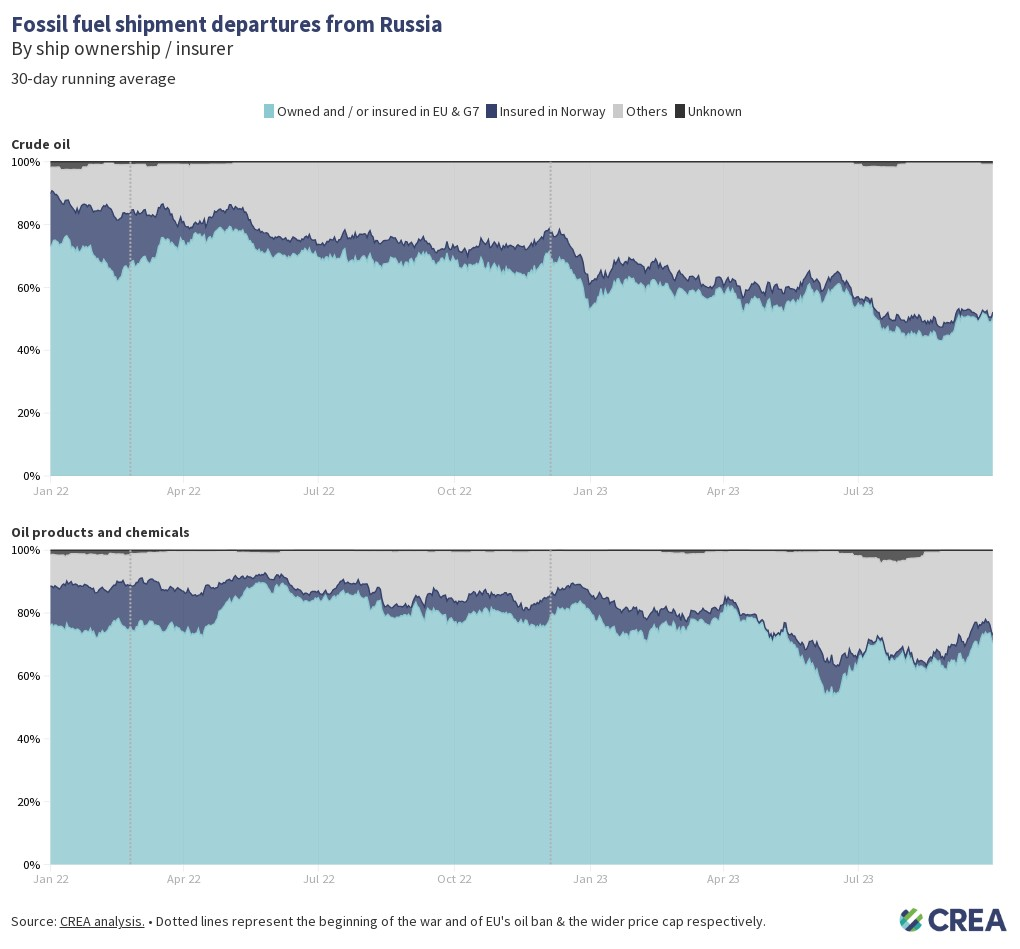

- In September, the percentage of tankers subject to the oil price cap that transported crude oil from Russia remained consistent with the previous month, at around 50%. “Shadow” tankers, those that are not subject to the price cap policy, transported the remaining portion of Russia’s crude oil volumes. For tankers transporting oil products and chemicals and LPG, the coverage of the price cap coalition slightly decreased in September (67%) compared to August (64%). Conversely, 33% of these products were transported by “shadow” tankers in September.

- In September, most of Russia’s total oil exports were shipped from Russian Baltic Sea ports, accounting for 57% by volume. Additionally, 22% were exported through Black Sea ports, while 16% originated from Pacific ports. The remaining 4% came from ports in the Arctic.

- The proportion of tankers utilizing vessels insured or owned by countries implementing price caps to transport fossil fuels from Russia’s Baltic and Black Sea ports is significantly higher than in the Pacific ports. In September, 56% and 80% of Russian oil exports worldwide were transported on tankers insured or owned by these price cap implementing countries. The remaining volume was transported by “shadow” tankers. The situation is the opposite in Russian Pacific ports. In September, 23% of Russian crude oil exports were carried by tankers insured or owned by countries implementing price caps. These tankers loaded Russian oil at ports like Kozmino, where the ESPO pipeline ends and is connected to the refinery. Here, the ESPO crude oil grade is exported at prices exceeding the cap.

- The high proportion of shipments transporting Russian oil with EU/G7 insurance and/or vessels outlines how strong a set of tools the price cap coalition has to force down Russia’s oil export revenues by lowering the price cap while implementing significantly better monitoring and enforcement measures.

How can Ukraine’s allies tighten the screws?

- Fossil fuel exports from Russia have fallen since sanctions were implemented, showing the impact they have had at lowering Putin’s ability to fund the war. However, much more should be done to limit Russia’s export earnings and constrict the Kremlin’s war chest such as lowering the oil price cap, increasing monitoring and enforcement of sanctions and banning unsanctioned fossil fuels such as LNG, LPG and pipeline fuels that are legally allowed into the EU.

- Additionally, measures must be taken to prevent Russia’s ability to ship its oil without relying on western owned or insured vessels and circumventing the price cap policy; actions could include banning the sale of old tankers used to transport Russian oil.

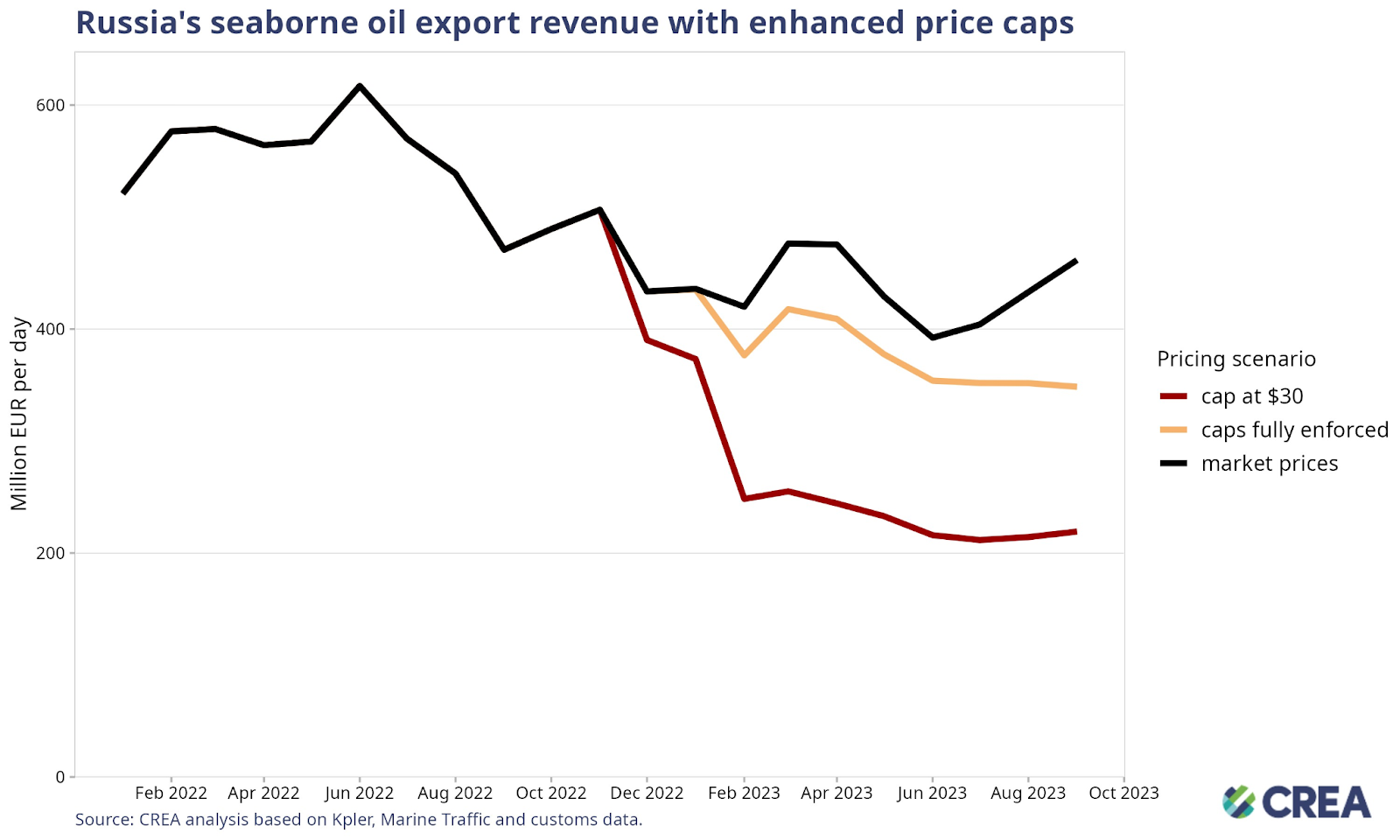

- Over the period starting from when sanctions on Russian oil were imposed up until the end of September 2023, Russian revenues could have been slashed by EUR 50 bn (48%), while this month alone, revenues could have been decreased by EUR 7.27 bn (53%) by setting the cap for crude oil at USD 30 per barrel (still well above Russia’s production costs, averaging USD 15). Lowering the price cap would be deflationary, reducing Russia’s oil export prices and inducing more production from Russia to make up for the drop in revenue.

- Even with the rising prices of Russian oil, trade with Russia continues. If full enforcement of the current cap had been implemented, it would have reduced Russia’s oil export revenue by approximately EUR 3.4 billion, which represents a 25% decrease.

- Higher oil prices for Russian grades pushed its monthly export revenues up by 3% compared to August. It is essential that sanction imposing countries tighten the monitoring and enforcement of the oil price cap policy, forcing Russian exporters to offer larger discounts on their oil exports.

- Institutions overseeing sanctions implementation must undertake vigilant investigations of entities such as insurers that are registered in countries implementing the price cap policy and are facilitating the transportation of Russian oil.

- Penalties must be implemented on entities that are caught violating sanctions to increase the perceived risk of others violating the oil price cap in pursuit of profit. Despite clear evidence of violation, there are minimal reports in the media of enforcement agencies implementing penalties against shippers, insurers or vessel owners.

- Penalties for those found guilty of violating the price cap must be significantly harsher. Current penalties provide for a 90-day ban of vessels from securing maritime services after violating the price cap, a mere slap on the wrist. Vessels should be fined and banned in perpetuity if they are found guilty of violating sanctions.

- Without greater monitoring and enforcement of the oil price cap policy to prevent violations of the sanctions, Russian oil prices and Putin’s export revenues used to fund the war have been increasing.

Relevant reports:

- Shedding light on “shadow” tankers – Who transports Russia’s oil 18 months into the invasion?

- Putin Green-lights Novatek’s Massive Murmansk LNG Project.

- Authorities weigh action on Indian fuel exports made from Russian oil.

- Russian Seaborne Oil Exports Drop to Lowest Level since September 2022, but Revenues Surged – Russian Oil Tracker by KSE Institute.

- France’s LNG paradox.

- How Ukraine Fights for the European Embargo on Russian Liquefied Natural Gas.

| The monthly update on Russian fossil fuel exports and sanctions was prepared by Isaac Levi, Europe-Russia Policy & Energy Analysis Team Lead, CREA; and Hubert Thieriot, Lead Data Scientist, CREA. |

| Note on methodology: From 2023‑04‑03, our monthly analysis values are no longer seasonally corrected, which may lead to some disparities between the preceding and following reports. We have also adjusted our time frame to show totals since the start of 2023 rather than the start of the invasion. Dates featured are the date the arrival of the shipment was captured by our algorithm. 80% of arrivals for shipments are found within 4 days of the arrival port call in the specific port. For our oil products and chemicals commodity group, please note this contains a wider range of items than just those specified in the current sanctions, as of 2023‑02‑05. More information at: https://energyandcleanair.org/ |