On December 5, the EU will be taking by far its strongest measure to date to curtail fossil fuel imports from Russia and target the country’s export revenue, much of which goes to fund the illegal and barbaric invasion of Ukraine. On that date, the EU’s ban on seaborne crude oil imports enters into force. The original plan was to ban the use of European-owned ships for the transport of Russian oil at the same time, but this will now likely be replaced by an oil price cap mechanism, that only allows the use of European-owned ships if oil is sold under the price stipulated by a cap. The crude oil ban will be followed on February 5, 2023 by a ban on the imports of refined oil products.

This leaves Russia with two options: comply with the price caps or try to find buyers for its oil exports outside of Europe, and tankers to carry them.

Russia’s federal budget in deficit and widespread reports of mobilized soldiers being required to buy their own equipment, it’s clear that money is already a constraint on Russia’s ability to continue and escalate the invasion. Effective steps to curtail revenue will have an impact.

With less than six weeks to go, the key question is whether Russia will be able to work around the EU oil import ban. While the common fear for policymakers has been that the ban would be too effective, slashing oil supply to the world market at a time when the market is already tight, there are now analysts suggesting that Russian exporters will be able to “largely” replace European demand and shipping capacity.

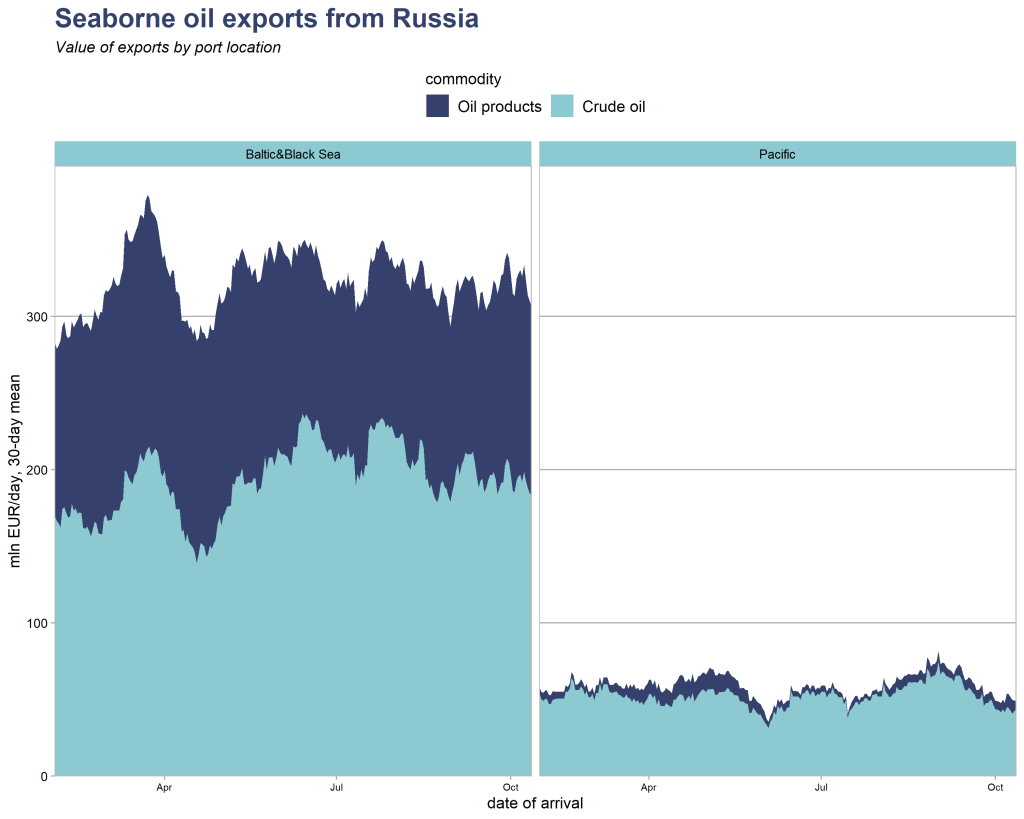

First of all, Russia’s oil exports are divided into two markets: the “Atlantic” market supplied by ports in the Baltic Sea and Black Sea, and the Pacific market. Essentially all oil shipped out of Pacific ports goes to China, while the vast majority of the oil gets to the market on the Atlantic side. Oil from Atlantic ports makes its way to the EU, Turkey, the Middle East and India, occasionally as far as Malaysia, but it’s a very long way from the Gulf of Finland to China. There is also no scope to shift exports to the Pacific, as the infrastructure is already at capacity. This is evidenced by the fact that there has been no shift even if China would presumably have been a willing buyer:

Finding new buyers has required discounts of 25-35% on Russian oil, compared with international market prices. As the Russian state makes money on the margin between production cost and sales price, the impact on state revenue has been even more significant. Speeding up the shift and persuading new buyers to take on more will require larger discounts.

The graph above also shows that while crude oil exports have shifted, oil products have been a lot more tardy. The crude oil ban on Dec 5 will have a significant impact, but the oil products ban on Feb 5 seems potentially even more impactful. Product tankers are smaller and the market is shallower so diverting exports will require even bigger discounts.

Most importantly, as we’ve been emphasizing, shipping is the real achilles heel of Russian oil exporters. Shipping oil longer distances to India or Malaysia requires more ship capacity, and Russia has made no progress in tapping non-European capacity for this: 50% of Russian oil, regardless of departure port and destination, continues to be carried on European-owned ships, and 70% on European-insured ships.

In terms of dependence on European-owned and insured ships, Russia has been making hardly any progress at all. It’s highly likely that Russia won’t be able to replace all the Europe-linked ships that are currently carrying Russian fossil fuels by Dec 5 without prices falling below the targeted caps, one way or the other.

The importance of the price caps was shown by our earlier analysis finding that applying the caps would have slashed Russia’s revenue from fossil fuel exports by EUR 14 billion, even under very conservative assumptions, between July and September.

Russia will likely never admit it is complying with oil price caps, but if the shipping ban is implemented effectively, the discount on Russian oil is likely to widen so much that it gets sold under the price cap level regardless. India, Turkey or Malaysia won’t overtly comply either.

Our assessment of the oil and tanker markets could of course prove wrong. Something much more fundamental is happening, however. With the oil and coal bans, and Russia’s shutting off of gas pipelines, we’re getting close to cutting off Europe’s energy dependence on Russia. That changes the game.

The EU’s initial sanction efforts were characterized by a balancing act between trying to maximize the economic impact on Russia while preserving the access to Russian fossil fuels. Once this concern is off the table, the gloves can come off.

If the shipping ban turns out not to be effective enough, what the EU and G7 should do is ban all ships that touch Russian fuels from entering any of their ports, forever. That would get around the concerns that vessel ownership could just be shifted to other jurisdictions. A vessel taking on Russian fuels would immediately lose a major share of its commercial and aftermarket value, as tankers need to be able to take on orders from any port to maximize their utilization.

All the carve-outs and exemptions that were left in EU sanctions in order to keep oil and gas flowing should be revisited. This includes technology, spare parts, maintenance, support and financial flows.