Current account crisis and stagflation de-fuels energy demands in the country, with annual air pollution levels expected to be lower this year than past years

By Dawar Butt, Energy and Air Quality Researcher; and Sunil Dahiya, South Asia Analyst, CREA

Pakistan’s economy has remained in turbulent waters for most of the past two years, starting in early 2022 when the current account deficit started to rise while tranches from the International Monetary Fund (IMF) assistance programme were delayed. The country depends heavily on imported crude oil and petroleum products, along with other imported fossil fuels (LNG, LPG, and coal). This dependency has also been previously pointed out in a CREA analysis of emissions during the COVID-19 linked national lockdown. Russia’s decision to limit gas sales to the EU in 2021 and the invasion of Ukraine in February 2022 resulted in serious price shocks around the world, also felt in Pakistan. Unlike retail sales of other items, Petroleum products do not have a Sales Tax or Value-added Tax in Pakistan. But beyond this, the unfolding political turmoil in Pakistan further exacerbated the crisis as the outgoing and incoming governments both refused to pass on costs to consumers and did not charge applicable Petroleum Development Levy. While prices continued increasing internationally for Petroleum products and Crude oil, local prices in the country did not follow the same increase which enhanced the subsidy burden. Until as late as June 2022, the then Pakistani government maintained explicit fuel subsidies, and only removed them as part of the IMF’s demands for resumption of financial assistance. These measures created a market distortion and tilted market demand to overconsumption, nearly bankrupting the country.

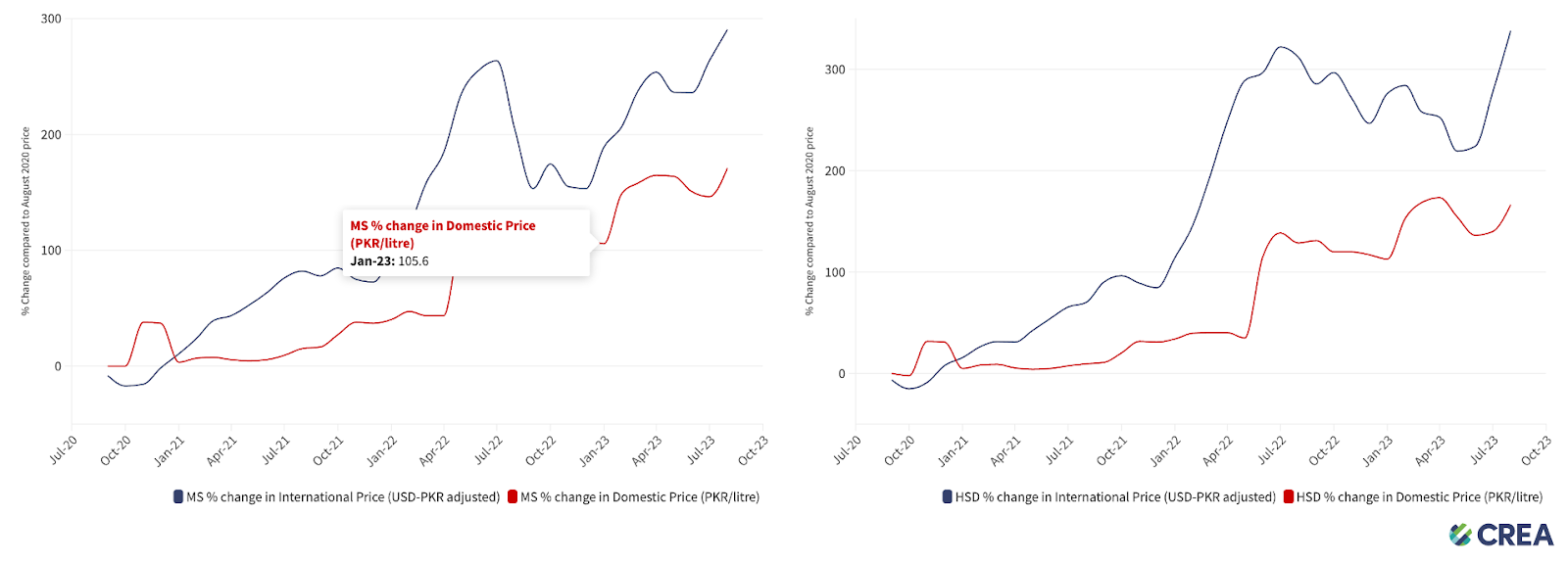

Figure 1: % Change in domestic and international price of Motor spirit (MS) & high-speed diesel (HSD): Prices artificially kept low through implicit & explicit subsidies in the highlighted period

By artificially stabilising local prices, while international prices increased and the Pakistani Rupee (PKR) depreciated, the government incentivized the consumption trend, which would have fallen as later trends now show. When this subsidy ended in late June 2022, it was estimated that it cost PKR 248 billion, or USD 1.4 billion. The emissions trend in large cities closely followed the consumption trend, as transport and energy sectors are heavily reliant on fossil fuels. Nitrogen dioxide (NO2) data obtained through CREA’s tool based on Sentinel 5-P Tropomi shows reduced emissions levels in major cities in Pakistan, such as Karachi.

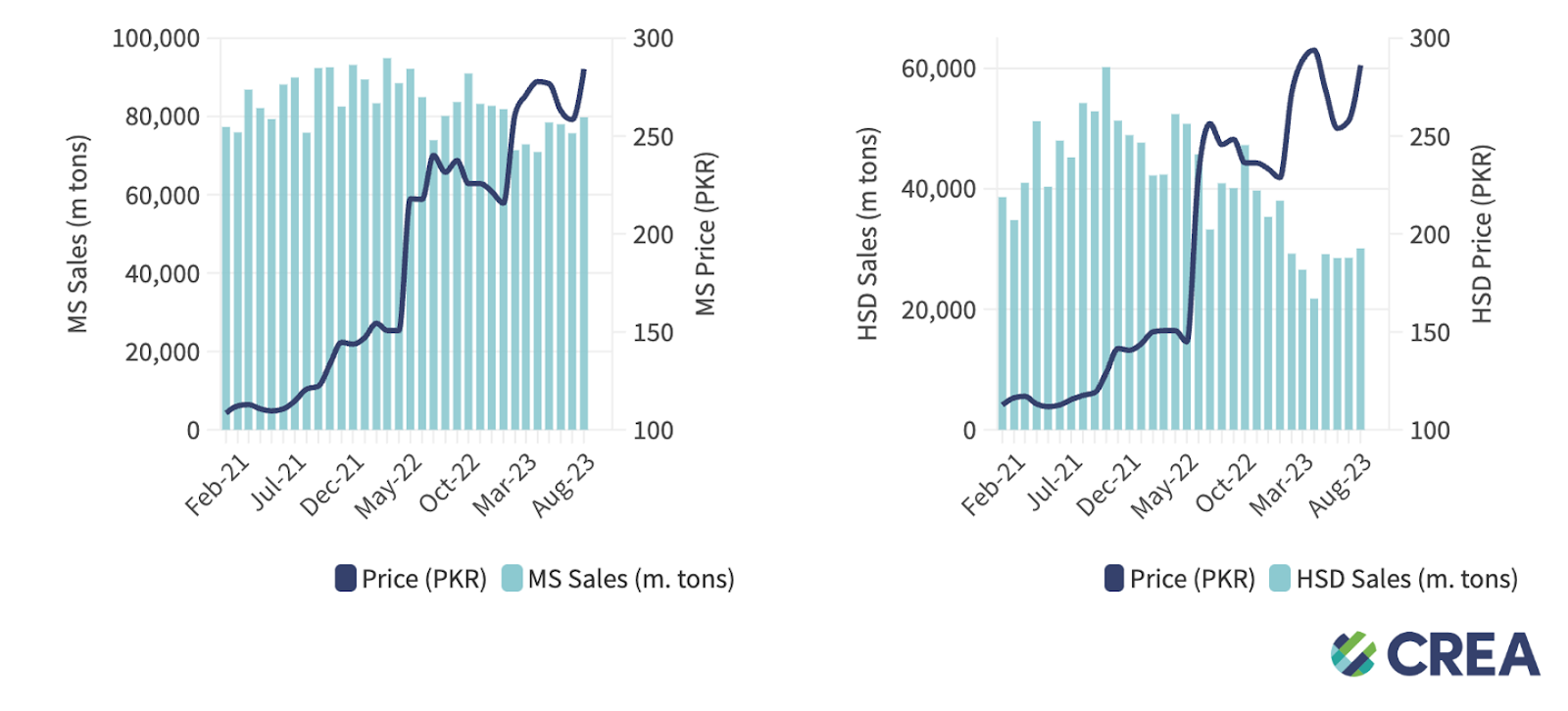

During the period of January 2021 until August 2023, motor-spirit (MS) sales in Karachi peaked in March 2022, while high-speed diesel (HSD) sales peaked in October 2021. Year-on-year (YoY) combined sales volumes during January to August periods for both 2021 and 2022 varied only slightly, at 1,009,285 tons vs 1,042,970 tons, respectively, but for the same period in 2023, the sales are down to 841,221 tons – a decline of 24% YoY.

Figure 2: Fuel sales in Karachi against local fuel prices

Motor spirit (MS) volumes are believed to have been relatively more stable . Inflation also appears to have driven users towards cheaper two-wheelers. Based on estimates from Google Environmental Insights Explorer, 57.7% of journeys in Karachi in 2022 were on two-wheelers, up from 47.7% in 2018. Since the start of 2023, price hikes have substantially dented fuel sales, down by nearly a quarter from previous year. It should be noted that due to Karachi’s proximity to Iran, cheaper smuggled diesel is available for purchase in the outskirts of the city, which is likely one of the reasons for a sharper decline in ‘formal’ HSD sales data. Some analysts have claimed that Iranian HSD took 25-35% of the total demand in the market.

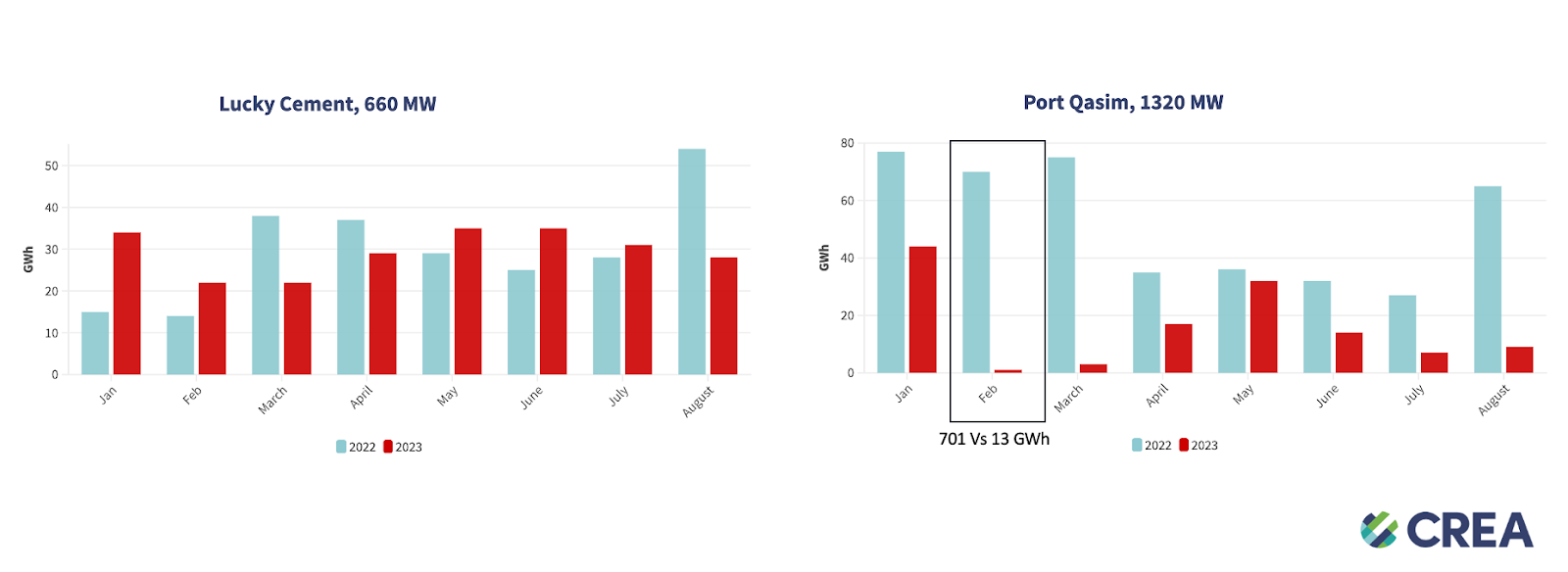

Other than fuel consumption for transportation, energy production from a major Karachi-based coal power station also collapsed as falling forex reserves forced the government to restrict payments to the Chinese-sponsored 1320 MW Port Qasim Coal power plant in February 2023. The decrease likely also contributed to reductions in emissions. Another station, the 660 MW Lucky Electric Coal power plant, continued generation, with only a marginal decline. Between the two years, cumulative production for the two plants fell from 6,652 GWh to 3,715 GWh over the same period (January to August).

Figure 3: Power generation at two Karachi-based coal power stations

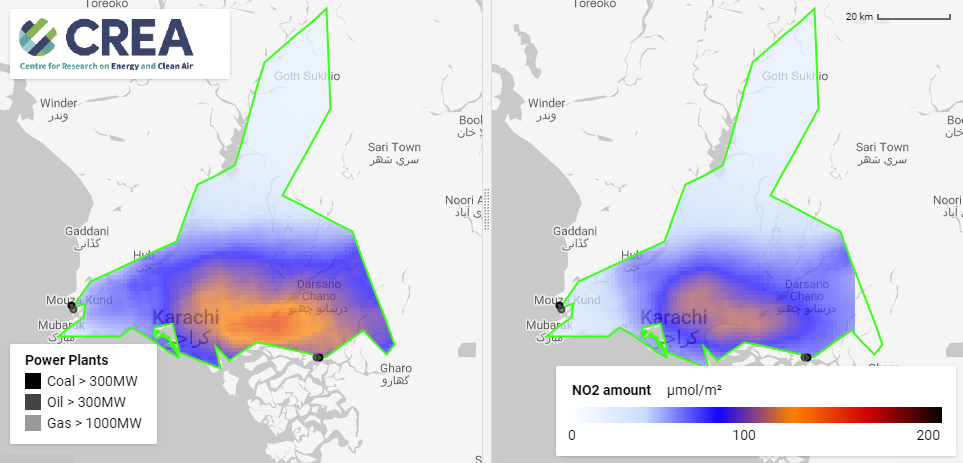

The impact of these changes has led to observable reductions in nitrogen dioxide (NO2) levels this year (January to August), by 20.14% within the bounds of Karachi division. The use of smuggled diesel inside the city, which is unaccounted for in official sales data, likely resulted in a somewhat lower emissions decrease vis-a-vis expectations based on reduced fuel sales. However, the claims of 25-35% cannot be accurately confirmed without monitoring of retail outlet sales, plus informal sales, compared to figures released by oil marketing companies (OMCs). Beyond lower power generation and road transport levels, industrial activity has also slowed down contributing to reductions, which have not been accounted for in this analysis.

Figure 4: NO2 levels in Karachi during January to August 2022 (left) vs 2023 (right)

Latest NO2 trends across major cities

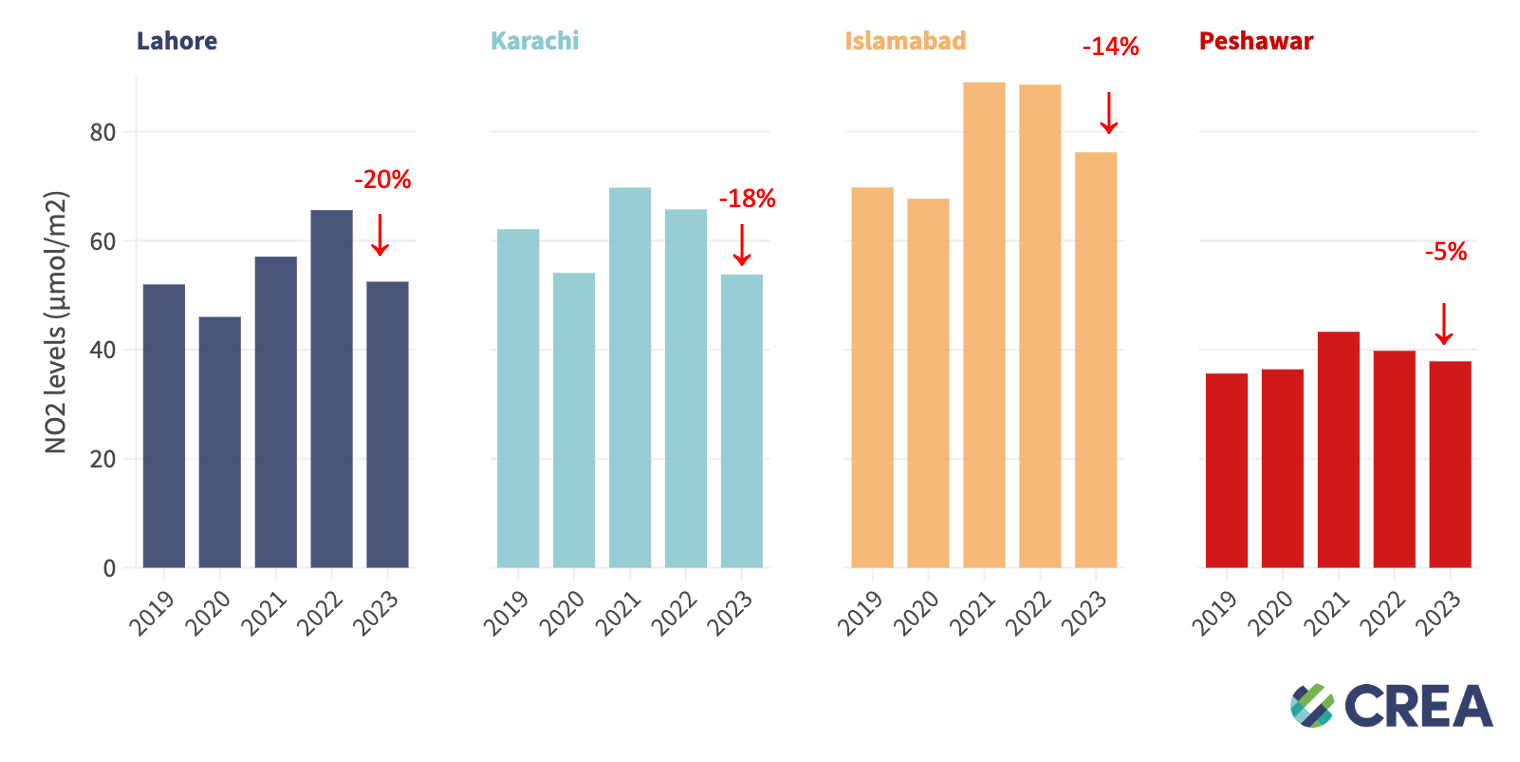

Similar to Karachi, economic activity levels have fallen across major cities. Reduced transport use, combined with industry shutdowns and lower thermal power generation around cities are resulting in reduced emission levels. Previously, comparable levels of emissions were observed during 2019 (attributed to economic slowdown) and 2020 (attributed to Covid-19 lockdowns). NO2 data for Lahore, Karachi, Islamabad, and Peshawar is compared for January to September periods over the last 5 years, which shows emissions falling down for these large cities.

Figure 5: Observed reduction in percentage in NO2 levels during January to September 2023 vs previous year(s)

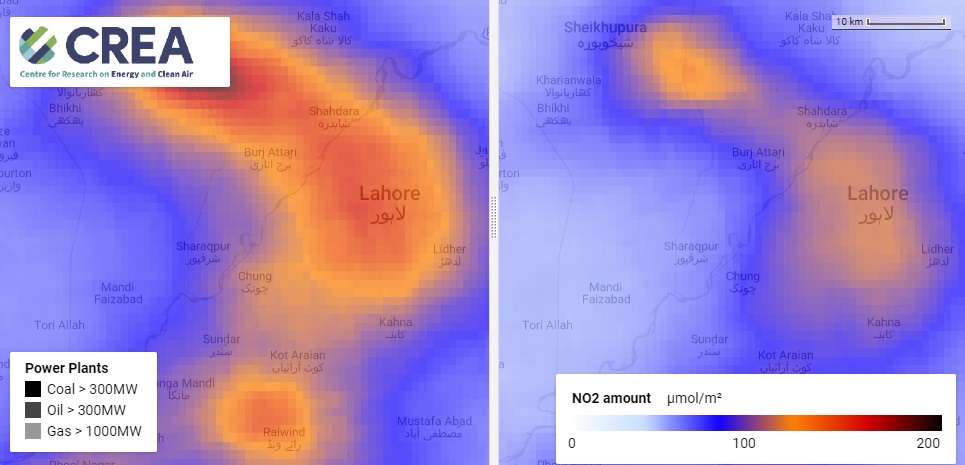

Figure 6: NO2 levels in Lahore during January to September 2022 (left) vs 2023 (right)

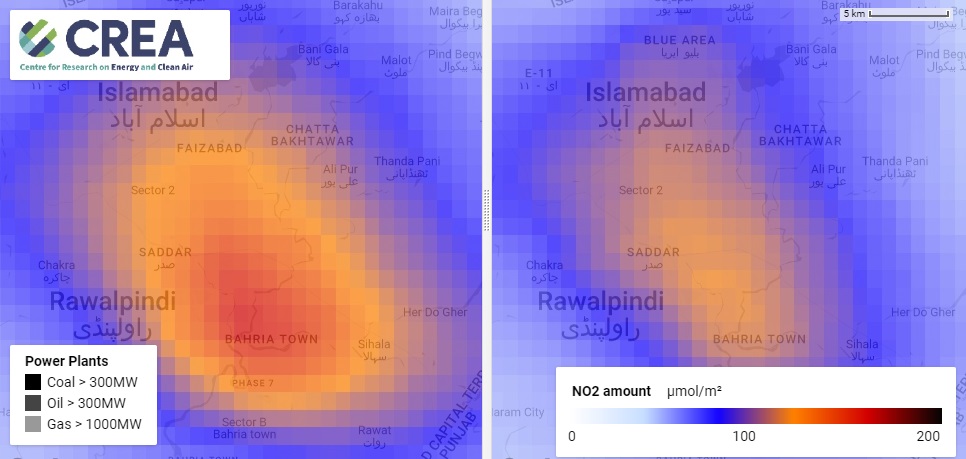

Figure 7: NO2 levels in Islamabad & Rawalpindi during January to September 2022 (left) vs 2023 (right)

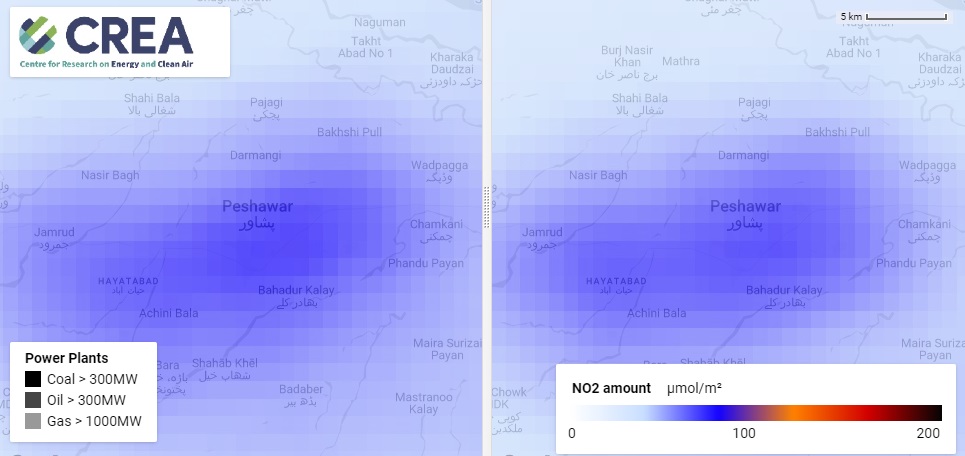

Figure 8: NO2 levels in Peshawar during January to September 2021 (left) vs 2023 (right)

Conclusion

As the above discussed data and short-term economic expectations indicate, energy consumption across major Pakistani cities will likely remain muted for the remainder of the year. It can further be expected that emissions will remain subdued and lower during the upcoming ‘winter smog’ months, when air quality turns ‘very poor’ in cities like Lahore and Peshawar – both ranked among the top ten polluted cities by IQAir. Alongside NO2 levels, monthly particulate (PM2.5) averages may also be comparatively lower, because sources of emissions greatly overlap, with the exception of some activities such as construction and biomass burning. Notwithstanding effects of meteorological variations, the annual average levels are expected to be similar to 2019 and 2020. While it may appear that citizens would get some respite, it is also possible that people and businesses may be forced to use poorer quality, highly polluting fuels, leading to localised anomalies, in the absence of affordable sources of heating.

The findings also, yet again, show that many sectors, particularly transport and power, are highly dependent on imported fuels, which are a burden on the national economy as well as high-emissions in the absence of better technology. Improving fuel-quality standards, vehicle engine technology, incentivising electric vehicles (cars, rickshaws, and bikes, as well as buses and other vehicle fleets), and expanding renewable energy are some of the ways Pakistan’s economy can be de-linked from the reliance on imported fuel and at the same time reduce air pollution in major cities.

Data Sources

Fuel Sales volumes – OCAC (https://www.ocac.org.pk/oil-industry-statistics/)

Fuel Prices – PBS (https://www.pbs.gov.pk/cpi)

International Fuel Prices – MarketWatch (Gasoil/Diesel: https://www.marketwatch.com/investing/future/gas00?countryCode=UK, MS: https://www.marketwatch.com/investing/future/rb.1)

Power Generation – NEPRA (https://nepra.org.pk/publications/State%20of%20Industry%20Reports/Detail%20of%20Generation/SIR%20Data%202022.htm) USDPKR Exchange Rate – MarketWatch (https://www.marketwatch.com/investing/currency/usdpkr)