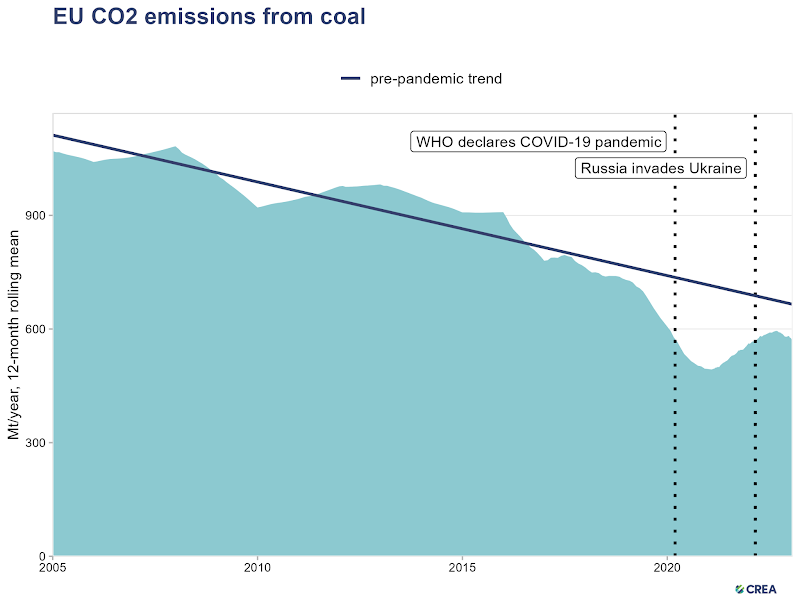

Coal consumption and CO2 emissions remained below pre-COVID levels and have been falling since September 2022

Many observers have suggested the EU is increasing fossil fuel, and particularly coal, consumption as a reaction to Russia’s war against Ukraine. However, data shows this is not true. In fact, consumption of both gas and coal have sharply fallen in the second half of 2022, and coal use in particular is set to fall further in 2023.

EU coal consumption and emissions plummeted in 2020 due to the COVID-19 pandemic. They started rebounding from early 2021 until summer 2022. Besides the rebound in electricity demand, coal consumption increased until summer 2022 due to a widespread drought that affected hydropower production, and serious but temporary technical issues at French nuclear power plants.

However, coal consumption and CO2 emissions peaked below their pre-COVID level, and both have been falling since September 2022. As hydropower and nuclear power operation normalize and more solar and wind power capacity comes online, coal consumption is set to fall further this year. The record-high fossil fuel prices caused by Russia’s decisions to cut supply to Europe have also resulted in a major increase

in investments in clean energy and strengthening of clean energy policies that will accelerate reductions in fossil fuel consumption in the coming years.

Data sources: CREA analysis using Eurostat monthly coal consumption data. For the most recent months for which Eurostat data is not available, ENTSO-E daily power generation data is used for power sector coal consumption and the trend in consumption outside the power sector is extrapolated. Non-power sector consumption is a small share of the total.

What caused the energy crisis

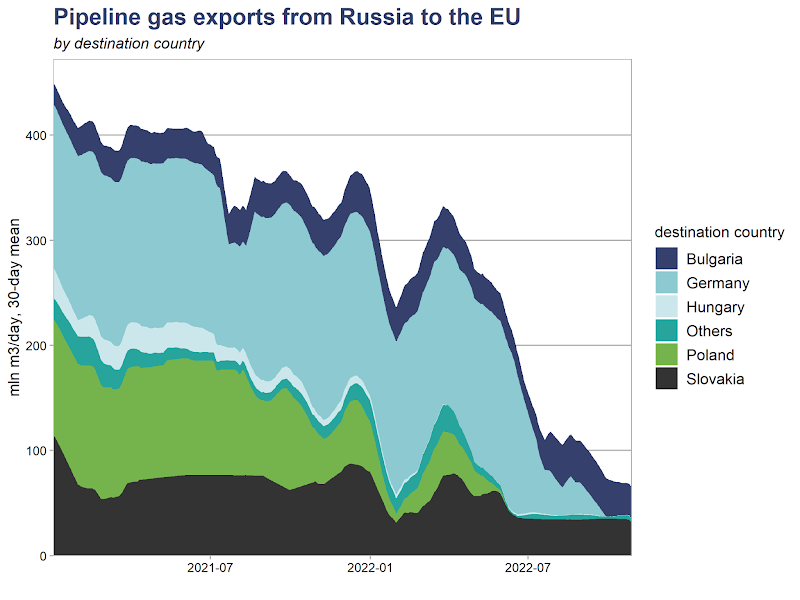

Starting in summer 2021, the EU has experienced an energy crisis. The crisis was caused by Russia’s decisions to limit gas supply to Europe in preparation for the invasion of Ukraine, and to further cut supply after the start of the invasion. The supply cuts came just as EU energy demand was rebounding from the drop caused by COVID-19. The reduced gas supply from Russia over the winter 2021–22 had led to very low levels of gas storage which made the situation more precarious.

Source: CREA analysis of daily data from ENTSOG transparency platform.

EU emissions and coal use increased in the first half of 2022, leading a lot of observers to draw a connection between the energy crisis and the increase. The growth in coal use and emissions however started already in early 2021, making it clear that the fundamental reason was the rebound in energy demand. In early 2022, several additional factors contributed to the increase in coal and gas demand: widespread drought, affecting hydropower production; historical heatwave in the summer, which boosted electricity demand; and a drop-off in nuclear power generation. Germany closed down three nuclear reactors, in accordance with the country’s nuclear phase-out plan, at the end of 2021. An even larger drop in nuclear power generation happened in France due to neglected maintenance of the country’s nuclear reactors and the discovery of stress fractures affecting the majority of the nuclear fleet.

None of these factors were structural and none of them were caused by the war or the energy crisis. They merely happened at the worst possible time in terms of Europe’s energy supply security. The only consistent bright spot throughout the summer and autumn was solar power generation, which set new records every month, easing the pressure on gas and coal-fired generation.

The figure below shows that both hydropower and nuclear power generation fell far below their levels in the preceding five years in 2022. As a result, both coal and gas-fired power generation increased year-on-year until August but started falling in September. In November, power generation from both coal and gas were at their lowest levels in at least 30 years.

Source: CREA analysis of daily power generation data from ENTSO-E transparency platform.

Following the gas supply cuts, the EU in turn banned the imports of coal from Russia in August and imports of crude oil in December 2022. As a result of the almost complete stoppage of fossil fuel imports from Russia, the EU increased imports from practically all other exporting countries, with policymakers paying a lot of attention on securing gas and oil supplies in particular. These imports were not covering for increased demand inasmuch as they were covering for the loss of supply from Russia. This “hunger” for fossil fuel imports, however, contributed to the impression that demand in the EU was increasing.

Another factor creating the impression of “return to coal” was decisions to re-activate mothballed coal power plants and extend the lifetime of some plants that were set to retire. In total, these decisions affected 26 power plant units. This back-up measure helped ensure the availability of capacity at some critical times but contributed very little to coal consumption, as the plants were on average operated at a utilization rate of 18%.

Why are emissions falling now?

The basic laws of supply and demand suggest that a dramatic reduction in the supply of fossil fuels, especially gas, will lead to an increase in prices and a reduction in demand. This is exactly what happened: as prices shot up, gas demand started falling significantly below the previous year’s levels in May 2022 and electricity demand in August 2022.

In other words, without the cutbacks to fossil fuel supply and the high prices, emissions would very likely have increased more and for a longer time.

The temperature-corrected data also shows that unseasonably warm weather connected to the warming climate is a contributing factor but not the main cause of lower demand.

CO2 emissions stopped increasing in July and have been falling since September. Besides the reduction in electricity and gas demand, the contributing factors are growth in wind and solar power generation, normalization of hydropower availability and progress in restoring nuclear power operation in France. Germany’s decision to extend the life of the country’s remaining nuclear reactors, which were set to retire at the end of 2022, also helps reduce coal and gas-fired power generation in the first quarter of 2023.

Emissions likely increased in calendar year 2022, due to the large rebound early in the year. There is still a long way to go to restore the full operation of the French nuclear fleet, which means that improved availability of nuclear power, together with increased capacity of solar and wind power, will help reduce emissions throughout 2023.

Both coal and gas fired power generation are falling. Gas has been falling faster, due to the extremely high gas prices. Therefore, there has been a shift from gas to coal in power generation in relative terms, but it’s misleading to call this a return to coal since coal consumption is falling too.

The energy crisis is accelerating the energy transition

The market response

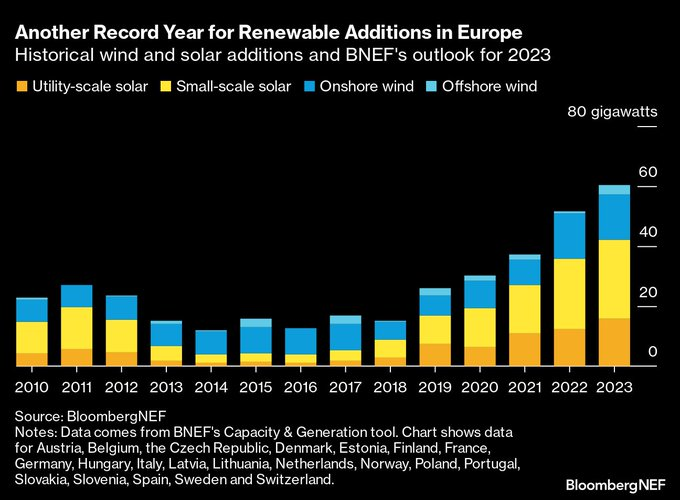

The security of supply implications of the fossil fuel crisis and the price implications of the broader energy crisis have resulted in forceful responses, both from energy markets and policymakers. Some of these responses may be observed as the spectacular growth in solar power, heat pump installations, as well as electric vehicle sales.

According to SolarPower Europe projections, nearly 40 GW of solar PV capacity was installed in Europe in 2022. This is a 45% gain compared to 2021 which itself broke a decade-long record in capacity installations. Solar is becoming an important source of energy in Europe, generating a record 12% (99.4 TWh) of EU electricity from May to August 2022, up 9% from the 77.7 TWh generated last summer. Thereby, solar power generation is just 4% points behind coal which currently produces 16% of the EU’s electricity.

The boom in solar power generation is widely spread across the Union, with 18 of 27 EU countries breaking their former records in solar power generation as a share of total electricity generation this summer. This is the result of multiple years of investment in solar, like Poland’s 26-fold increase in solar power capacity since 2018 and Hungary’s and Finland’s 5-fold expansions in the same period.

Europe’s installed solar power capacity was sufficient to substitute 210 TWh of fossil gas from May through August, the equivalent of 44% of the imports from Russia over that period in 2021. These imports would otherwise have cost the Union EUR 29 billion, and increased its vulnerability to Russian gas cuts. However, while solar is seeing a boom that raises the resilience of the European energy system, wind power is still being held up by restrictions and slow permitting processes in many countries despite the economics of wind power being highly favorable.

Even with high electricity prices, high and volatile prices for gasoline and diesel have made electric vehicles much more competitive and their sales volumes have increased since the beginning of the war. In the second quarter of 2022, which is the first full quarter after the war began, the sales of passenger EVs in Europe increased by 16% year-on-year. This comes on top of a 70% increase in 2021. In some markets, including the Netherlands, Sweden, and Norway, EVs already had a market share exceeding 50%, becoming the default option for new car buyers. In Norway, their share hit 85% of all passenger cars in the second quarter of 2022.Building owners are also scrambling to install heat pumps to reduce their energy consumption and reliance on gas in heating. This is mirrored in the European Heat Pump Association’s projection of a 30% increase in heat pump sales in 2022 compared to 2021 which itself saw a growth of 35%. Some of this growth is already apparent in Germany, where high gas prices have increased heat pump deliveries by over 50% in 2022, compared with 2021 which in itself was a record year.

The policy response

Supporting the market reaction is a host of EU and national policies promoting clean energy. The REPowerEU plan launched in May 2022 envisions that 45% of the EU’s energy mix in 2030 will consist of renewable energy, up from 40% in the earlier Fit-for-55 plan. This includes all uses of energy spanning from heating, transportation, industry, as well as electricity. Reaching the target will require the EU to install a total capacity of 1,236 GW of wind and solar by 2030, which is 16% higher than the 1,067 GW envisaged in the Fit for 55 strategy.

A report by Ember and CREA shows that the EU’s heightened ambition is supported by accelerated decarbonization plans in most EU member states. By June 2022, 19 governments had already announced plans to accelerate the green shift in response to the COVID-19 pandemic and Russia’s threat to their energy supply and security. In the power sector, these plans are set to deliver an 82% share of non-fossil energy sources in EU power generation by 2030, which is a substantial increase from the share of 74% projected following plans in place at the end of 2019. This means an almost complete phase-out of coal and a substantial reduction in the use of fossil gas in the power sector — the share of fossil fuels in EU power generation was 36% in 2021.

Overcoming bottlenecks that have suppressed wind power expansion in Europe is key to realizing these goals, and EU governments have announced plans to do so. One example is the “Wind-on-Land-Act” launched by the German government which seeks to overcome hurdles that have slowed the expansion of German wind power capacity over the past years. The act will allow wind power installation on 2% of Germany’s land area, and seeks to install 10 GW of onshore wind power capacity annually — almost five times more than the average installation over the years 2018–2021. Another example includes the agreement between eight EU countries bordering the Baltic Sea on increasing offshore wind power capacity seven-fold by 2030 to reduce their dependence on Russian energy. Such measures will contribute to a more energy secure Europe with less dependence on CO₂ emitting fuels and their insecure value chains.

Simultaneously, the EU and its member states are boosting their targets for energy efficiency and energy savings to directly cut the need for Russian gas. On the EU level, this includes heightening the Union’s energy consumption reduction target from 9% to 13%, meaning that the EU will cut its energy use by an additional 4% points by 2030 compared to the reference scenario. This target is complemented by several measures, including increasing the energy efficiency of buildings and installing 10 million new heat pumps in European households within the next five years. The German government has already embraced this approach, and has called upon the heat pump industry to ramp up production capacity to aid Germany to install 500,000 new units yearly from 2024.

EU emissions are not yet falling fast enough to align with climate targets but policies and market trends are moving in that direction. The key challenges are permitting processes, which in many EU countries are slow and cumbersome, particularly for wind turbines and for transmission lines; and input cost increases for equipment manufacturers which have led many of them to struggle despite strong market demand. EU policymakers are also concerned about the high degree of import reliance for some key raw materials and technologies that are central for the energy transition, such as rare earth metals, polysilicon and batteries. Policy proposals to address these issues are emerging.

In conclusion, the high energy prices and supply concerns have led to reductions in EU coal consumption and CO2 emissions. The rebound in coal and other fossil fuel use that was associated with re-opening and economic recovery after COVID-19 has ended, and coal use or CO2 emissions never rose above the pre-pandemic levels. They fossil fuel supply shock has also accelerated clean energy investments and the energy transition, leading to faster coal phase-down and emissions reductions in the coming years than previously expected.

| Author: Lauri Myllyvirta, Lead analyst at Centre for Research on Energy and Clean Air (CREA) |