Despite the EU/G7 countries’ sanctions on Russian oil, a majority of vessels carrying Russian oil and oil products are owned and/or insured in the EU and G7 countries. Before the war, Putin was incredibly reliant on Western owned or insured tankers to transport Russian oil globally. Despite the strong set of tools to cut revenues for the Kremlin’s war chest, EU/G7 countries have allowed the proliferation of the Russian oil trade by insuring tankers transporting Russian oil.

CREA analysis has found that the UK — the largest insurer of seaborne Russian oil globally — insured ships that transported Russian oil worth EUR 120.6 bn from March 2022, just after Russia’s invasion of Ukraine1, until the end of November 2023.

Key Findings

- In the 12 months since the oil price cap (5 December 2022), EUR 46.4 bn of Russian oil has been transported on tankers using UK protection and indemnity (P&I) insurance.

- 33% of all Russian oil (by volume) was transported on tankers insured in the UK since the sanctions were implemented until early November 2023.

- A majority of the Russian oil carried by tankers insured in the UK was crude oil (31% worth EUR 14.4 bn), followed by diesel (22% worth EUR 10.3 bn).

UK insurance’s role in transporting Russian oil

While there has been a decrease in insurance companies from the UK covering shipments of Russian crude, Russian oil still remains highly reliant on vessels insured in the UK for transport. Russia is also heavily reliant on tankers that are owned or insured in countries that implement the oil price cap policy although this trend has decreased since Russia’s invasion of Ukraine. In December 2023, 62% of Russian oil products, chemicals, and liquefied petroleum gas (LPG) were carried on tankers owned or insured in countries that implement the price cap policy.

CREA’s analysis found that 33% of all Russian oil (by volume) was transported on tankers insured in the UK since the sanctions were implemented until early November 2023. In November, ships insured in the UK transported EUR 3 bn of Russian oil products, with vessels shipping crude oil accounting for EUR 803 mn of the total.

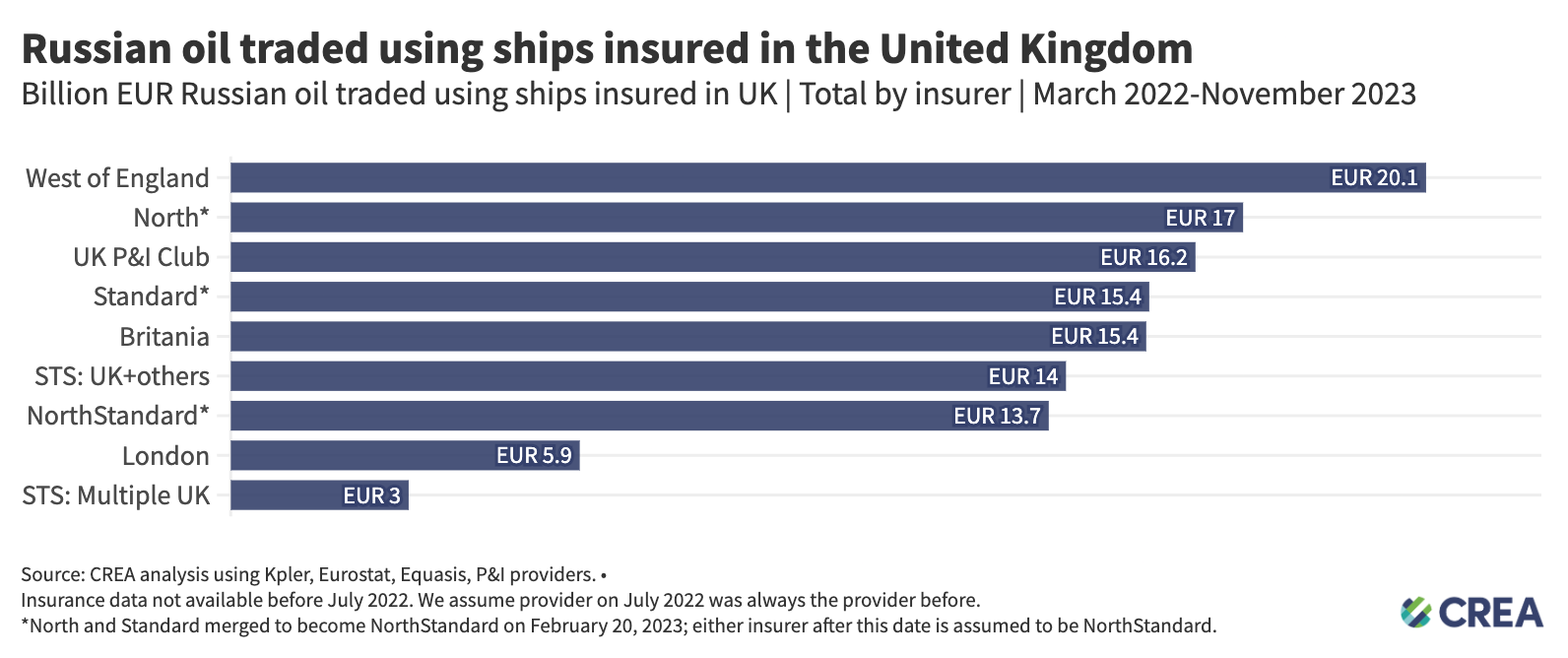

Ships insured by West of England Protection & Indemnity (P&I) Club covered the highest value of Russian oil products between March 2022 and November 2023 (EUR 20.1 bn). While their insurance for tankers transporting Russian oil has marginally dropped by 8% in the 12 months since the sanctions, ships insured by them have transported Russian fossil fuels worth EUR 9.8 bn, of which 37% (EUR 3.6 bn) has been Russian crude.

In November alone, ships insured by West of England transported EUR 892 mn worth of Russian crude and oil products, which was 29% of the total oil transported by UK insured ships that month.

North and Standard insurance merged to become NorthStandard in February 2023. Since then, the company has insured EUR 13.7 bn of Russian fossil fuels of which 33% (EUR 4.5 bn) has been Russian crude. Ships insured by NorthStandard transported EUR 1.2 bn worth of Russian crude and oil products in November 2023, an estimated 41% of the total oil traded by ships insured in the UK in the same month.

CREA’s analysis of vessels’ P&I insurance in particular makes two important points. Russia’s reliance on UK insurance to transport their oil provides the UK with significant leverage which they can use to lower the price cap, and implement better monitoring and enforcement that would considerably lower Russia’s oil export revenues.

It also shows the somewhat posturing nature of the support and aid that the UK provides to Ukraine, while at the same time supporting Russia’s ability to fund the invasion by conducting its oil trade easily and globally.

How can the UK curb Russian oil revenues?

The most important way to cut Russia’s export revenues will be to drive down the oil price cap and use their reliance on G7/EU insurance to do so. Lowering the price cap would be deflationary, reducing Russia’s oil export prices and inducing more production from Russia to make up for the drop in revenue.

A price cap of USD 30 per barrel would have slashed Russia’s revenues by EUR 4.9 bn or 41% in November 2023 alone. If this price cap had been established in December 2022 and paired with full enforcement, when the sanctions were originally implemented, Russia’s oil export earnings would have been reduced by 40% (EUR 56 bn). Russia has consistently traded oil using Western owned or insured tankers above the price cap, and as Russia has found new and consistent buyers, prices have risen. Higher export prices for Russian oil paired with evidence that trades have taken place above the cap with limited enforcement of sanctions significantly negates the impact of the price cap.

The movement towards the implementation of tighter shipping measures are encouraging, but more needs to be done to tackle violations and disincentivize those doing so. The UK and Price Cap Coalition should require maritime insurers to verify via bank statement that the oil price was paid below the cap to avoid fraudulent attestation documents being used to attain Western insurance; this could significantly improve compliance with the policy.

Vessels owned or insured by G7 countries have persisted in loading Russian oil at all ports within Russia during periods when prices remain above the price cap. These occurrences serve as compelling evidence of violations against the price cap policy. Yet there is very little information on enforcement agencies implementing penalties against shippers, insurers or vessel owners in the public domain. The UK Office of Financial Sanctions Implementation (OFSI), must investigate UK entities and insurance firms that have provided services to facilitate the maritime transportation of Russian oil above the oil price cap. Penalties must be implemented on firms that violate sanctions and facilitate Russia to increase their oil export earnings, above the price cap, which are then used to fuel the war on Ukraine.

Penalties for entities caught violating the oil price cap are inadequate. The UK and sanctioning countries should ban maritime services in perpetuity for vessels used to transport Russian crude without complying with the price cap. The current ban of 90 days prohibiting vessels from attaining EU maritime services following a violation of sanctions is far too weak. The UK’s monitoring and enforcement agency can impose fines of around GBP 1 million for breaches of the oil price cap or 50% of the value of the breach. These are weak punishments for tankers carrying crude oil that are often valued at more than GBP 100 million.

The UK and Oil Price Cap Coalition should introduce a spill insurance verification programme for vessels that travel through their waters. Sanctioning countries could mandate that tankers travelling through their waters must provide compliant spill liability insurance under international maritime law. This could exclude ‘shadow’ tankers without spill insurance from travelling through their most travelled route from Baltic ports whilst reducing the risk of environmental catastrophe. If this policy excluded many ‘shadow’ tankers from transporting oil from the Baltic ports it could increase Russia’s reliance on legally insured vessels and enhance the leverage of the oil price cap policy.

| Methodology: CREA’s analysis uses Kpler to estimate seaborne exports from Russia and other countries. We receive protection and indemnity (P&I) insurance information about ships from known P&I providers directly as well as from Equasis. More information about our datasets and methodology can be seen here. |

- Russia’s invasion began with dozens of missile strikes on cities all over Ukraine before dawn on 24 February 2022. ↩︎