China has the largest steel industry in the world, accounting for more than half of global production, making decarbonisation of the steel sector crucial to both achieving China’s climate targets and mitigating global climate risks.

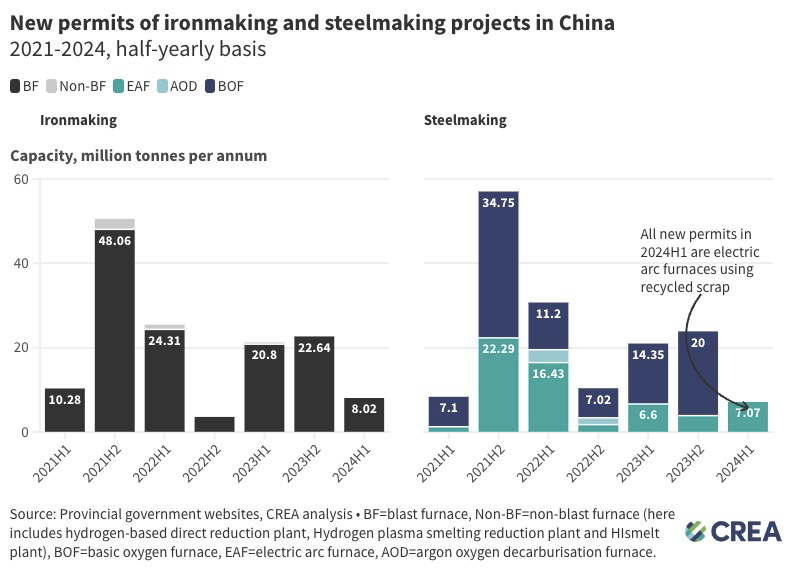

CREA tracks China’s steel decarbonisation progress with biannual reviews. Our 2023 H2 analysis revealed that steel sector decarbonisation in China had stalled in 2023. Our H1 2024 biannual review reveals a potential turning point for decarbonisation that emerged in the first half of 2024: no new coal-based steelmaking projects were permitted for the first time on a half-yearly basis since China announced its ‘dual carbon goals’ in September 2020, with new policies kicking in to support this trend.

Steel can be produced from iron ore in blast furnace–basic oxygen furnaces (BF–BOFs) using coal as fuel and reductant, or from recycled scrap steel in electric arc furnaces (EAFs). The steel sector in China primarily relies on BF–BOFs, which makes it the country’s second-largest CO2 emitter, following electricity generation. Yet, in H1 2024, only EAFs were permitted.

Key findings

- There were no new permits for coal-based steelmaking projects in the first half of 2024 for the first time since China announced its ‘dual carbon goals’ in September 2020.

- In the first six months of 2024, provincial governments permitted 7.1 million tonnes per annum of steelmaking capacity, all of which are electric arc furnace projects, which could signify a turning point for the Chinese steel industry in terms of halting new investments in coal-based steelmaking capacity.

- China could cut 200 million tonnes of CO2 from the steel industry by 2025, which would be a 10% reduction compared to the highest emission levels up to now recorded in 2020 due to measures to cut steel output and increase scrap-based secondary steel from electric arc furnaces.

- China’s forecasted CO2 reductions of 200 million tonnes by 2025 are equivalent to the annual emissions from the EU’s steel sector.

- As China’s steel demand peaks and more scrap becomes available, there is great potential to shift away from coal-based production, representing a significant opportunity for emissions reduction in the next 10 years.

Policy drivers

- China’s state planner has emphasised reducing carbon emissions from the steel sector in 2024-2025 in a recently released action plan, which aims to reduce a total of 20 million tonnes of standard coal and 53 million tonnes of CO2 emissions compared to 2023.

- Additionally, the action plan announced strict restrictions on exports of iron and steel products with high energy intensity but low added value. This could potentially limit the volume of Chinese steelmakers’ excess production sold overseas.

- Mandates from the central government have seen provincial governments laying out plans to cut steel production in 2024. Provinces with high steel production growth in 2023 and from January to May 2024 might face high pressure to cut their production, such as Anhui, Guangdong, Guangxi, Fujian and Inner Mongolia. The most affected steel mills will be those running blast furnace-basic oxygen furnaces (BF-BOFs) because of their high carbon intensity. Electric arc furnaces (EAFs) will be prioritised to ensure good production rates.

- The Chinese government has issued supporting policies to expand domestic scrap steel supply more rapidly in the coming years, including taxation and financial aid.

- The looming EU Carbon Border Adjustment Mechanism has accelerated efforts to improve carbon accounting measures and include the steel sector in China’s national Emission Trading Scheme, both of which have been central policy factors driving the decarbonisation of the sector.