Fossil power generation rebounded in May as exceptionally weak wind conditions limited clean power growth. Industrial activity remained subdued, while energy imports and refining weakened, and batteries and NEVs stayed strong.

By Qi Qin, China Analyst; Elizabeth Frost, China Analyst; Miao Chien, Data Scientist; with contributions from Lauri Myllyvirta, Lead Analyst

A group of wind turbines in Nagqu, southwest China’s Xizang Autonomous Region, May 2026. Photo: Xinhua/ Alamy.

Key findings

- Fossil power generation rose 2% year-on-year in May, mainly because of exceptionally weak wind conditions. Wind speeds in March, April, and May were all lower than in any of the previous 10 years; without this drop, rising clean power supply would likely have reduced coal- and gas-fired generation. Curtailment may also have played a role, but weak wind was the key driver and is likely to reverse quickly.

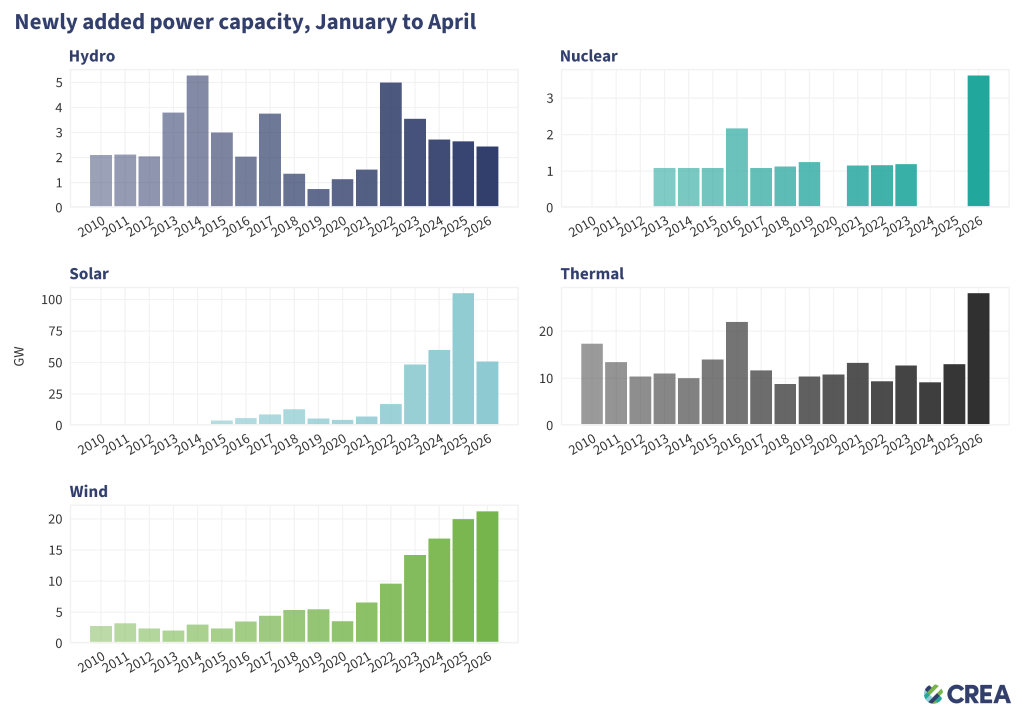

- Thermal power commissioning in the first four months surged by 116% year-on-year, reaching a record high. Solar power capacity additions fell by 52% year-on-year due to the high base in the same period last year, but remained above the level seen in the first four months of 2023. Wind power additions rose by 6.5%.

- In May, shipping disruptions through the Strait of Hormuz continued to weigh heavily on China’s energy imports, with crude oil imports falling by 29% year-on-year. Coal imports also declined by 7.7%, mainly due to relatively high import prices. The pressure on energy supply also fed through to the refining sector: average daily throughput fell to its lowest level since 2023. Refiners are increasingly drawing on their own inventories to keep operations running.

- Domestic natural gas output fell 2.2% year-on-year in May, marking its first monthly year-on-year decline since 2017, partly due to a high base in the same period last year and weaker seasonal demand. Cumulative output in the first five months still rose 1.7%. Gas imports stayed at the same level as the same period last year.

- Industrial value-added growth rebounded modestly in May but remained weak, with steel and cement output continuing to fall year-on-year. Cement output remained at its lowest level for the same period since 2020, while chemical fibre output extended a decline that began in April, when output fell for the first time in 22 months. Non-ferrous metal output remained elevated, up 2.2%.

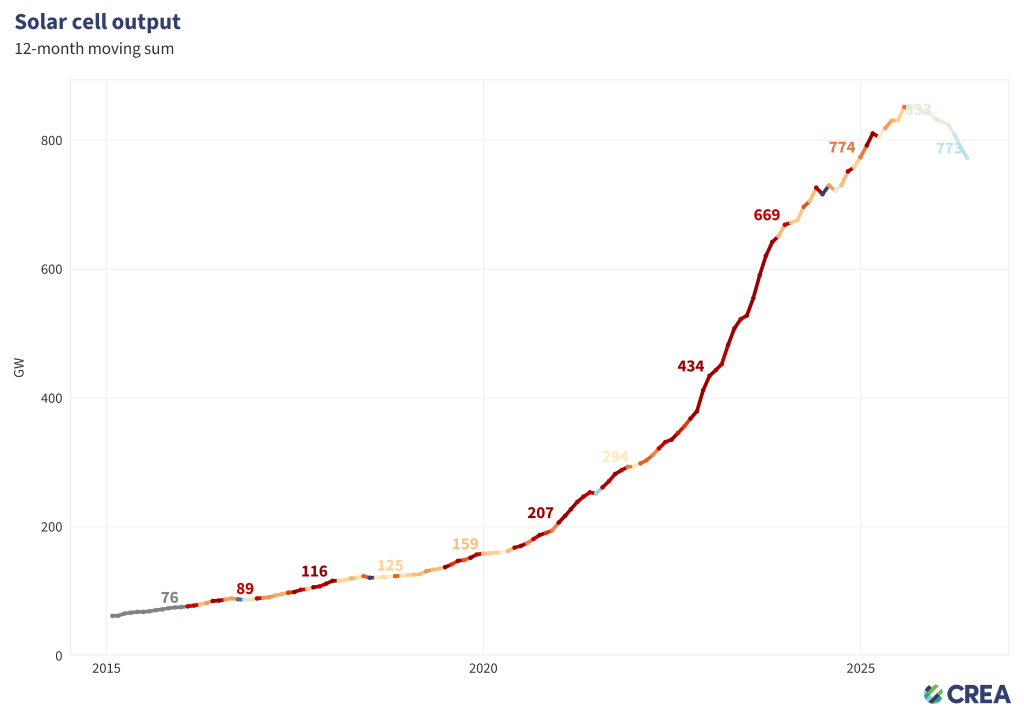

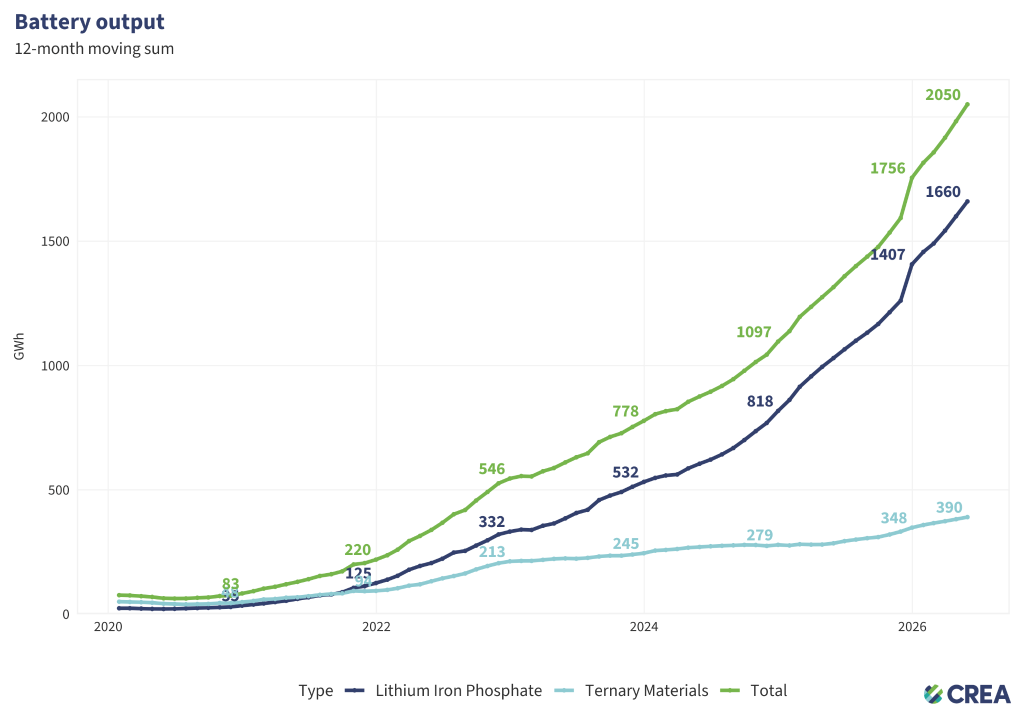

- Solar cell production fell by 20.4% year-on-year, reflecting weaker domestic installations. The decline suggests that China’s solar manufacturing sector is adjusting after last year’s exceptionally rapid deployment boom. Battery output remained strong in May, rising 55.2% year-on-year, supported by energy storage demand and exports.

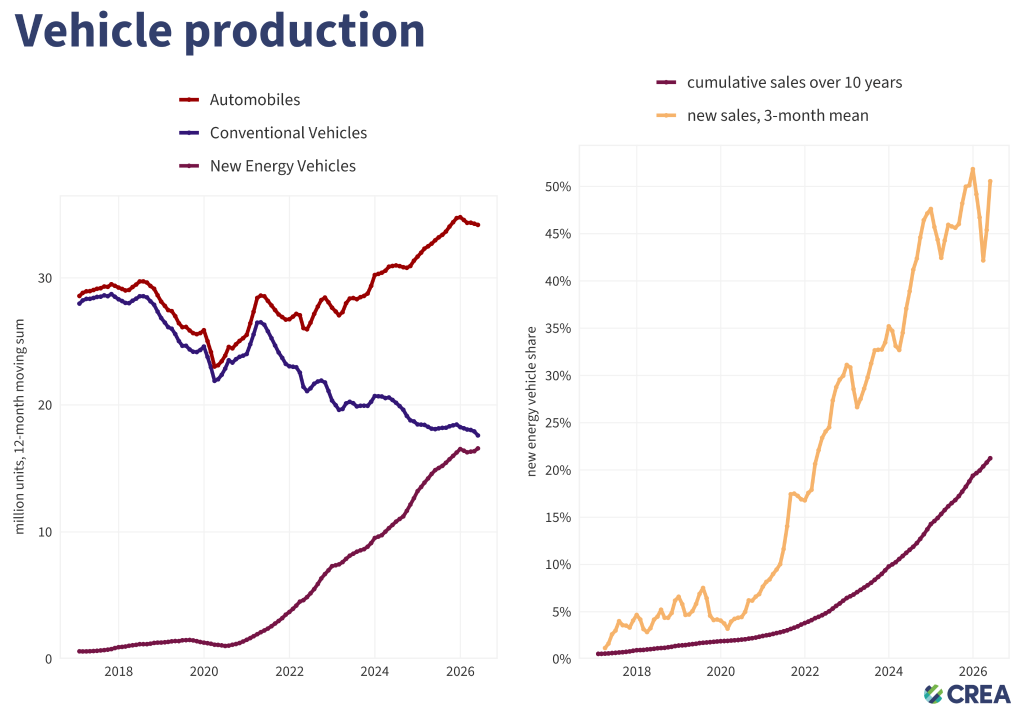

- New energy vehicles (NEVs) continued to outperform the broader auto sector in May, with their share of total vehicle production rising to 57% and exports more than doubling to a record high for the month. Production of fuel-burning vehicles fell sharply, by 22%.

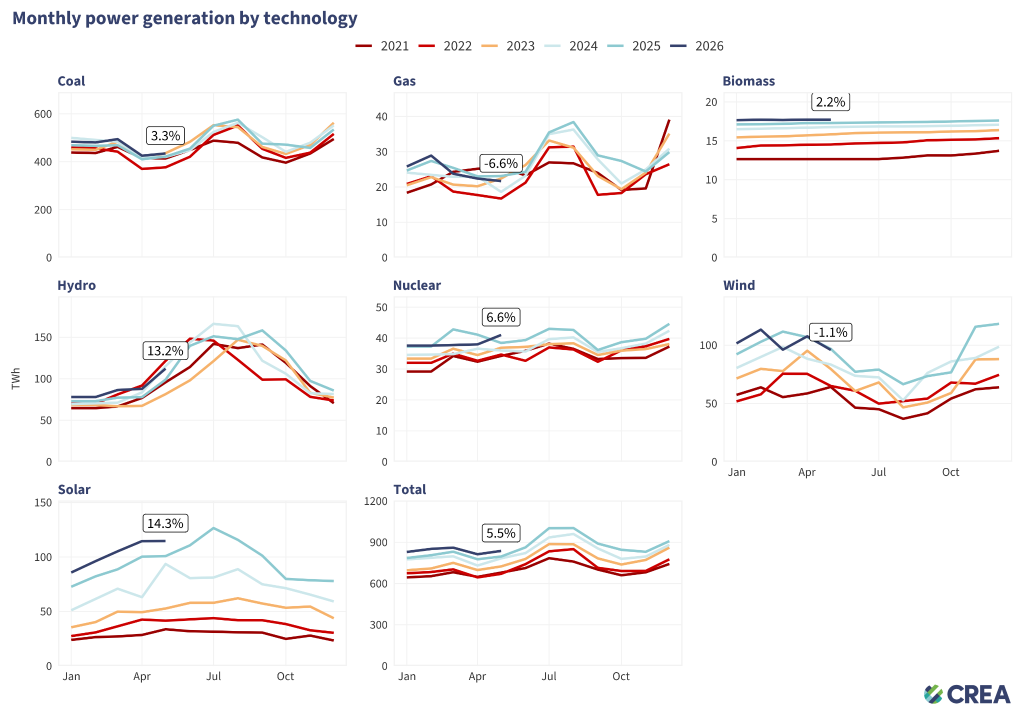

Coal power rose again as wind underperformed

- In May, power generation by large-scale power producers rose 4.2% year-on-year, while total power generation is estimated to have increased by 5.5%.

- Coal power generation rose 3.3% year-on-year, marking the fifth consecutive month of increase, as wind underperformed. This came after China’s coal power generation fell in 2025 for the first time in a decade.

- Gas power generation dropped by about 6.6% year-on-year, reflecting the impact of Strait of Hormuz shipping disruptions on natural gas supplies.

- Solar generation rose by 14.3% year-on-year.

- Wind generation dropped by 1.1% year-on-year, as wind speeds in May were unusually low.

- Hydropower and nuclear power generation grew 13.2% and 6.6%, respectively.

*Thermal, nuclear, and hydropower generation are based on National Bureau of Statistics (NBS) data. Wind and solar generation are estimated from installed capacity and projected utilisation rates, adjusted for weather and average curtailment over the preceding three months. Coal and gas generation are estimated by splitting total thermal generation using last year’s same-month fuel mix, adjusted by the year-on-year change in the fuel mix over the preceding three months.

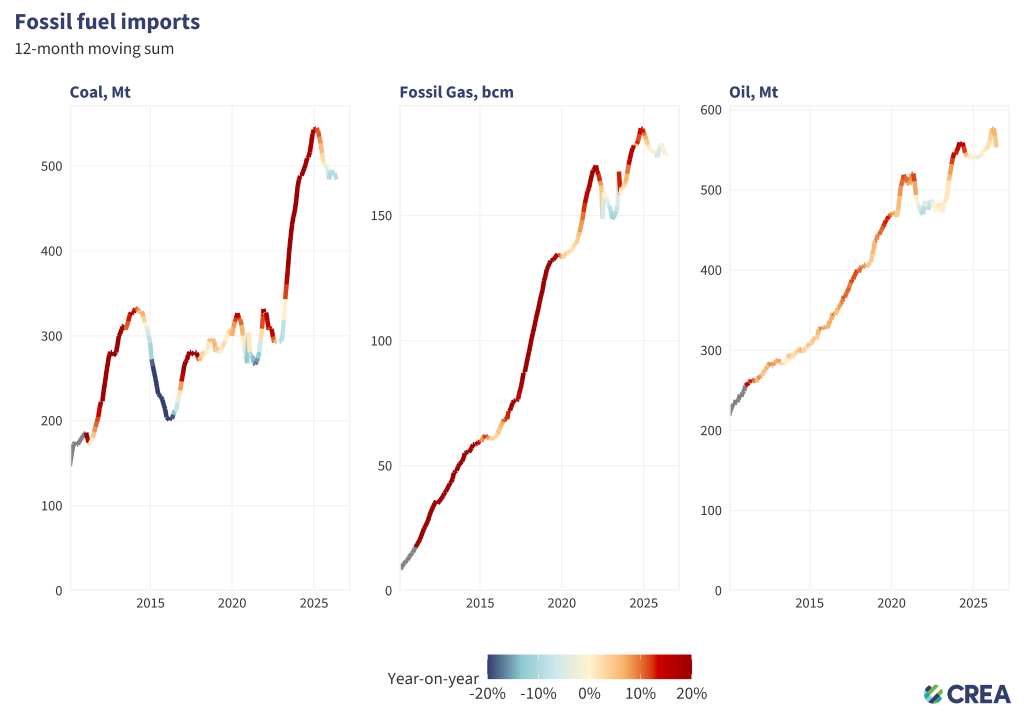

Fossil fuel imports remained in decline amid shipment disruptions and price hikes

- China’s coal imports fell by more than 7.7% year-on-year in May 2026. For the first five months as a whole, import volumes were down 3.2% year-on-year.

- China’s crude oil imports fell by 29% year-on-year in May, to the lowest level in a decade, still showing a clear impact from shipment disruptions through the Strait of Hormuz. For the first five months as a whole, oil import volumes declined 4.8% year-on-year.

- Natural gas imports stayed at the same level as the same period last year, amid the same Gulf shipment disruptions. This brought cumulative imports so far this year to about 4.9% below the same period in 2025.

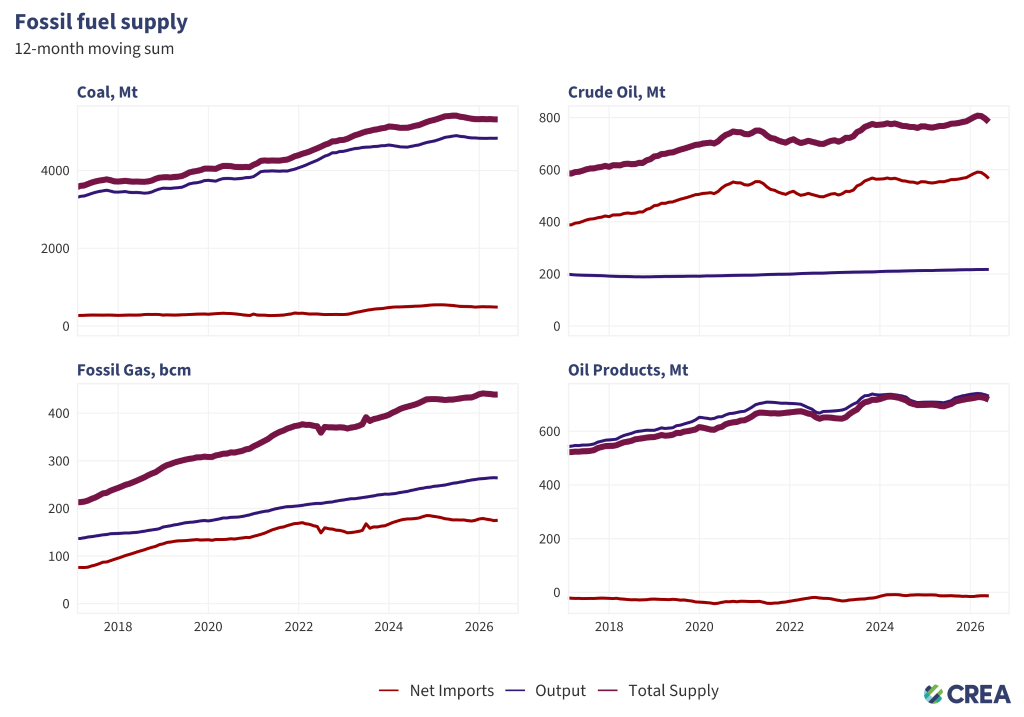

Coal and gas output declined as oil production inched up

- Coal output fell 1.7% year-on-year in May 2026, bringing production in the first five months down 0.3% from a year earlier. Coal output has now gone ten consecutive months without year-on-year growth.

- Domestic natural gas output fell 2.2% year-on-year in May, the first monthly decline since 2017, partly due to a high base last year, while output in the first five months was still up 1.7%.

- Crude oil production increased by 0.5%. Output in the first five months increased by 1.1%.

- The fall in crude oil imports continued to feed through to refinery activity in May. Crude throughput dropped 9.1% year-on-year, a decline 3.3 percentage points steeper than in April, while average daily throughput fell to its lowest level since 2023. Refiners are increasingly drawing on their own inventories to keep operations running.

Industrial output growth remained weak despite a modest rebound

- The steel sector continued to weaken in May, with output of pig iron, crude steel, and steel products falling by 2.6%, 2.7%, and 2.8% year-on-year, respectively.

- Cement output continued to fall 8.1% year-on-year in May, staying at its lowest level for the same period since 2020. First five months output was down 8.6% year-on-year, extending the decline in one of China’s most emissions-intensive industrial sectors.

- Chemical fibre output dropped 3.3% year-on-year, extending a decline that began in April, when output fell for the first time in 22 months. Non-ferrous metal output remained elevated, up 2.2%.

- Sulfuric acid production, an important input for phosphate fertiliser production, dropped by 2.6%.

The steel and cement industries are the largest CO2 emitters in China, when emissions from their electricity use are included. They are also bellwethers of real estate, infrastructure, and other fixed-asset investments that play an outsized role in China’s emissions and economy.

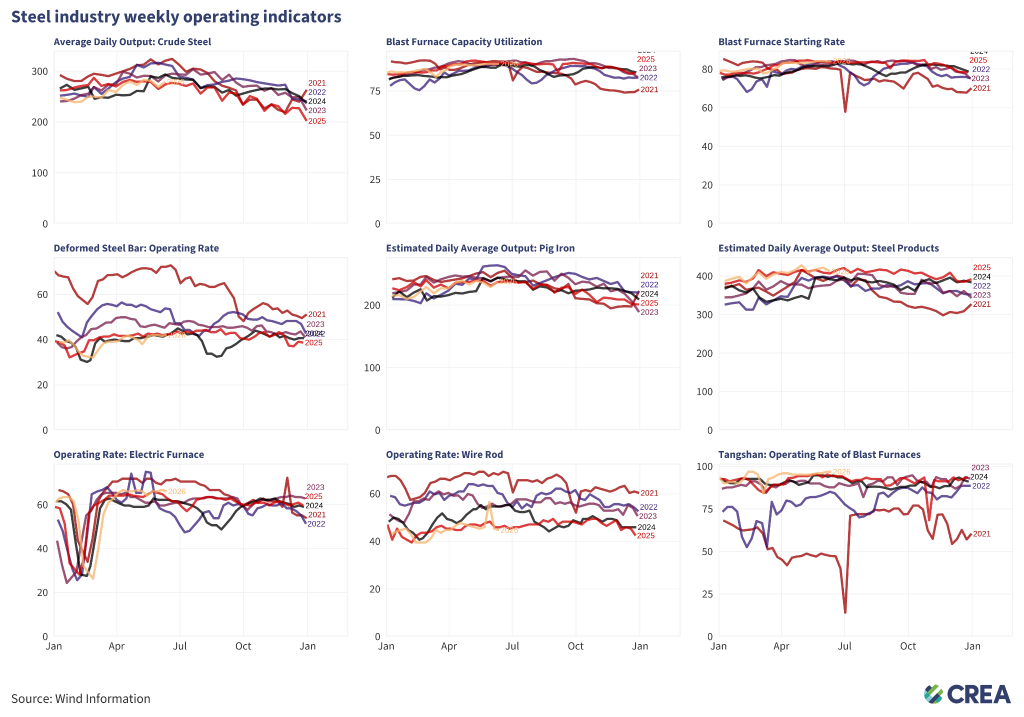

Tangshan blast furnace activity reached multi-year high

- In the second week of June, blast furnaces for steel production remained active, with a starting rate of 84.3% and utilisation reaching 90.3% — both among the highest levels seen so far this year. Electric furnace operating rates also rose to 66.7%, slightly above the same period last year.

- In early June 2026, daily crude steel and pig iron output were slightly above the level of the same period last year.

- The operating rate of blast furnaces in Tangshan, China’s ‘steel capital’ and a significant source of air pollution in Beijing, reached 96.8% in early June, close to the highest level in history.

Hebei Province industrial output is a bellwether of national priorities: when air quality and emissions are the priority, it is the most tightly regulated area due to its impact on Beijing’s pollution levels.

Thermal power addition more than doubled year-on-year

In the first four months of 2026, China added:

- 50.9 gigawatts (GW) of solar power capacity, down 52% from last year;

- 21.3 GW of wind power capacity, up 6.5% from last year;

- 28 GW of thermal power capacity, up 116% from last year;

- 2.45 GW of hydro power capacity, down 7.5% from last year;

- 3.6 GW of nuclear power capacity.

In April 2026 alone, China added:

- 9.5 GW of solar power capacity, down 79% from last year;

- 5.5 GW of wind power capacity, up 2% from last year;

- 4 GW of thermal power capacity, up 8% from last year;

- 1.25 GW of hydro power capacity, up 140% from last year;

- 2.4 GW of nuclear power capacity.

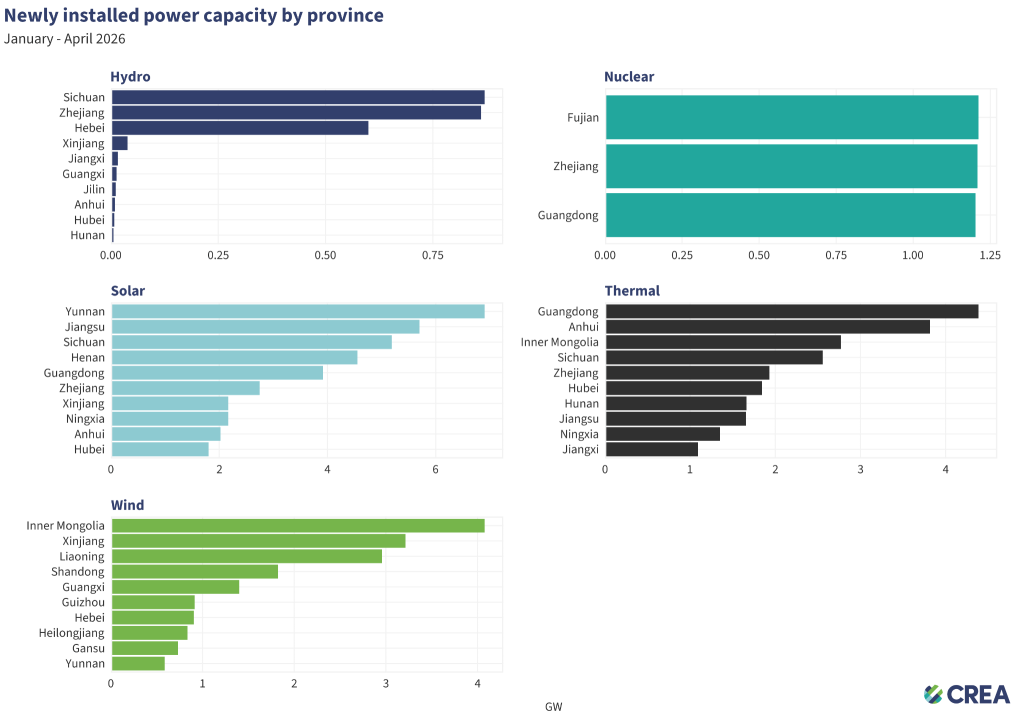

Large-scale clean energy bases took the lead in wind and solar installations

- Solar power installations are led by Yunnan, Jiangsu, and Sichuan. The strong showing of Yunnan and Sichuan is notable, as both are already major hydropower provinces and are set to host new hydro-wind-solar bases under the 15th Five-Year Plan (FYP).

- Inner Mongolia, Xinjiang, and Liaoning lead in wind development. These provinces are also part of the large-scale clean energy bases initiative under the 15th FYP.

- Thermal (coal) power additions accelerated in Guangdong, Anhui, and Inner Mongolia. Guangdong has led the country in new thermal power capacity additions in recent years, and its coal-fired generation continued to rise in 2025. By contrast, coal generation declined in both Anhui and Inner Mongolia despite the increase in new capacity.

Solar cells weakened further, while batteries continued to boom

Solar cell production fell by 20.4% year-on-year, reflecting weaker domestic installations. The decline suggests that China’s solar manufacturing sector is adjusting after last year’s exceptionally rapid deployment boom.

Battery production remained on a strong growth trajectory in May, reaching 191.7 GWh, a 55.2% increase from a year earlier, driven by robust demand from energy storage and export markets.

NEV production share rose as exports hit May record

- NEV production continued to grow in May, rising 17.8% year-on-year, bringing the first five months’ output up 0.9%. Overall vehicle production declined 3.2% in May, bringing the share of NEVs rising to 58% of all vehicles produced, up from 47% in May last year.

- China’s new energy vehicle exports surged by more than 110% year-on-year in May 2026, setting a new record for the month.

Relevant analysis by CREA:

China’s CO2 climbs 2% in early 2026 due to ‘wasted’ wind and solar

What drove China’s historic drop in power-sector emissions?

China’s new carbon metric leaves Germany-sized gap in its emissions

Reclaiming credibility in China’s steel industry: Climate ambition, financial resilience, and market trust

China’s 15th Five-Year Plan — Implications for climate and energy transition

Analysis: Clean energy drove more than a third of China’s GDP growth in 2025

Analysis: China’s CO2 emissions have now been ‘flat or falling’ for 21 months

Analysis: Coal power drops in China and India for first time in 52 years after clean-energy records

Built to peak: Coal power expansion runs out of room in China

China’s Climate Transition: Outlook 2025