Introduction

Price caps are meant to limit the economic rents a resource owner can extract from its asset base above a pre-established level. Assuming rational economic actors, price caps are expected to work if the supply of a commodity is relatively inelastic, i.e. the producer of that good cannot sustainably diminish the production or has few alternatives to sell its goods. Price caps work effectively as a tax applied to the supplier of a commodity and need to be carefully engineered so that the supply of that commodity is not affected, i.e. prices have to be above the marginal price of production to maintain the incentive to supply the good to the market.

Tax theory suggests that the impact of a price cap, used interchangeably here with tax, depends on the relative elasticity of supply and demand, more exactly on whether alternatives for sellers and buyers are better and available. Most of Russia’s sales of gas and oil to Europe were historically operated through pipelines conferring Russia little alternatives to sell the respective oil and gas elsewhere, which means that Russia’s supply is rather inelastic. At the same time, European oil demand is more elastic as oil can be imported through other means, mainly through ships. European gas demand is less elastic, but increasingly becoming so as alternatives to Russian gas are worked around at a breakneck pace. In 2021, 60% of Russia’s oil exports went to OECD countries. Redirecting this oil is a costly endeavor, as we see from current discounts at which China and India are lifting Russian oil. In 2021, 75% of Russian fossil gas exports went to OECD countries, mostly delivered through pipelines: this gas is impossible to divert in the short run to other destinations. Gas sent to China, a fraction of sales in Europe, is estimated to be 3 to 8 times less expensive than gas sold in Europe.

Supply and demand under price caps

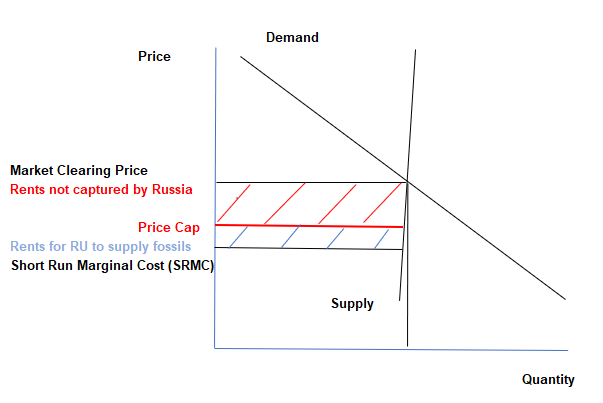

Our methodology to estimate the rents that would not have been captured by Russia in the presence of a price cap is informed by the microeconomics of commodities supply and demand, under the reality that Russia’s fossil fuel commodities supply is relatively inelastic as explained here. Every producer of a commodity has a short-run marginal cost of supplying that commodity below which it is uneconomical to supply that commodity. Coal, gas and oil supplied by Russia to global markets each have their own short-run marginal costs below which it is uneconomical for Russia to keep supplying them. A drop in Russian supplies in the short term would imply a significant increase in prices, all things equal, which will hurt emerging and developing economies at the same time. In order to avoid this, any price cap for coal, gas and oil needs to be set above Russia’s short-run marginal cost of production for that specific fossil fuel. As such, our methodology assumes these price caps are set slightly above the short-run marginal cost of Russia to deliver the fossil fuels as needed by markets. As exemplified in figure 1, the difference between the short-run marginal cost and the price cap allows for some rents to flow to Russia to incentivize the supply of said fossil fuels, which in the short run are demanded by world markets. This provides an economic incentive for Russia to continue the supply, albeit with limited rents. The difference between the price cap and the market clearing price consists of rents that would not be captured by Russia, which will not fund the war in Ukraine and can be used by governments imposing them to finance the reconstruction of Ukraine and for supporting those vulnerable to high energy prices.

Source: CREA analysis

Figure 1 – Supply and demand of commodities under a price cap

In practice, the current discounts at which Russia is selling the oil that is shunned by the European Union, United States and United Kingdom to China and India act as a variable price cap which Russia is willing to take on. These discou nts have varied between USD 37/barrel and USD 10/barrel versus Brent prices, suggesting that Russia’s short run marginal cost of producing a barrel of oil is significantly below USD 68/barrel. The fact that Russia is willing to sell its oil at these discounts is proof that price caps are highly likely to work as they incentivize willing offtakers to ask even higher discounts for lifting Russian fossil fuels.

Our assumptions

We assume that prices for all Russian fossil fuels carried aboard European-owned and insured ships, regardless of their destination, as well as for all gas imported into Europe, are capped at their average level in the first half of 2021. This has a moral basis in denying Russia the economic windfall resulting from its own energy blackmail, which started in summer 2021. Furthermore, as Russia’s fossil fuel exports in the first half of 2021 were at a high level, short-run marginal costs clearly are below these price levels, meaning that the price caps would slash profits but not make production unprofitable. The linked sources provide further evidence that the marginal costs for each fuel are below the price caps:

- Crude oil $75/barrel

- Oil products $79/barrel

- Pipeline gas EUR 31/MWh

- LNG EUR 43/MWh

- Coal $110/tonne

Potential downsides of price caps

The biggest issue relating to price caps is a potential uncontrollable price spike of fossil fuels, should Russia decide to stop delivering the fossil fuels the global markets need if price caps are enforced thoroughly. While this is in theory possible and can be enacted short-term, it would be very costly for Russia to maintain such a policy over a longer period, as the depletion of its fossil-fueled cash reserves will be dramatic and the technical issues surrounding the closing of fossil fuel production exceedingly costly longer term. Additionally, throttling supplies and the consequently high prices are likely to worsen the recessionary environment brought about by current high prices, which will crash medium to long term demand of Russia’s exports of oil, gas and coal.