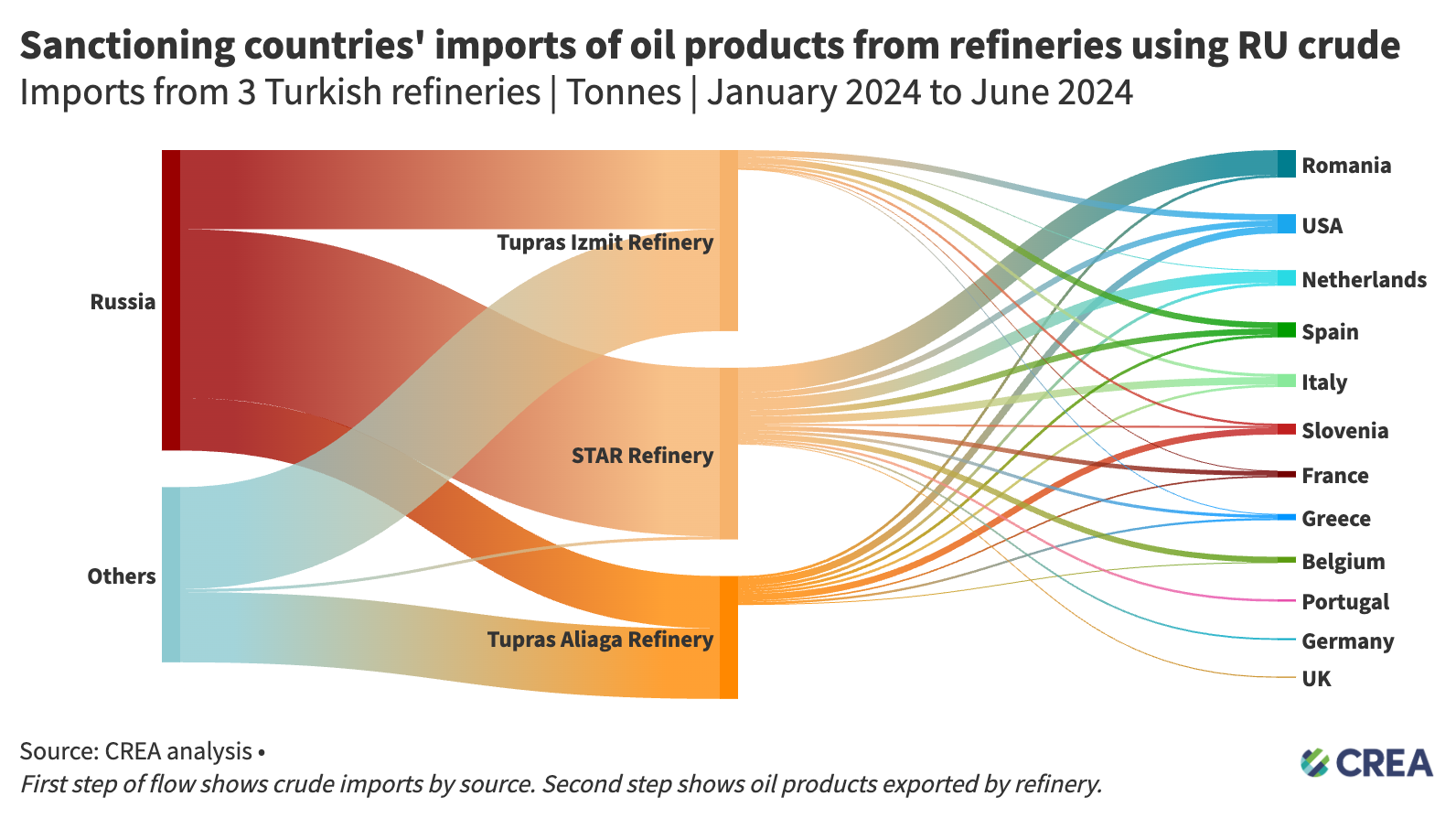

In the first half of 2024, Turkey has risen from being the 14th largest buyer of Russian crude oil before Russia’s full-scale invasion of Ukraine, to the third largest importer.

In the same period, three Turkish refineries have used EUR 1.2 bn worth of Russian crude to create oil products that are then imported by G7+ countries.

Imports of refined oil products from Turkey’s STAR Refinery, Tupras Izmit Refinery, and the Tupras Aliaga Izmir Refinery have generated an estimated EUR 750 mn in tax revenues for the Kremlin to finance its brutal war on Ukraine.

The Russian oil and gas sector is a crucial revenue stream for the Kremlin, contributing 32% to the federal budget in 2023, a decrease from 42% in 2022. Furthermore, the Kremlin allocated a third of all 2024 spending on the military.

The tax revenue received from imports by sanctioning countries of Turkish oil products made from Russian crude would enable Russia to recruit over 6,200 soldiers every month even after the new sign on benefits they are offering to those willing to fight in Ukraine.

G7+ countries have displayed little desire or political will to address the refining loophole and stop it since the beginning of Russia’s full-scale invasion of Ukraine. While the loophole goes unchecked, G7+ countries have actually increased their imports from non-sanctioning countries taking advantage of the situation by simply switching their supplier from Russia to third countries that are essentially functioning as Russian middlemen merchants. Having discovered that Western countries are not concerned about the origin of the crude used to create products for them, non-sanctioning countries have switched suppliers and are now heavily dependent on Russian crude oil and indirectly supply Russian coffers.

While the oil price cap and embargo did lower Russia’s oil export earnings by an estimated 14% in the second year of the invasion, the loopholes have allowed Russia to continue relying on its traditional Western markets and make up for the loss of revenues by selling larger volumes to third countries, who then sell derived products on to Western markets. The latter would not be possible if G7+ countries did not accept final products from the third country refineries and oil export terminals. By buying oil products from refineries that rely on Russian crude oil, G7+ countries are maintaining and even increasing demand and therefore boosting the price of Russia’s oil exports.

USA’s increased demand for refined oil products raises refineries’ demand for Russian crude oil

EU Member States’ imports of refined oil products from Turkish refineries remain the highest but it is the United States who is the second largest importer of refined oil products from these three refineries in the first half of 2024.

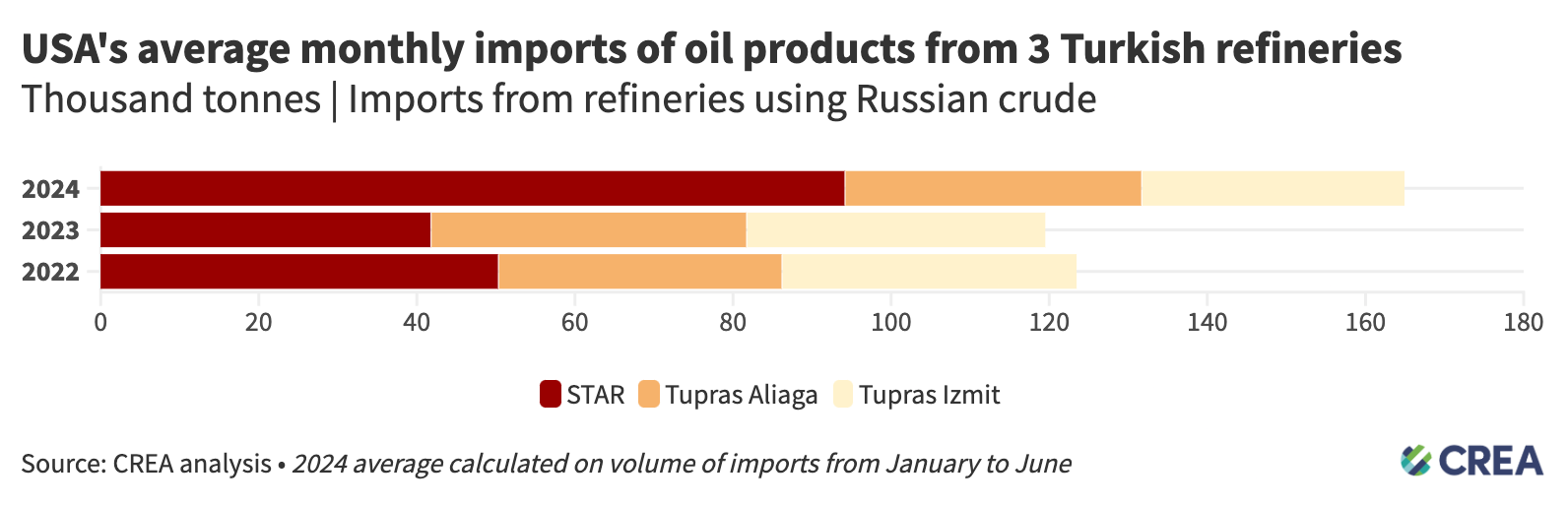

The USA’s imports from these refineries have risen an astronomical 335% year-on-year in the first six months of 2024, up to around 613,000 tonnes — already higher than their total oil products imports from them in 2023. CREA estimates that 386,000 tonnes of the imported refined oil products in the first half of 2024 were derived from Russian crude. These imports consist mostly of gasoline. The USA’s imports of gasoline from these refineries, estimated as being refined from Russian crude, could have filled up an estimated 338,782 American cars every month.

Key findings

- G7+ countries imported EUR 1.8 bn of oil products derived from Russian crude, from three refineries in Turkey in the first half (H1) of 2024.

- G7+ countries have grown their oil products purchases from these refineries by 62% year-on-year.

- Turkey expanded its dependence on Russian seaborne crude oil imports from around 34% in 2023 to 70% in the first half of 2024, taking advantage of a USD 5-20 per barrel discount for purchases of the Russian Urals crude blend.

- The Azeri owned STAR refinery is 98% dependent on Russian crude, with 73% of its crude imports supplied by the US sanctioned company Lukoil. 87% of its seaborne exports of oil products are directed to G7+ countries.

- The USA’s imports of oil products from Turkish refineries rose by more than three times year-on-year in H1 2024 and have generated EUR 125 mn in tax revenues for Russia.

- The USA’s H1 2024 imports of oil products from the STAR refinery have generated EUR 38.3 mn in revenues for the US sanctioned company Lukoil — the single largest crude supplier to the refinery.

- The USA’s H1 2024 Turkish imports of gasoline, estimated as being derived from Russian crude, could have fuelled an estimated 338,782 American vehicles every month in the same period.

- The total volumes of crude oil processed by Turkish refineries to export oil products to EU and G7 countries have secured EUR 750 mn in tax revenues for the Kremlin in the first half of 2024 alone.

Policy recommendations

- Ban imports from refineries using Russian crude: The first and most important step sanctioning countries should take is to ban the imports of oil products from refineries using Russian crude oil.

- Sanction Lukoil owned and operated refineries: The USA should also ban imports of oil products from refineries owned, operated or running on crude oil sold by the sanctioned Russian company Lukoil. Any purchases of refined products from refineries part-owned by Lukoil or from refineries running on Russian crude purchased from Lukoil are sending funds to a sanctioned entity that is closely related to the Kremlin.

- Low reliance will not impact domestic prices: Banning imports from these refineries or Lukoil supplied entities will not have any effect on oil prices or create any domino effect. For example, the USA’s purchases from STAR refinery constitute a mere 1% of its total seaborne imports of refined oil products. Banning these imports — from a refinery with huge imports of Lukoil crude — would have no effect on domestic prices or supply.

- Target wider network of Russian companies operating in Europe: The EU should also impose sanctions on the remaining Russian oil companies operating on the European fuel distribution market including affiliates and subsidiaries of Lukoil, Tatneft and Rosneft, which benefit from their intricate supply chains for the import of petroleum products made from Russian crude in third countries.

- Lower the price cap: Lowering the price cap would cut Russian revenues and would be deflationary, reducing Russia’s oil export prices and inducing more production from Russia to make up for the otherwise drop in revenue. A lower price cap of USD 30 per barrel (still well above Russia’s production cost that averages USD 15 per barrel) would have slashed Russia’s oil export revenue by EUR 62 bn since the sanctions were imposed in December 2022 until the end of July 2024. A USD 30 per barrel price cap would have slashed Russian revenues by EUR 3.51 bn in July alone.

| Methodology and assumptions CREA analysis is based on an array of different data sources including: Kpler, Eurostat, Comtrade, Equasis, P&I providers, Global Energy Monitor. Our estimation of refinery runs based on crude production regions is derived from Kpler. We assumed that the domestic consumption of oil products is the difference between the production capacity of the refinery and the total seaborne oil products exported. Estimating the value and volume of oil products made from Russian crude for export to G7+ countries We assume that all feedstock crude oil is perfectly mixed by refineries over the analysis period. For each refinery, we multiply the percentage of the feedstock crude oil that is of Russian origin to the total volume of oil products flowing out of the refinery. This allows us to attribute products as being derived from Russian crude. For example: if 30% of a refinery’s feedstock crude is of Russian origin, and the refinery exports 100 tonnes of diesel, we assume that 30 tonnes of the diesel comes from Russian origin crude. Similarly, we derive the volume of Russian crude used to make these products as the percentage of the refineries’ output being directed towards export multiplied by the volume of their imports of Russian crude. Our data on each refinery’s monthly output comes from the Turkish energy regulator’s reports. We combined this with CREA data on exports to G7+ countries of oil products from these refineries and each refinery’s volume of imports of Russian crude oil. CREA’s pricing model aggregates pricing data from a variety of different sources including Eurostat, UN Comtrade and OilPrice.com to derive monthly average prices of commodities. Read more about our pricing methodology here. |

| Calculating the number of American cars fuelled using gasoline made from Russian oil We estimated that the US imported 37,172 tonnes of gasoline from the three Turkish refineries using Russian crude throughout the first half of 2024. 23,418 tonnes of this was estimated as being produced from Russian crude. On average the US imported 3,903 tonnes of gasoline per month made from Russian crude from the three analysed Turkish refineries. 3,903 metric tonnes = 4,302.4 US tons (3,903 x 1,000/907.18) 1 US ton = 748.0519480519 gallons. 4,302.4 US tons = 3,218,425.9 gallons of gasoline The average US vehicle takes approximately 9.5 gallons of gasoline according to data from the American Petroleum Institute. Diesel & gasoline pricing We estimated the per unit pricing for imports of diesel and gasoline using European Union Member States’ import data from Eurostat. We eliminated any anomalous data — insufficiently representative of quantity or value — mainly of volumes below 500 kg for this analysis. Assumptions We assume that refineries perfectly mix the crude imported over the period of analysis, January 2024 to the end of June 2024, for the production of oil products. |