Russia’s fossil fuel export earnings rise 2% in May as EU LNG imports climb despite new restrictions

Authors: Luke Wickenden and Isaac Levi; Data scientist: Panda Rushwood

Key findings

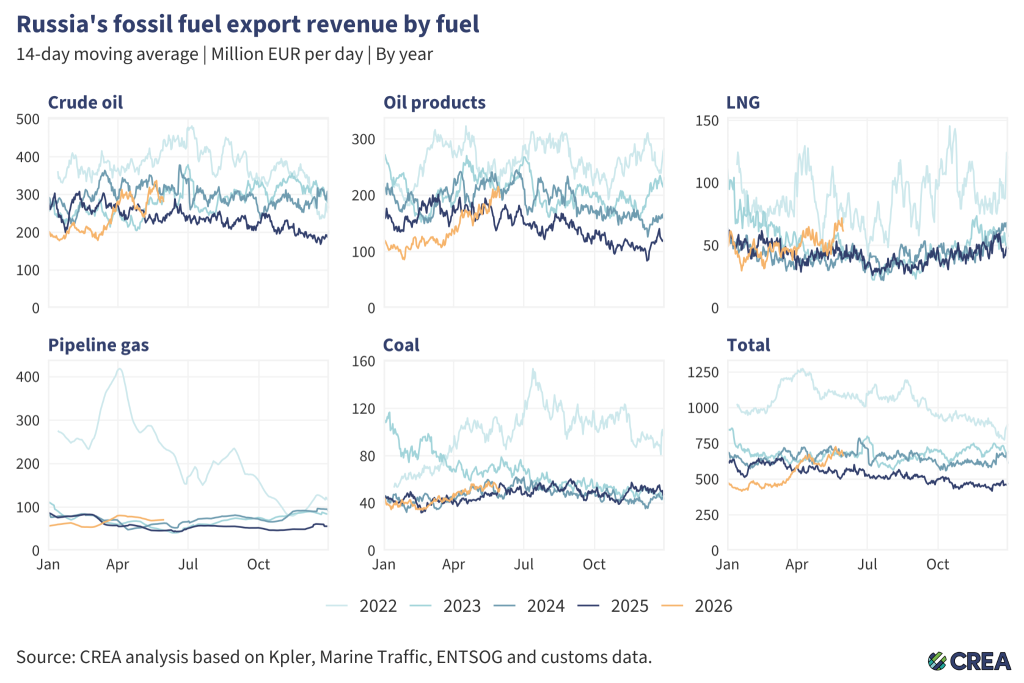

- In May 2026, Russia’s fossil fuel export revenues increased by 2% month-on-month to EUR 726 mn per day despite export volumes remaining roughly the same as in April.

- Russia’s crude oil export revenues grew marginally by 1% month-on-month to EUR 362 mn per day, while volumes increased by 8%. Crude oil loadings at Russia’s fourth-largest export port, Ust-Luga, rose 49% month-on-month after a period of reduced exports following repeated Ukrainian drone strikes on Russia’s export infrastructure in March and April 2026.

- A significant 53% month-on-month decline in oil product exports was recorded at Taman, one of Russia’s key Black Sea ports, following drone strikes in mid-May.

- In May 2026, Turkiye’s total seaborne crude imports saw a 28% month-on-month increase but a 22% decrease in imports from Russia, as the country imported more US crude than it had in the last two years combined.

- Flows through the Druzhba pipeline, which carries Russian crude oil to Hungary and Slovakia, resumed on 23 April after almost three months of inactivity, contributing to a 22% month-on-month increase in Russia’s pipeline oil export revenues.

- Ten shipments of oil products from refineries using Russian crude — and identified as high risk according to EU guidance — were unloaded at EU ports in the month of May.

- LNG loadings at Russia’s largest Yamal installation reached their highest level in 18 months.

- Despite a new UK ban, 99% of the EUR 4.4 bn in UK imports of oil products partially made from Russian crude between December 2022 and May 2026 — jet fuel and diesel — remain exempt from restrictions.

- EU imports of Russian LNG increased by 4% month-on-month in May 2026, despite the ban on short-term contract purchases taking effect on 25 April 2026, driven largely by Spain doubling its supply of Russian gas.

- In May 2026, 48% of Russia’s seaborne oil was transported by ‘shadow’ tankers under sanctions. A further 44% of the volume was transported by G7+ tankers. The remainder was transported by non-sanctioned ‘shadow’ tankers.

Trends in total export revenues

- In May 2026, Russia’s fossil fuel export revenues increased by 2% month-on-month to EUR 726 mn per day despite export volumes remaining roughly the same as in April.

- Russia’s crude oil export revenues grew marginally by 1% month-on-month to EUR 362 mn per day, while volumes increased by 8%. Crude oil loadings at Russia’s fourth-largest export port, Ust-Luga, rose 49% month-on-month after a period of reduced exports following repeated Ukrainian drone strikes on Russia’s export infrastructure in March and April 2026.

- Russian pipeline crude oil exports have increased by 22% month-on-month, influenced by the resumption of flows through the southern section of the Druzhba pipeline to Hungary and Slovakia on 23 April.

- Liquefied natural gas (LNG) revenues decreased by 6% to EUR 55 mn per day while export volumes dropped 3% month-on-month. May saw the highest-ever volume of LNG exported from the Murmansk ship-to-ship (STS) transfer locations. LNG loadings at Russia’s largest Yamal installation reached their highest level in 18 months.

- Pipeline gas export revenues decreased by 9% to EUR 70 mn per day, while export volumes dropped 4% month-on-month.

- Revenues from the exportation of seaborne oil products saw a 10% month-on-month increase, generating EUR 186 mn per day in export earnings, the highest per day revenue since August 2024. This is despite oil product export volumes decreasing massively by 20% month-on-month. A significant 53% month-on-month decline in oil product exports was recorded at Taman, one of Russia’s key Black Sea ports, following drone strikes in mid-May. Monthly loadings of Russian oil products at the Black Sea port of Tuapse were 91% lower than in May 2025, following a sustained campaign of drone strikes targeting the refinery.

- Coal export revenues grew by 5% month-on-month, reaching EUR 54 mn per day, with export volumes also rising by 5%.

Who is buying Russia’s fossil fuels?

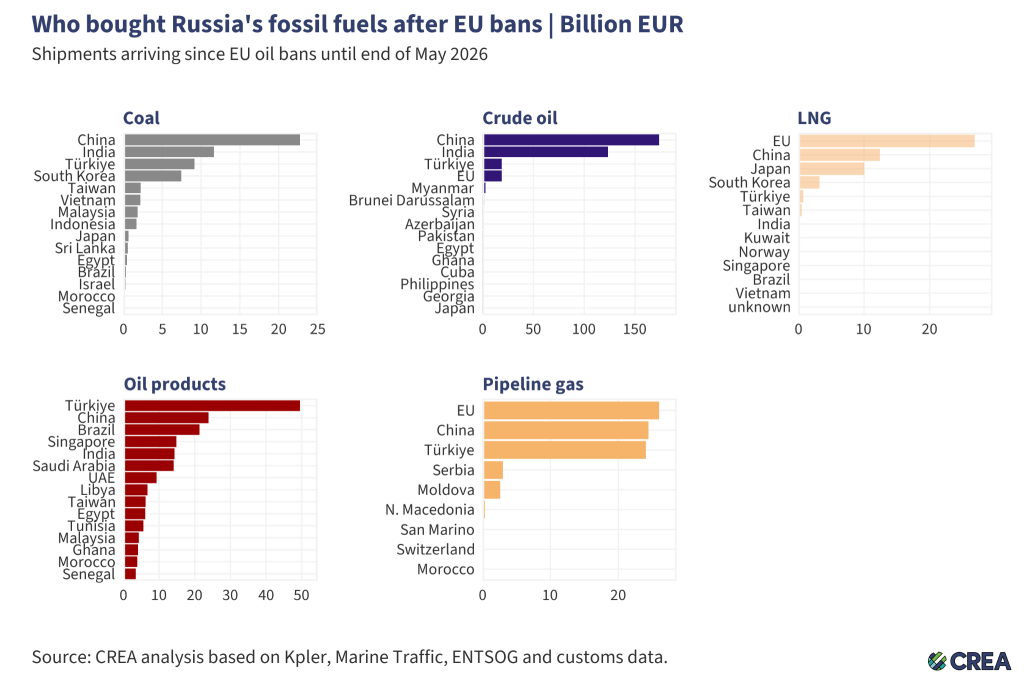

- Russia’s fossil fuel exports remain highly concentrated, with China dominating purchases of coal and crude oil, Turkiye leading purchases of oil products, and the EU remaining the largest buyer of LNG and pipeline gas — showing Moscow’s dependence on a narrow set of key customers.

- Coal: From 5 December 2022 until the end of May 2026, China purchased 37% of all Russian coal exports. India (19%), Turkiye (15%), South Korea (12%), and Taiwan (4%) round out the top five buyers’ list.

- Crude oil: China has bought 50% of Russia’s crude exports, followed by India (36%), Turkiye (6%), and the EU (5%).

- Oil products: Turkiye, the largest buyer, has purchased 26% of Russia’s oil product exports, followed by China (13%), Brazil (11%), and Singapore (8%).

- LNG: The EU remains the largest buyer of Russian LNG, accounting for almost half (49%) of Russia’s total LNG exports, followed by China (23%) and Japan (18%).

- Pipeline gas: The EU is the largest buyer, purchasing 32% of Russia’s pipeline gas exports, followed by China (30%) and Turkiye (30%).

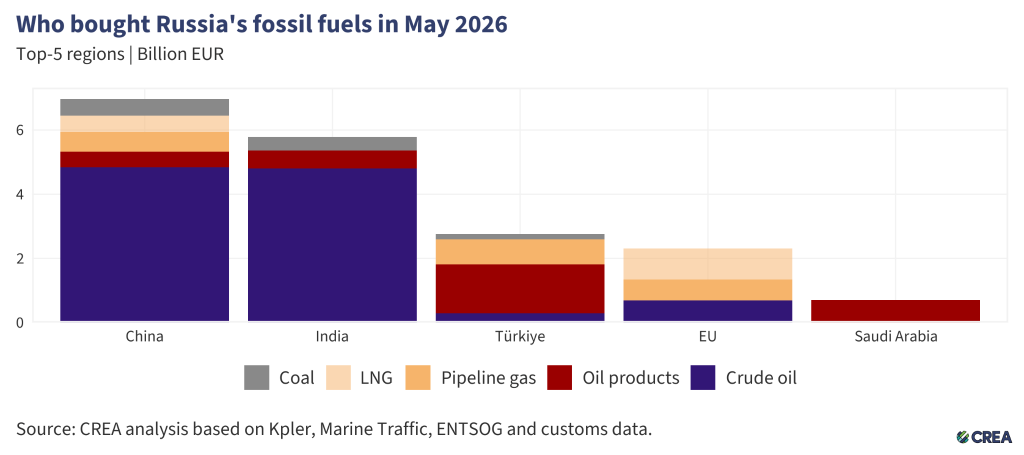

- In May 2026, China remained the largest global buyer of Russian fossil fuels, accounting for 38% (EUR 7.0 bn) of Russia’s export revenues from the top five importers. Crude oil made up 69% (EUR 4.8 bn) of China’s purchases, followed by pipeline gas (EUR 618 mn), then coal (EUR 525 mn), and lastly LNG (EUR 510 mn). Oil products (EUR 479 mn) constituted the remainder of China’s imports.

- China’s total seaborne crude import volumes saw a marginal 17% month-on-month decrease in May. Imports of Russian seaborne crude dropped 23% month-on-month. The vast majority (64%) of China’s seaborne Russian crude imports were East Siberia–Pacific Ocean (ESPO) grade, shipped from the Pacific port of Nakhodka.

- While total imports by Chinese installations fell in May, imports of Russian crude unloaded at the Dongjiakou oil terminal increased by 144%, reaching their highest level in the past two years. This increase in imports of Russian crude from the Dongjiakou oil terminal correlates with a 66% month-on-month decrease in imports from Iran’s Kharg Island.

- India was the second-largest buyer of Russian fossil fuels in May 2026, importing a total of EUR 5.8 bn of Russian hydrocarbons. Crude oil constituted 83% of India’s purchases, totalling EUR 4.8 bn. Oil products (EUR 550 mn) and coal (EUR 429 mn) constituted the remainder of their monthly imports.

- India’s total crude import volumes recorded an 8% month-on-month increase in May. This is partially explained by a 21% month-on-month increase in Russian imports. There was a marginal increase in Russian crude imports at India’s major installations, with unloaded volumes at the Vadinar and Jamnagar refineries increasing by 36% and 14%, respectively.

- The state-owned New Mangalore and Visakhapatnam refineries had stopped Russian imports at the end of November 2025, but purchases resumed in March 2026 and continued in April and May. Both refineries saw further month-on-month increases in Russian imports of 13% and 42%, respectively. Furthermore, the Paradip refinery unloaded the highest quantity of Russian crude in two years.

- Turkiye was the third-largest importer, purchasing EUR 2.8 bn of Russian hydrocarbons in May. Oil products accounted for the largest share at 55% (EUR 1.5 bn), followed by pipeline gas (EUR 783 mn), and crude oil (EUR 290 mn). The remainder of Turkiye’s monthly imports from Russia were made up of coal (EUR 159 mn).

- In May 2026, Turkiye’s total seaborne crude imports saw a 28% month-on-month increase but a 22% decrease in imports from Russia, as the country imported more US crude than it had in the last two years combined.

- The EU was the fourth-largest buyer of Russian fossil fuels, accounting for almost 12% (EUR 2.3 bn) of Russia’s export revenues from the top five importers in May.

- Forty-two percent of the EU’s imports (EUR 966 mn) consisted of LNG, and another 30% was crude oil. The remaining 28% consisted of pipeline gas.

- Surprisingly, the EU’s imports of Russian LNG rose by 4% month-on-month in May 2026, following the EU’s ban on short-term supply contract purchases of Russian LNG, which took effect on 25 April 2026. The increase was driven largely by Spain doubling its imports from Russia, underscoring the importance of strict enforcement and transparency to prevent the phase-out from being undermined by continued purchases under legacy contracts. If the short-term supply contracts were concluded before 17 June 2025, the increased quantity of Russian LNG unloaded at EU ports would not violate the REPowerEU regulation.

- Saudi Arabia was the fifth-largest importer in May, with all of its purchases totalling EUR 710 mn, all of which were oil products. While the Jizan Refinery saw a 137% increase in Russian imports, all Saudi imports of Russian refined fuels continued to unload at its Western ports, with no shipments of Russian oil products to Saudi ports transiting the Strait of Hormuz. In May, the Jizan refinery on Saudi Arabia’s western coast exported a record volume of oil products to the EU.

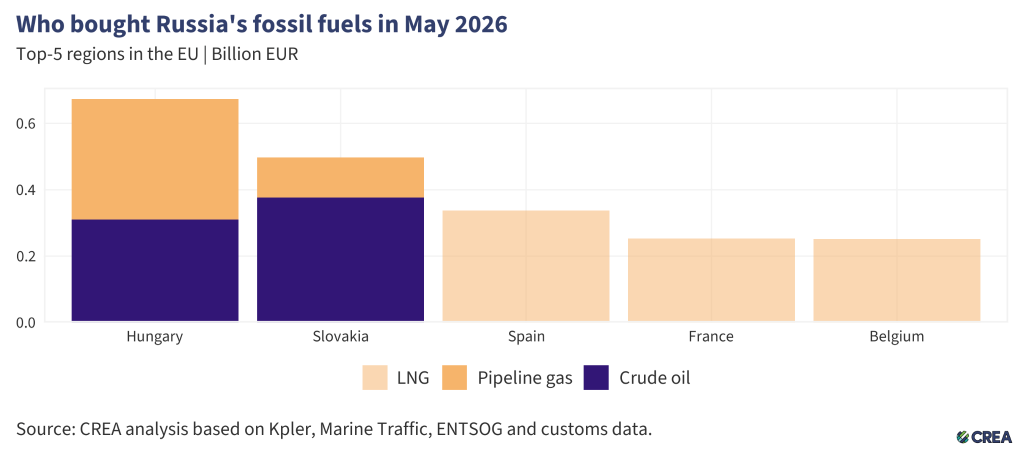

- In May 2026, the five largest EU importers of Russian fossil fuels paid Russia a combined EUR 2 bn. Natural gas — partially sanctioned by the EU — accounted for 66% of the value of imports from the five largest buyers. The five largest EU importers purchased EUR 842 mn of Russian LNG in May, EUR 485 mn of pipeline gas, and EUR 687 mn of crude oil through the Druzhba pipeline.

- Hungary and Slovakia received EUR 485 mn in pipeline gas via the Balkan Stream pipeline.

- Hungary was the EU’s largest buyer, importing EUR 674 mn of Russian fossil fuels. In May, Hungary’s imports of Russian fossil fuels consisted of pipeline gas and crude oil.

- Slovakia was the second-largest EU importer, receiving EUR 497 mn in Russian fossil fuel imports. Their imports consisted of EUR 121 mn in pipeline gas purchases and EUR 376 mn in crude oil purchases via the Druzhba pipeline.

- Spain was the third-biggest importer, receiving EUR 337 mn of Russian fossil fuels, all of which was LNG. Despite the EU’s ban on short-term Russian LNG contracts coming into force on 25 April, Spain’s Russian LNG imports doubled month-on-month in May. By contrast, the country’s total LNG imports increased by a far less significant 14%. Bilbao unloaded twice as much Russian LNG in May as in April 2026. The port of Cartagena unloaded its first shipment of Russian LNG in one and a half years.

- France was the EU’s fourth-largest importer, purchasing EUR 253 mn worth of Russian LNG in May. There was a 29% month-on-month decrease in France’s imports of Russian LNG. Meanwhile, its total LNG unloadings also dropped by 23% month-on-month.

- Belgium was the bloc’s fifth-largest importer, unloading EUR 252 mn of Russian LNG in May. Belgium’s LNG imports from Russia decreased by 25% month-on-month. Meanwhile, its total LNG unloadings dropped by a higher proportion of 31% month-on-month.

- Despite the EU’s ban on imports of oil products made from Russian crude on 21 January 2026, 10 shipments of oil products from refineries using Russian crude — and identified as high risk according to EU guidance — were unloaded at EU ports in the month of May.

- Six of these shipments departed from Turkiye’s refineries and three from Georgia.

- Cyprus was the largest recipient of shipments from these refineries running on Russian crude, unloading three shipments in May. Spain unloaded two shipments from refineries running on Russian crude. Meanwhile, Bulgaria, Croatia, France, Ireland, and Italy each received one shipment.

- Enforcement agencies in Member States must investigate shipments of oil products imported from refineries that run on Russian crude to prevent Russian oil molecules from entering the bloc, which would violate the EU’s recently implemented ban.

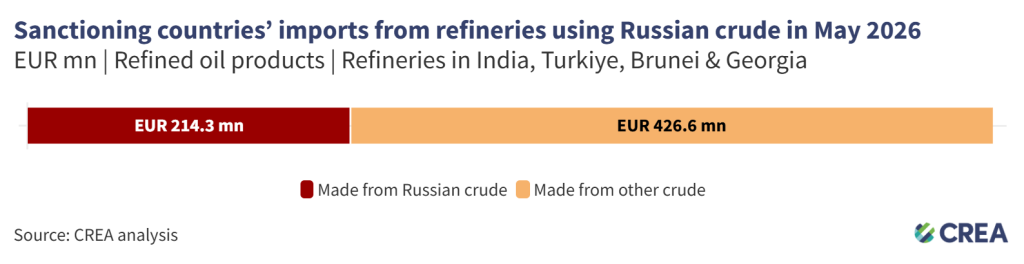

- Refineries using Russian crude in India, Turkiye, Brunei, and Georgia exported EUR 641 mn of oil products to sanctioning countries in May 2026. The importers included the EU (EUR 174 mn), Australia (EUR 275 mn), the US (EUR 147 mn) and New Zealand (EUR 45 mn). An estimated EUR 214 mn of these products were refined from Russian crude.

- There was an overall 28% month-on-month decrease in exports from these refineries to sanctioning countries. The UK did not receive a single shipment from these refineries in May. Exports of oil products to the EU from refineries running on Russian crude sky rocketed 197% in value terms month-on-month, while those to Australia fell 55% month-on-month.

- Exports to the US originated at the Jamnagar refinery in India, the SOCAR-owned STAR refinery in Turkiye, and the Tupras Izmit refinery as well. In the prior three months, 39% of the STAR refinery’s crude oil feedstock and 15% of the Jamnagar refinery’s feedstock came from Russia.

- The Kulevi refinery in Georgia continues to run solely on Russian crude and has not received a single shipment of non-Russian crude, while also exporting refined products to the EU after the ban came into force. At the end of March, the CEO of the refinery’s operating company stated that they are working to replace Russian crude oil. Despite this commitment to end reliance on Russian crude, 100% of the refineries’ imports came from Russia in May 2026. Furthermore, the refinery narrowly escaped being added to the EU sanctions list in March.

| The UK bans oil products made from Russian crude, while leaving an indefinite exemption covering 99% of imported fuels |

|

| The UK Government’s ban on Russian crude oil and oil products came into force on 5 December 2022. However, for more than three and a half years, a loophole remained that legally allowed oil products refined from Russian crude in non-sanctioning countries to be imported by companies in the UK. On 15 October 2025, the UK announced it would implement a ban on oil products derived from Russian crude, but provided no clear implementation date. Just over seven months later, on 19 May 2026, the United Kingdom declared a ban on oil products refined from Russian crude oil in third countries, which came into force the following day. However, the measure currently excludes jet fuel and diesel, which together accounted for 99% of the UK’s imports of oil products produced from Russian crude since the UK’s direct ban on Russian oil imports took effect in December 2022. The exemption currently remains open-ended, with no specified end date. CREA analysis estimates that between the start of the UK’s ban on Russian oil imports (5 December 2022) and the end of May 2026, the UK imported EUR 4.4 bn worth of oil products from refineries in India and Turkiye that processed Russian crude oil. Of these imports, an estimated EUR 1.9 bn consisted of products derived from Russian crude. Jet fuel accounted for 84% of these imports, while diesel represented a further 15%. Imports of jet fuel and diesel from refineries processing Russian crude had already declined substantially before the UK’s ban was implemented. CREA tracking shows that the UK did not unload any shipments of jet fuel or diesel from refineries running partially on Russian crude between February and May 2026. Nevertheless, the continued exemption of these products means that the majority of oil products refined from Russian crude remain outside the scope of the new restrictions. The largest refinery that exported oil products made from Russian crude to the UK was India’s Jamnagar refinery, which accounted for 46% of the total, followed by the New Mangalore and Vadinar refineries. The UK has also unloaded shipments of bitumen from Turkiye’s Tupras Izmit refinery, a facility that remains a significant purchaser of Russian crude. Just before the UK ban came into force, a shipment of bitumen — a heavy petroleum product derived from crude oil refining, primarily used in road construction and roofing — was unloaded at the UK’s port of Avonmouth on 18 May 2026 from the Tupras Izmit refinery. Between March and May 2026, the Tupras Izmit refinery received 60% of its feedstock crude from Russia. Between December 2022 and May 2026, Thames Haven and the Isle of Grain unloaded the largest value of oil products from refineries running on Russian crude (EUR 1.4 bn each), followed by Bristol (EUR 0.9 bn), Milford Haven (EUR 0.4 bn), and Liverpool (EUR 0.2 bn). All other ports accounted for a combined EUR 0.2 bn. |

How are oil prices changing?

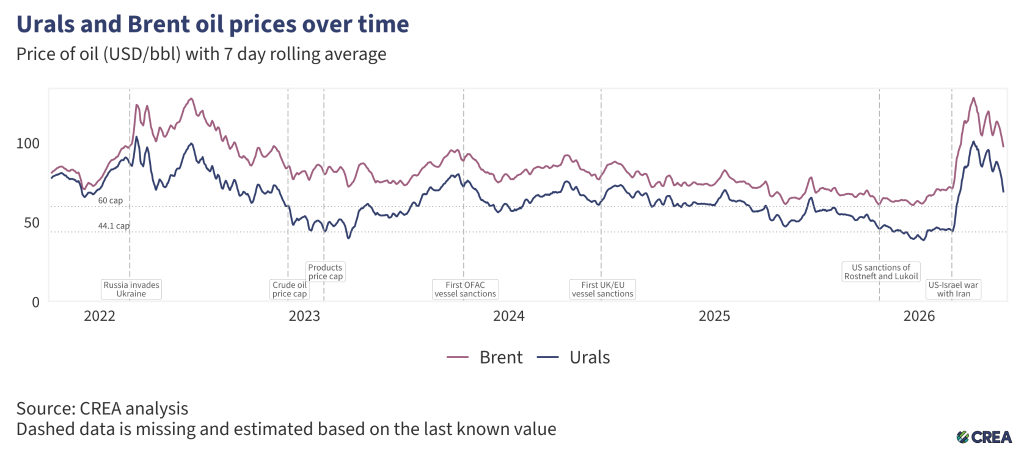

- In May 2026, the average price of Russia’s Urals crude fell by 12% month-on-month to USD 82.02 per barrel, remaining just under double the updated EU and UK price cap of USD 44.1 per barrel, which took effect on 1 February 2026.

- In May, the price discount of Urals-grade crude oil relative to the global benchmark Brent increased to around 25%. This is despite the current supply constraints affecting the global crude oil market.

| Notice: On 19 May 2026, we improved our pricing model for Urals crude oil with an aim to estimate free-on-board (FOB) value instead of over-the-counter (OTC) and contract for difference (CFD) financial instruments. This provides more accurate estimates of therevenues Russia receives from Urals crude exports. The new model lowered CREA’s estimate of Russia’s Urals crude revenue by 7.0% (11.6 EUR bn)1. While the previous model was not designed to estimate FOB values, the new model aligns much more closely with FOB market sources, reducing the mean absolute percentage error (MAPE) from 18% to 5.2% and reducing the mean signed deviation (MSD) from 9.3 USD/bbl to 0.1 USD/bbl.2 1. Figures are based on an internal review dated 13 May 2026 and may differ slightly from the final published estimates.2. When compared to market FOB market sources between April 2025 and March 2026. |

Sanctioned tankers carry the majority of Russian crude despite G7+ sanctions

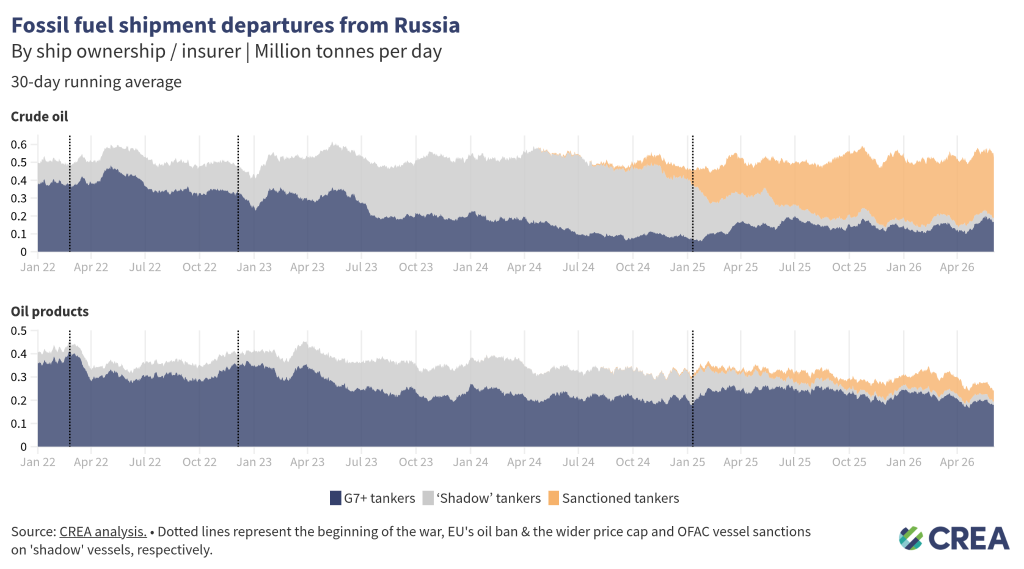

- In May 2026, 48% of Russia’s seaborne oil was transported by ‘shadow’ tankers under sanctions. A further 44% of the volume was transported by G7+ tankers. The remainder was transported by non-sanctioned ‘shadow’ tankers.

- G7+ tankers transported 31% of Russian crude oil exports in May, while non-sanctioned ‘shadow’ tankers accounted for 7% of the total. The largest share, 62%, was carried by sanctioned ‘shadow’ tankers.

- For oil products, Russia’s dependence on G7+ tankers is higher; these tankers transported 70% of Russian oil products in May. Sanctioned ‘shadow’ tankers carried 21% of total Russian oil product volumes, while non-sanctioned ‘shadow’ tankers accounted for 9% of the volume.

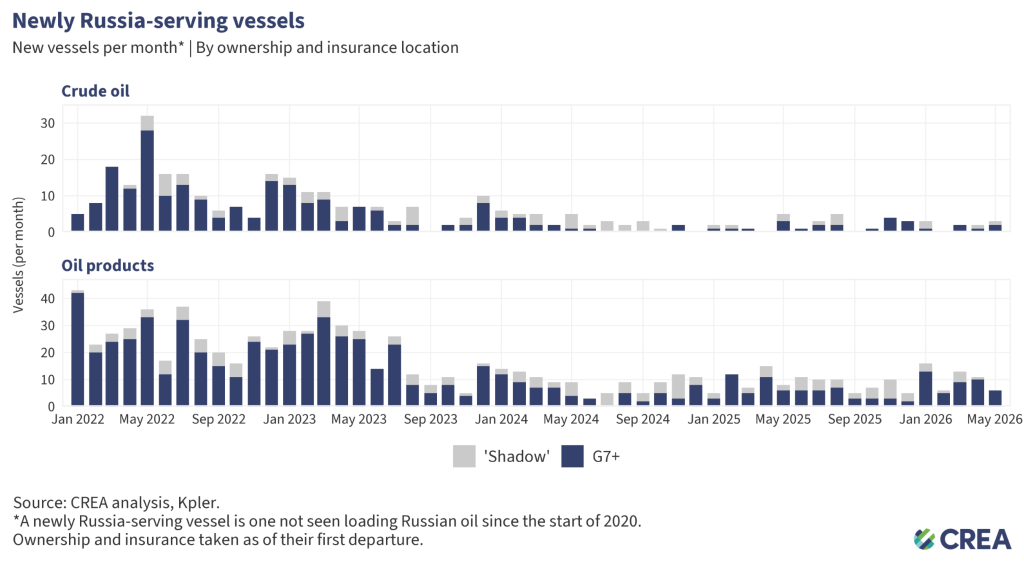

- In May, nine new vessels entered the Russian oil trade, none of which had loaded Russian oil at any point since the start of our analysis period in 2020. This total is marginally below the average over the past twelve months. Eight of these nine newly Russia-serving vessels were owned or insured by the G7+ at the time of loading.

- New Russia-serving ‘shadow’ fleet vessels (no ownership or insurance registered in sanctioning countries) have slowed to a trickle across 2026, with only one new ‘shadow’ fleet vessel shifting to serve Russian routes in May.

- In May 2026, six vessels transported Russian oil products for the first time since 2020, all of which were owned or insured in G7+ countries at the time of loading.

- In the most recent month, three tankers transported Russian crude oil for the first time since 2020, two of which were owned or insured in G7+ jurisdictions and one being a ‘shadow’ vessel.

- In May 2026, 43 ‘shadow’ vessels were operating under false flags at the end of the month. Two vessels (5%) appear to be idle, having not loaded any cargo in over a year.

- Of the 43 falsely flagged vessels, 11 have carried both Russian and Iranian oil, alternating between the two sanctioned trades. Four falsely flagged vessels most recently loaded Iranian crude or products and three loaded Venezuelan crude oil, pointing to a shared ‘shadow’ infrastructure that services Russia, Iran, and Venezuela interchangeably.

- A spell of inactivity rarely signals a return to legitimate trade. Of the false-flagged tankers that went idle for over a year and have since resumed loading oil, 16 of 23 came back still flying a false flag, most often switching to Iranian or Venezuelan cargo instead of Russian oil. Time spent idle under a false flag tends to precede a return to sanctioned oil rather than an exit from it.

- Eight vessels delivered EUR 368 mn of Russian crude oil and oil products while flying a false flag in May.

- All five vessels operating under a false flag that loaded crude oil or oil products in May departed from Russia’s Black Sea ports.

- In May 2026, two Russian ‘shadow’ tankers were reported as having been detained and inspected, compared with one tanker detained in April 2026.

- The Swedish Coast Guard boarded and detained the sanctioned ‘shadow’ tanker Jin Hui on 3 May near Trelleborg after determining that it was sailing under a false flag and raising concerns about its seaworthiness. The vessel’s captain was later arrested on suspicion of using false documentation.

- On 31 May 2026, the French Navy, supported by the UK, boarded and detained the sanctioned tanker Tagor in the Atlantic, west of Brittany, after it was suspected of using a false flag. Reports claim that the vessel may have been detained after authorities identified a discrepancy between its Automatic Identification System (AIS)-reported destination (Limbe, Cameroon) and its actual course toward East Asia, indicating deceptive routing practices commonly used to evade maritime sanctions and prompting direct enforcement action.

- Despite the UK Government’s announcement on 25 March that it had given permission to the British military to board sanctioned ‘shadow’ fleet vessels transiting UK waters, there were no reported detentions of Russian ‘shadow’ tankers by UK coastal authorities in May 2026.

‘Shadow’ tankers pose significant risks to ecology and the impact of sanctions

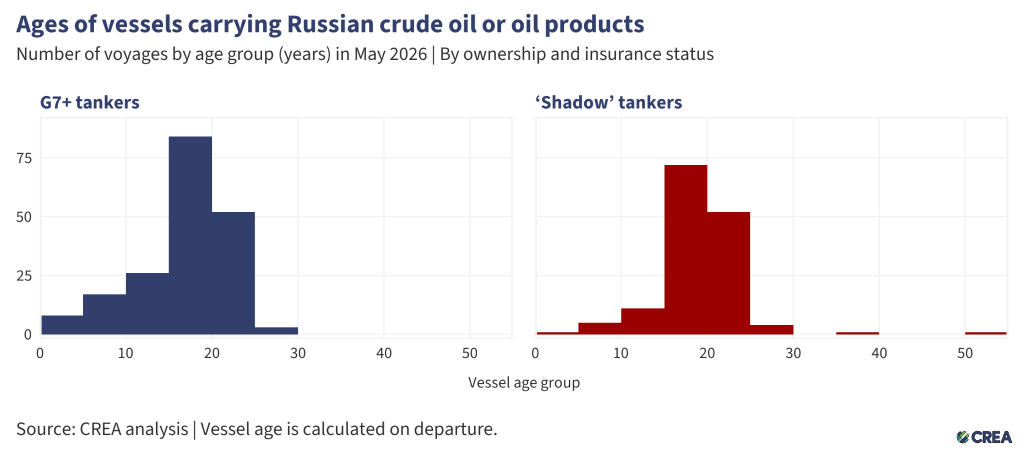

- In May 2026, 337 vessels exported Russian crude oil and oil products. Among them, 190 were G7+ owned or insured tankers, and the remaining 147 were ‘shadow’ tankers. Additionally, 39% (58 in total) of these ‘shadow’ tankers were at least 20 years old or older.

- Older ‘shadow’ tankers transporting Russian oil through EU waters pose environmental and financial risks due to their age, poor maintenance, and inadequate protection and indemnity (P&I) insurance. In the event of an oil spill or accident, coastal states may face significant cleanup costs and damage to their marine ecosystems.

- The cost of cleanup and compensation from an oil spill by tankers with dubious insurance could amount to over EUR 1 bn for taxpayers in coastal countries.

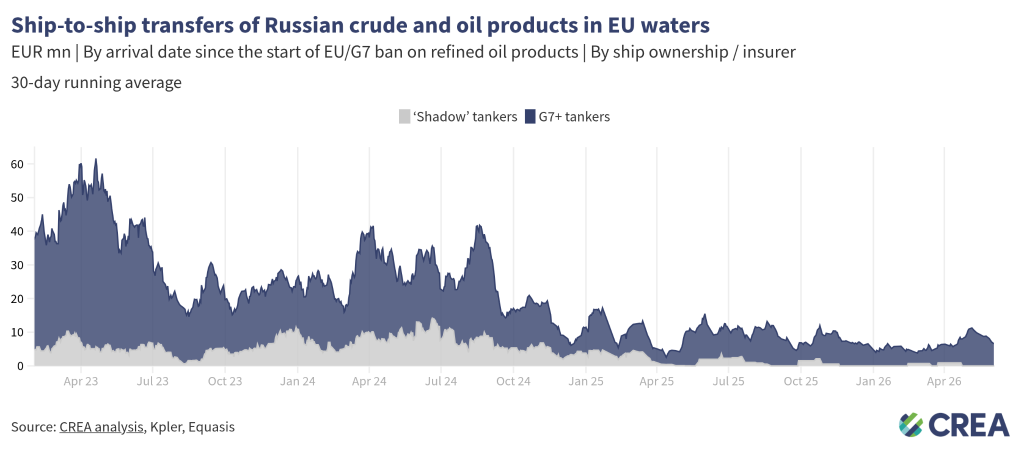

- In May 2026, an estimated EUR 140 mn worth of Russian oil was transferred via ship-to-ship (STS) transfers in EU waters.

- All STS transfers of Russian oil in EU waters were conducted in Cypriot (56%), Italian (26%), and Spanish waters (18%).

- Daily transfers averaged EUR 4.5 mn in May 2026. G7+ tankers conducted 100% of these transfers.

How can Ukraine’s allies tighten the screws?

Russia’s fossil fuel export revenues have fallen since the sanctions were implemented, subsequently constricting Putin’s ability to fund his full-scale invasion of Ukraine. However, much more should be done to limit Russia’s export earnings and constrain the funding of the Kremlin’s war chest.

Lower the oil price cap to a baseline that tightens Russian revenues

The oil price cap has failed to impose a durable constraint on Russian crude export earnings, working only briefly and selectively for Urals while leaving other grades and export channels largely unaffected. Urals prices have dipped below the USD 60 per barrel cap level (the crude oil price cap level was lower to USD 44.1 per barrel as of 1 February 2026) for mere short periods of time, while ESPO crude has consistently traded well above the cap due to its structural orientation toward China and Pacific markets.

G7+ sanctions have focused on Russian revenues rather than on restricting Russian export volumes — aimed at keeping Russian barrels flowing in global markets and easing fears of supply constraints. Policies such as the price cap are mainly aimed at reducing the price at which Russia could sell their oil.

In January 2026, as Russian oil prices fell sharply due to market oversupply, the EU proposed a ban on maritime services that facilitate Russia’s crude oil exports. Subsequently, in April 2026, the EU adopted its 20th sanctions package, which includes the basis for a future maritime services ban on Russian crude oil and petroleum products; however, it will be implemented only if an agreement is reached with the G7 and the Price Cap Coalition members. The maritime services ban would have, for the first time, targeted Russian oil export volumes and aimed at shrinking the tanker capacity required to transport Russia’s oil globally.

A massive spike in oil prices following the closure of the Strait of Hormuz has led to a rethink of this policy to avoid creating further supply crunches in global markets. Therefore, in the face of the current energy crisis of 2026, CREA recommends that the price cap coalition either fix the price cap policy to a base level that severely restricts Russian revenues or implement a value-based sanction, such as a tax on the use of Western maritime services for transporting Russia’s fossil fuels.

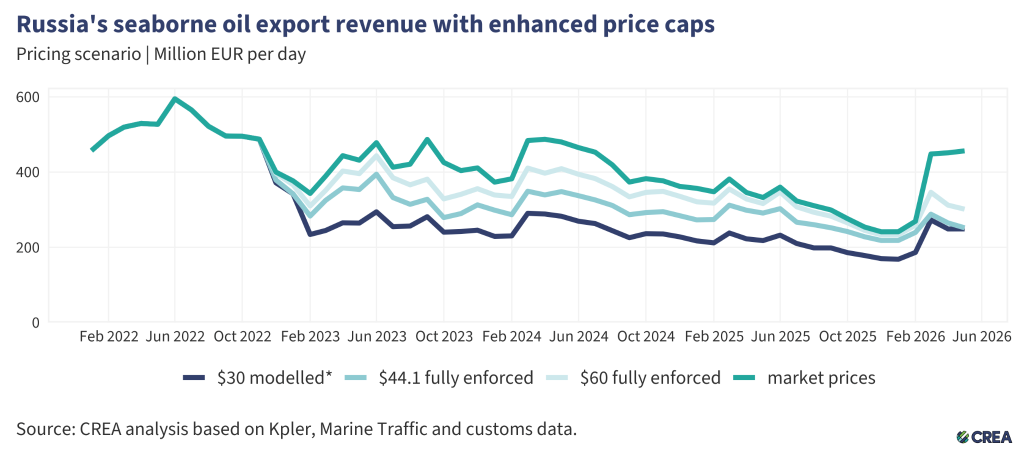

- For the price cap policy to achieve its desired impact, strong enforcement is key. In May 2026, full enforcement of the USD 44.1 per barrel price cap would have reduced revenues by 45% (approximately EUR 6.3 bn).

- CREA recommends that the price cap be set to a lowered level of USD 30 per barrel — still well above Russia’s production cost, which averages USD 15 per barrel. This price cap would have slashed Russia’s oil export revenue by 37% from the start of the EU sanctions in December 2022 until the end of May 2026.

- In May alone, a USD 30 per barrel price cap would have slashed Russian revenues by 45% (EUR 6.4 bn).

- Lowering the price cap would be deflationary, reducing Russia’s oil export prices and inducing more production from Russia to make up for the drop in revenue.

Create better enforcement mechanisms for the price cap policy

- Sanctioning countries must implement measures that address attestation fraud — a key enabler of non-compliance. Maritime insurers or vessel owners currently do not have direct access to the pricing information for the oil they insure or transport, and are reliant on attestation documents provided by oil traders for price cap compliance.

- At the same time, the majority of Russian crude oil is currently being traded by opaque entities located outside price cap coalition countries — such as the United Arab Emirates (UAE) and Hong Kong. These traders can fraudulently underreport the price that they paid to attain Western maritime services for the transport of Russian oil.

- Maritime insurers and oil traders must be required to obtain a bank statement showing that the Russian oil was traded below the price cap to avoid fraudulent attestation documents being produced. This bank statement must be verified by the bank itself to reduce the risk of the oil trader fraudulently producing documents. It would also enable maritime service providers to independently verify the price paid for the oil.

- As an alternative to amending and enforcing the price cap policy, sanctioning jurisdictions could utilise their leverage to tax Russia’s use of G7+ maritime services when transporting its fossil fuels.

Restrict the growth of ‘shadow’ tankers & tighten regulations targeting the refining loophole

- Frequent sanctioning of Russian ‘shadow’ vessels has shifted Russian oil back to tankers owned or insured in G7+ countries. Nonetheless, Russian ‘shadow’ tankers still hold sway on the transport of Russian crude oil. In addition, many sanctioned vessels continue to deliver oil to ports globally, with EU and UK sanctions in particular being frequently violated. Sanctioning countries must align their vessel lists and enforcement paradigms for a magnified effect on their operations.

- Maritime coastal states should intensify efforts to monitor, inspect, and detain ‘shadow’ fleet vessels that lack legal passage rights, such as unflagged, unlawfully idle, or security-risk vessels. Authorities must enforce and improve environmental and navigation laws within their territorial waters, investigating and boarding suspicious vessels when justified. Crews involved in criminal activity should face prosecution, and noncompliant ships and personnel should be subject to international arrest warrants.

- In its 18th sanctions package, the EU banned the imports of ‘oil refined from Russian crude’. The regulation bans imports from countries that are ‘net importers’ of crude oil. Net export status does not preclude the import and refining of Russian-origin crude, especially in jurisdictions with flexible or opaque crude sourcing practices. To close this enforcement gap, the exemption should be applied at the refinery level rather than the national level. Refined petroleum products should be subject to import restrictions if produced at facilities that have processed Russian crude within the past six months, regardless of the final product’s declared origin or the host country’s net export position.

- The exemptions for countries including the UK, the US, Canada, Norway, and Switzerland create an opportunity for oil products refined from Russian crude to be re-exported to the EU. This gap should be closed to ensure the sanctions are comprehensive and watertight. The EU should work with its partners to encourage them to also ban the importation of oil products from refineries running on Russian crude.

- Imports of oil products or petrochemicals from storage terminals or re-export hubs in non-sanctioning countries that have received a shipment of Russian oil in the previous six months should be prohibited from exporting to sanctioning jurisdictions. This aims to prevent re-export hubs from obfuscating the origin of imported Russian oil products that are then sent to sanctioning countries, such as in the suspicious cases observed in Turkiye and Georgia.

Stronger sanctions enforcement and monitoring of violations

- Despite clear evidence of violations, there is a need for stronger enforcement of penalties by agencies against shippers, insurers, and vessel owners. This information must be shared widely in the public domain. Penalties against violating entities increase the perceived risk of being caught and serve as a deterrent.

- Penalties for violating the price cap must be significantly harsher. Current penalties include a 90-day ban on vessels from securing maritime services after violating the price cap, a relatively minor sanction. If found guilty of violating sanctions, vessels should be fined and banned in perpetuity.

- The G7+ countries should ban STS transfers of Russian oil in G7+ waters. STS transfers undertaken by old ‘shadow’ tankers with questionable maintenance records and insurance pose environmental and financial risks to coastal states and support Russia logistically in exporting high volumes of crude oil. Coastal states should require oil tankers suspected of being ‘shadow’ tankers transporting Russian oil through their territorial waters to provide documentation showing adequate maritime insurance. Upon failing to do so, having been identified as a ‘shadow’ tanker, they should be added to the Office of Foreign Assets Control (OFAC), UK, and European sanctions lists. This policy could limit Russia’s ability to transport its oil on ‘shadow’ tankers, which are not required to comply with the oil price cap policy.

- To strengthen the integrity of maritime operations, the International Maritime Organization (IMO) must revise its guidelines to enhance transparency regarding maritime insurance. The IMO should mandate that flag states require shipowners and insurers to publicly disclose key financial information, including insurer solvency data, credit ratings from recognised agencies, and audited financial statements. Maritime authorities of coastal states should be legally able and encouraged to detain tankers that fly false flags and therefore pose environmental and security threats.

Relevant reports:

- Russian shadow fleet enabled by EU-linked insurers, investigators say

- From sanctions to shortages: Why is the UK softening sanctions on Russia | Ed Conway analysis

- UK waters down new Russian oil sanctions as fuel prices rise

- The EU wants less gas from Russia. But LNG imports are growing

- Warnings over Russian ‘blood oil’ as Asian fuel imports increase

- Local Gasoline Shortages: How Attacks on Russia’s Oil Infrastructure Affected the Fuel Market

| Note on methodology: This monthly report uses CREA’s fossil shipment tracker methodology. The data used for this monthly report is taken as a snapshot at the end of each month. The data provider revises and verifies data on trades and oil shipments throughout the month. We subsequently update this verified data each month to ensure accuracy. This might mean that figures for the previous month change in our updated subsequent monthly reports. For consistency, we do not amend the previous month’s report; instead, we treat the latest one as the most accurate data for revenues and volumes. Russia’s daily revenues for commodities used in this report are derived as an average, using CREA’s pricing methodology. The number of vessels with false flags per month is calculated using an end-of-month snapshot. In other words, for each month, vessels were counted if their most recent flag change at the end of the month was to a false flag. This does not account for the vessels with multiple false flag periods (switches between false flags and verified flags, or between different false flags), only the most recent flag status at the end of the month. To calculate the volume and value carried by false flags through EU waters, we filter for vessels that load from Russia’s northern and western ports (Ust-Luga, Primorsk, Vysotsk, St Petersburg, Murmansk, Arkhangelsk, Kaliningrad) in the current month and check whether they have transited the Danish Straits, the English Channel or the Straits of Gibraltar. We assume that falsely flagged vessels that have not transported a single cargo in the last two years are not operational and therefore exclude them from the analysis. CREA’s estimates of the impact of a revised and lowered price cap have been updated since February 2025. These numbers are a more accurate representation of the revenue losses Russia would incur. Our earlier numbers significantly underestimated the impact of a lower price cap due to a bug that we identified that mislabelled commodities in our model. |