Coal power plant permitting, construction starts and new project announcements accelerated dramatically in China in 2022, with new permits reaching the highest level since 2015. The coal power capacity starting construction in China was six times as large as that in all of the rest of the world combined.

This report from the Centre for Research on Energy and Clean Air (CREA) and the Global Energy Monitor (GEM) takes a closer look at China’s permitting of new coal power plants in 2022, the possible implications for China’s climate commitments, and provides policy recommendations.

The massive additions of new coal-fired capacity don’t necessarily mean that coal use or CO2 emissions from the power sector will increase in China. Provided that growth in non-fossil power generation from wind, solar and nuclear continues to accelerate, and electricity demand growth stabilizes or slows down, power generation from coal could peak and decline. President Xi has also pledged that China would reduce coal consumption in the 2026–30 period. This would mean a declining utilization rate of China’s vast coal power plant fleet, rather than continued growth in coal-fired power generation.

Even then, hundreds of brand-new coal power plants will make meeting China’s climate commitments more complicated and costly. The politically influential owners of the plants have an interest in protecting their assets and avoiding a rapid build-out of clean energy and a phase-out of coal.

While China is making rapid progress in scaling up clean energy, the country’s power system remains dependent on coal power capacity for meeting electricity peak loads and managing the variability of demand and clean power supply. The continued addition of new coal power capacity implies insufficient emphasis on overcoming the power system and power market constraints that perpetuate dependence on coal.The worst-case scenario is that the pressure to make use of the newly built coal power plants and prevent a steep fall in utilization leads to a moderation in China’s clean energy buildout, and/or the promotion of energy-intensive industries to consume the electricity. This could mean a major increase in China’s CO2 emissions over this decade, undermining the global climate effort, and could even put China’s climate commitments in danger.

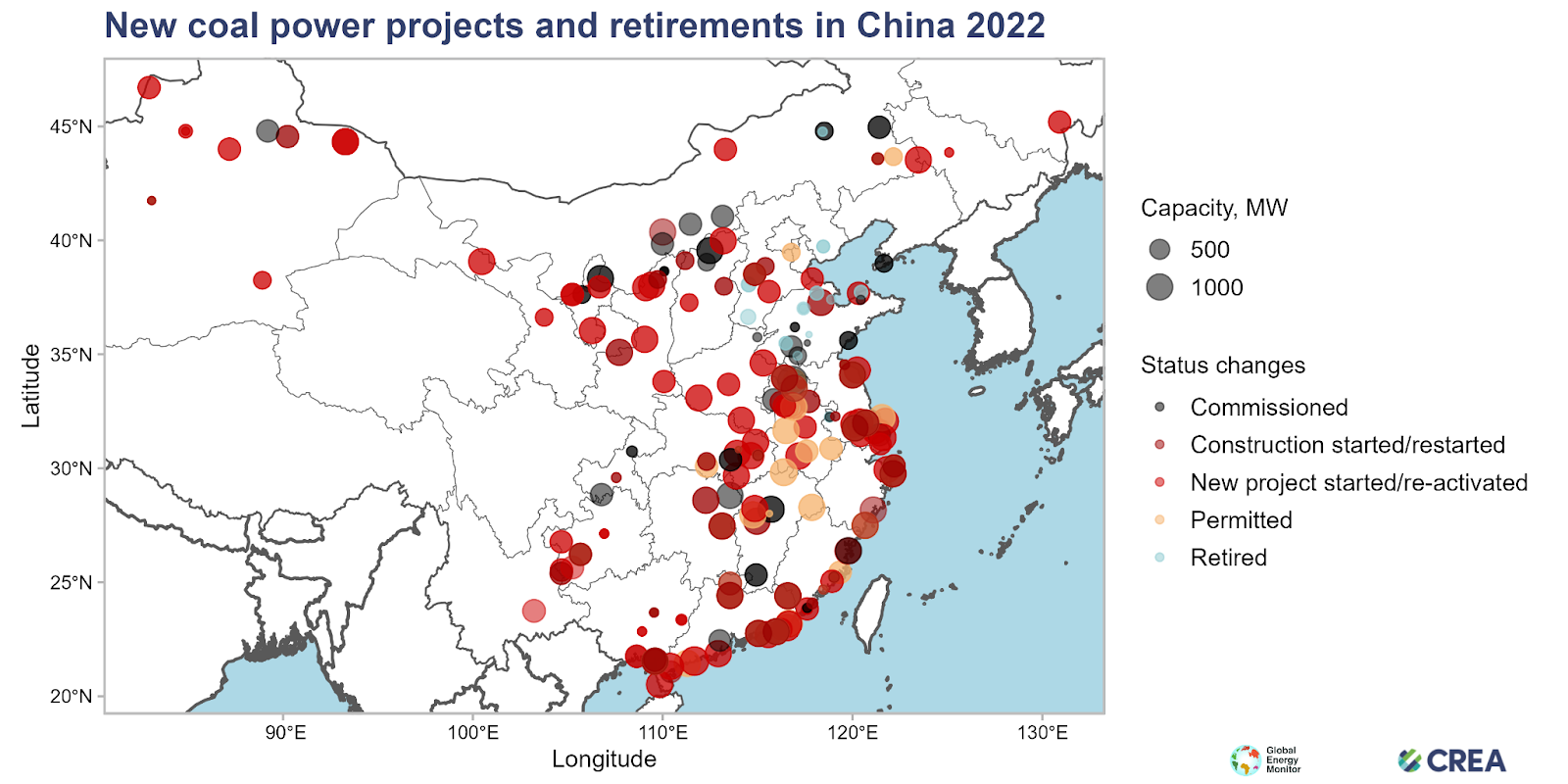

Key findings of the report

- Coal power plant permitting, construction starts and new project announcements accelerated dramatically in China in 2022, with new permits reaching the highest level since 2015. The coal power capacity starting construction in China was six times as large as that in all of the rest of the world combined.

- 50 GW of coal power capacity started construction in China in 2022, a more than 50% increase from 2021. Many of these projects had their permits fast-tracked and moved to construction in a matter of months. A total of 106 GW of new coal power projects were permitted, the equivalent of two large coal power plants per week 1. The amount of capacity permitted more than quadrupled from 23 GW in 2021. Of the projects permitted in 2022, 60 GW were not under construction in January 2023, but are likely to start construction soon, indicating even more construction starts in 2023. In total, 86 GW of new coal power projects were initiated, more than doubling from 40 GW in 2021.

- The largest amount of capacity moved ahead in Guangdong, Jiangsu, Anhui, Zhejiang and Hubei.

- New coal power capacity added to the grid kept steady from 26.2 GW in 2021 to 26.8 GW in 2022. These two years had the lowest annual additions since 2003, reflecting the lower level of construction starts around 2017–2020. Capacity additions will rebound in a few years when projects that broke ground last year begin to come online.

- China has seen a rapid increase in electric peak loads in 2021–2022, with the highest recorded momentary load increasing by 230 GW, due to an increase in the prevalence of air conditioners and exceptionally intense heat waves. This is prompting an increase in coal power plant development as a costly and sub-optimal solution, especially in major electricity demand centres and provinces neighboring them.

- Of China’s six regional grids, the South and East grid are the only ones that don’t suffer from a clear thermal power overcapacity problem. Yet, 50% of newly announced projects and 40% of construction starts took place in the grids with overcapacity.

- The provinces permitting a large amount of new coal power plants try to justify the projects as “supporting” power capacity to ensure grid stability and the integration of renewable energy. This justification doesn’t hold water, however, as the plants are intended to run at baseload utilization, and these specific provinces are laggards in growing clean energy generation to meet their demand growth.

- Avoiding the need for more coal-fired power plants requires improvements in energy efficiency, demand response and investments in storage, as well as improving grid operation.

- Plant retirements slowed down further in 2022, with 4.1 GW of coal-fired capacity closed down in 2022, compared with 5.2 GW in 2021. Policies on closing down small and inefficient plants have been revised to keep these plants online instead as back-up or in normal operation after retrofits.

Policy recommendations

- Strictly control new coal power capacity and reject or revoke permits to projects that are not necessary for “supporting grid stability” or “supporting the integration of variable renewable energy”.

- Accelerate investment in clean power generation to fully meet growth in electricity demand and stop increasing bulk power generation from coal. Decarbonisation requires substantial changes in network infrastructure, market mechanisms, regulatory framework, and planning processes, which require central government facilitation.

- Increase investment in electricity storage, flexibility and transmission within grid regions. Create a level playing field for different storage, demand response and generation technologies for meeting peak demand, and enable clean flexibility technologies to scale up. While many technologies, such as pumped hydro, lithium-ion battery and demand-side technologies, are as mature as coal power and ready for wider adoption, current power systems and policy frameworks still lead developers to default to coal.

- Strengthen energy efficiency requirements for A/C units and for new buildings, and introduce a program of large-scale energy efficiency improvements for existing buildings.

1 The size of coal-fired power generating units varies widely; the actual number of permitted units was 168 at 82 different plant sites.