Russia’s illegal and brutal full-scale invasion of Ukraine started one year ago. Russia’s fossil fuel revenues have continued to enable the war even though they have declined.

In this briefing, the Centre for Research on Energy and Clean Air (CREA) highlights how Russia’s fossil fuel revenues have decreased, what the impact of the recent sanctions has been to Russia’s revenues, who is importing the fossil fuels that Russia is exporting, who is enabling this trade, and the leverage and options Ukraine’s allies have to further starve the Kremlin of fossil fuel revenues.

Key findings of the briefing

- Russia’s fossil fuel export revenues have fallen 50% below their 2022 peak in January–February 2023, with revenue from exports to the EU falling almost 90%.

- Yet, Russia is making an estimated EUR 560 mln per day on exporting fossil fuels.

- The key enabler of Russia’s ongoing export earnings and therefore the invasion is the European shipping industry. Ships owned or insured in the EU and the UK are carrying EUR 310 mln per day worth of Russian fossil fuels, 65% of the total value of Russia’s seaborne fossil fuel exports.

- The excessively high levels of the oil price caps as well as gaps in enforcement allow the Kremlin to continue to profit handsomely off fossil fuels transported and insured by the European shipping industry. Revising the price cap for crude oil to USD 30/barrel and for premium oil products to USD 35/barrel would cut Russia’s revenue by an estimated EUR 150 mln per day.

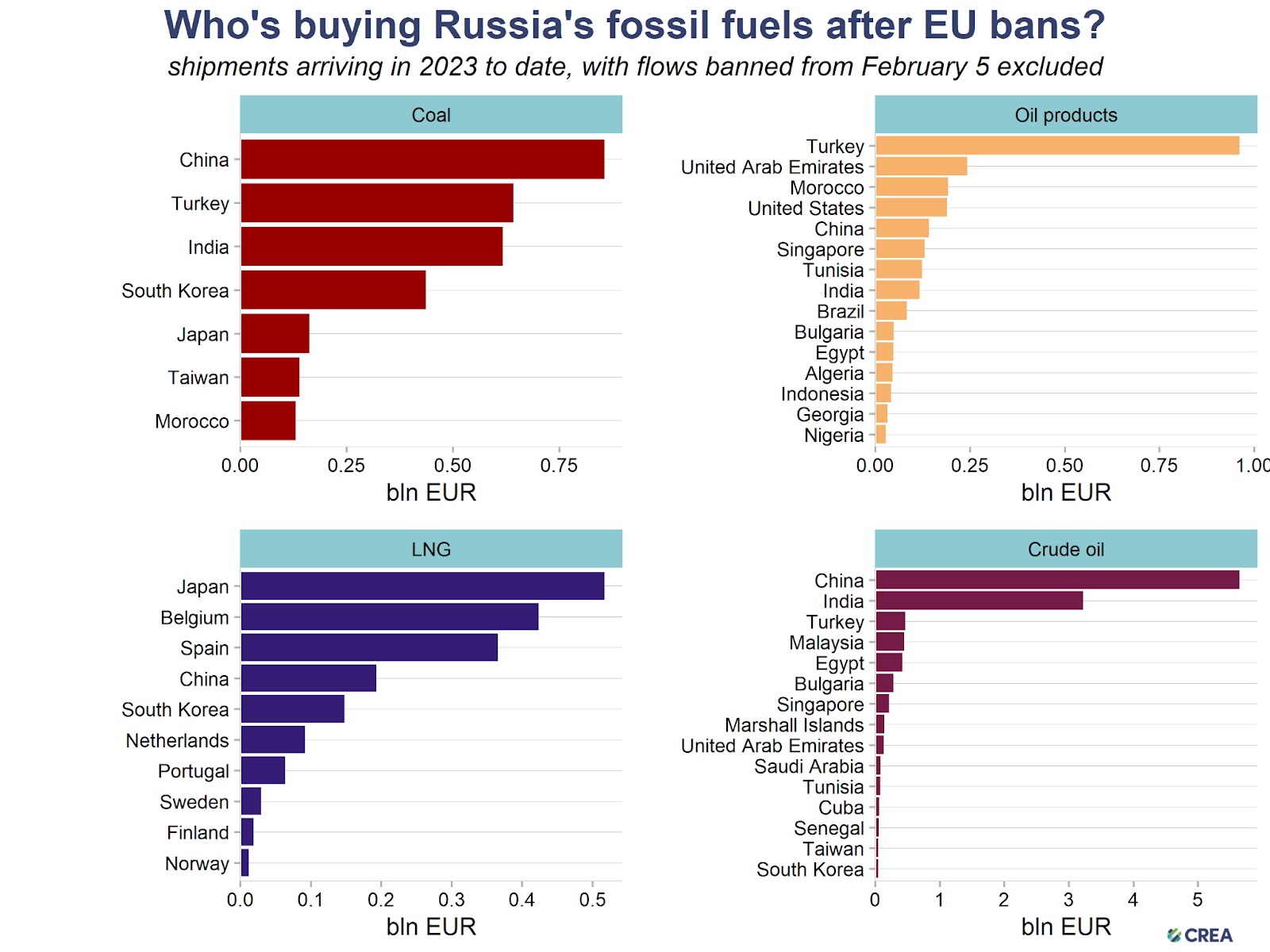

- The EU, Japan and South Korea continue to import approximately EUR 125 mln per day of oil, gas and coal from Russia. Restricting or placing price caps on these imports would be effective in squeezing Kremlin’s revenue.

Policy recommendations to cut the revenues feeding Putin’s war

The upcoming review of the level of the oil price cap in March is a prime opportunity for Ukraine’s allies to starve Putin’s regime of remaining fossil fuel revenues. We recommend lowering the price cap from its current level of USD 60 per barrel for crude oil down to a price level much closer to Russia’s low production costs which average an estimated USD 15 or less per barrel. Lowering the price Russia receives for their oil exports would deny the Kremlin of taxable revenues, while still incentivising continued supply. We recommend:

- Revise the oil price cap down to USD25–35 per barrel for crude oil and USD5 per barrel higher for premium refined products. This level substantially reduces Russian mineral tax revenues while keeping Russian oil production economically viable.

- Enhance monitoring and enforcement:

- permanently ban tankers that violate the price caps from entering EU and G7 ports or territorial waters.

- instead of relying on attestations, require copies of the underlying sales contracts. Alternatively, require either that payments be processed through an authorized intermediary, or that attestations can be allowed only from trading and financial entities on a pre-approved list established by the G7/EU sanction authorities to reduce the risk of fraudulent documentation.

- establish a dedicated Russian oil sanctions monitoring and enforcement authority that conducts regular monthly and extraordinary audits on attestations and other required paperwork.

- Introduce additional sanctions to limit Russian seaborne oil trade. These include:

- restrictions on the sales of tankers, to prevent Russia, its allies and related traders from acquiring old tankers to use to circumvent the cap.

- prohibit transhipment of Russian oil through territorial waters and exclusive economic zones of price cap coalition countries.

- require enhanced P&I insurance disclosure and review for any vessels not insured by the International Group when passing through the Danish Straits and other EU/G7 territorial waters or exclusive economic zones in order to ensure the enforcement of environmental norms for tankers in the Baltic and Black Seas.

- Institute price caps and/or import restrictions on pipeline oil and gas, and LNG coming to the EU from Russia.

- Introduce export restrictions on all software, technology and equipment used for the development, production and rehabilitation of oil and gas fields as well as coal mines.

- Address oil blending to ensure traded oil is not partly Russian, including through laboratory analyses and technical audits to check its origin.