In the years following the landmark Paris climate agreement, most countries have made progress in phasing out coal-fired power—but nowhere near fast enough, and much of the progress has been offset by even larger planned expansion in China. This is shown by new CREA analysis included in the new report Boom&Bust 2021 released today.

If there is one decisive test of the global efforts against climate change, that’s phasing out coal-fired power generation. Reductions in coal use make up the vast majority of the difference between energy futures that lead to potentially catastrophic climate disruption, and those that succeed in limiting warming to the more survivable levels that countries agreed to target in the Paris agreement.

In the years since the agreement, 13 countries have made a decision to phase out coal by 2030, compared with just two that had such a commitment before.

| Country | Phaseout year | Decision year |

| Belgium | 2017 | 2010 |

| Portugal | 2021 | 2019 |

| France | 2022 | 2016 |

| United Kingdom | 2024 | 2015 |

| Italy | 2025 | 2017 |

| Ireland | 2025 | 2018 |

| Greece | 2028 | 2019 |

| Netherlands | 2029 | 2018 |

| Finland | 2029 | 2019 |

| Canada | 2029 | 2019 |

| New Zealand | 2030 | 2017 |

| Denmark | 2030 | 2017 |

| Israel | 2030 | 2018 |

| Slovakia | 2030 | 2019 |

| Hungary | 2030 | 2019 |

| Germany | 2038 | 2020 |

In 2018, following the release of the IPCC 1.5 degree Special report, Global Energy Monitor and Greenpeace developed coal phase-out pathways consistent with the projected coal-fired generation in the IPCC scenarios for holding global warming to 1.5 degrees.

Two times a year, Global Energy Monitor releases an extremely detailed compilation of everything we know about every coal-fired power plant unit in the world. A report on the latest iteration of the data, reflecting the situation at the end of 2020, was released today, including a CREA analysis of the progress, and lack thereof, in phasing out coal globally.

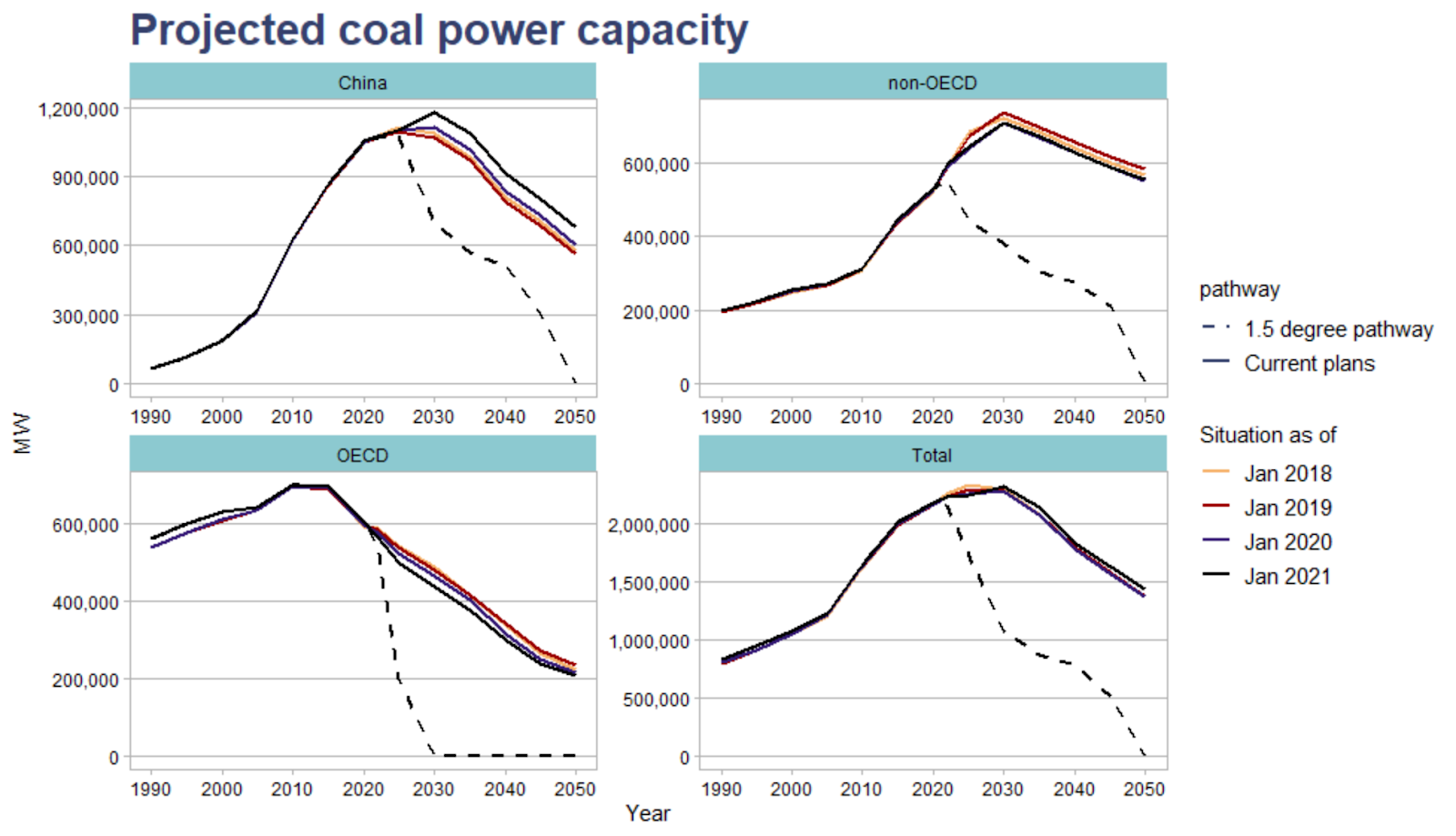

We used the versions of the database released in January 2018, 2019, 2020 and 2021 to see how the outlook for global coal power capacity has changed, and track progress towards phasing out unabated coal in line with the 1.5 degree pathway. These projections are not realistic economic-financial scenarios but rather illustrations of what would happen if all new coal power projects are realized, and existing power plants are retired following operator announcements, national phase-out decisions and, in the absence of those, the regional practice to date.

Both OECD countries and non-OECD countries, with the exception of China, have made modest progress in aligning their plans for coal power retirement and newbuild with the 1.5 degree pathways. The graph below looks at the expected coal power capacity in these regions based on announced national phase-outs and business-as-usual retirements of old plants, as well as projects under construction and planned capacity coming online over the next 10 years. Despite the modest progress outside China, no region is close to meeting the required reductions for the 1.5 degree pathway (dashed line).

At the end of 2018, OECD’s coal power capacity stood at 670 GW, and was expected to fall to 523 GW by 2030. By the end of 2020 (blue line), national and operator phase-out decisions in OECD countries have seen projected coal capacity in 2030 fall by 74 GW, to 449 GW. Although a reduction, the 1.5 degree target requires a complete coal power phase-out in OECD countries by this date. The OECD countries with largest projected coal power capacity in 2030 are the U.S., Turkey, Japan, South Korea, Poland, Germany and Australia. Out of these, Turkey and Japan are still planning a sizable coal power expansion.

The projected 2030 coal power capacity in non-OECD countries excluding China has fallen by 29 GW since 2018, with the largest reductions taking place in India (50 GW), Egypt (13GW) and Vietnam (3.5 GW)—although Vietnam’s future capacity is expected to fall further once its latest energy plan is finalized. Remarkably, the projected capacity in the Africa and Middle East region fell by 24 GW. The largest increases took place in Indonesia (10 GW) and Bangladesh (8 GW), with further reductions expected this year.

New coal power projects initiated and restarted in China since 2018 mean that the country’s projected coal power capacity increased by no less than 112 GW, more than offsetting the reductions in the rest of the world. As a result, the world as a whole is not much closer to the 1.5 pathway than it was two and a half years ago.

Globally, the projected coal-fired capacity in 2030, if all proposed projects are realized and retirements aren’t accelerated further, is almost 2400 GW, while the amount of capacity consistent with the IPCC 1.5 degree pathways would be 1100 GW. An additional 1300 GW will need to be cancelled or retired: 450 GW in the OECD, 500 GW in China and 400 GW in the rest of the world, to meet the emission budgets consistent with limiting global warming to 1.5 degrees.

CREA compilation of data on new coal power projects in China from Polaris Network indicates that permitting has slowed to a trickle in the first quarter of this year, with only 1.6GW of capacity given a green light, after a scathing environmental inspection of the National Energy Agency, criticizing out-of-control coal power expansion in the country’s air quality priority provinces, and numerous calls from the country’s top leadership for low-carbon development. However, a very large number of projects, totaling 11GW, have started feasibility studies, and 21GW of already permitted projects have issued calls for tenders or entered construction. There haven’t been any indications of cancelling or suspending the permits to projects that the environmental inspector said should not have been issued. This makes it seem that local officials are waiting for guidance from the top, while project developers are plowing ahead at full steam.

Details of the methodology

We projected the development of coal-fired capacity assuming that all coal power projects in active development are realized, and retirement of plants that don’t have an announced retirement date and are not covered by a national phase-out follows the practice in each region to date, based on average age of coal power plants at retirement, or the 90th percentile of the age of operating plants, whichever is greater. For new projects without an announced commissioning date, we spread commissioning over the next 10 years, differentiating by the current status of the project. The projections incorporate national phase-out decisions included in the Europe Beyond Coal Coal Exit Tracker, as well as those by Powering Past Coal Alliance members.