China’s steel industry stands at a critical juncture. As the world’s largest producer and exporter of steel, the sector plays a central role in both China’s domestic decarbonisation pathway and the evolution of global steel markets.

In September 2020, China announced its commitment to peak carbon dioxide emissions before 2030, marking a major shift in the country’s climate strategy. More recently, the country’s updated Nationally Determined Contribution (NDC), released in September 2025, pledged that economy-wide net greenhouse gas emissions will fall 7–10% below the peak level by 2035. Accounting for roughly 16% of China’s annual total carbon dioxide emissions, the steel sector is widely seen as one of the most important industries for delivering progress toward these climate commitments.

At the same time, the sector is also facing mounting financial pressures and increasing scrutiny from global markets. Persistent overcapacity, volatile profitability and rising leverage are heightening credit risks within parts of the industry, while a recent rebound in exports is reshaping global steel trade and contributing to renewed trade frictions with major importing regions.

Against this backdrop, the industry now faces a growing credibility challenge on multiple fronts. Progress toward the green steel transition has fallen short of policy expectations, financial resilience is under strain, and expanding exports are intensifying trade tensions with key partners.

Together, these trends raise a broader question: whether China’s steel sector can simultaneously deliver on its climate ambitions, maintain financial stability, and sustain constructive engagement with global markets. Restoring credibility will require structural adjustments that align climate commitments with financial discipline and evolving global trade dynamics.

Key findings

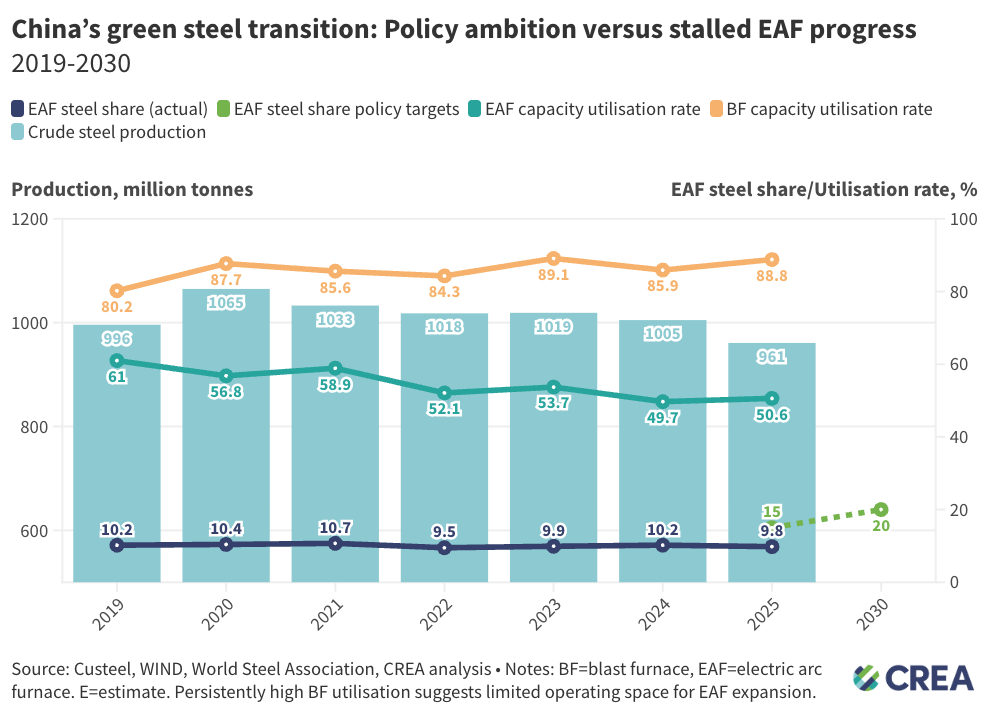

- Declining demand, rather than a structural shift to green steelmaking, drove emissions reductions in China’s steel industry in 2025. Crude steel production fell below 1 billion tonnes (-4.4% YoY) for the first time since 2020, substantially larger than the reductions expected from the policy target.

- Reviving green steel ambitions demands a structural shift away from carbon-intensive blast furnace-basic oxygen furnace (BF-BOF). Raising the electric arc furnace (EAF) share to 15–20% by 2030 could reduce BF-BOF steel production by around 80–120 Mt, equivalent to Japan’s annual steel output and approaching that of India.

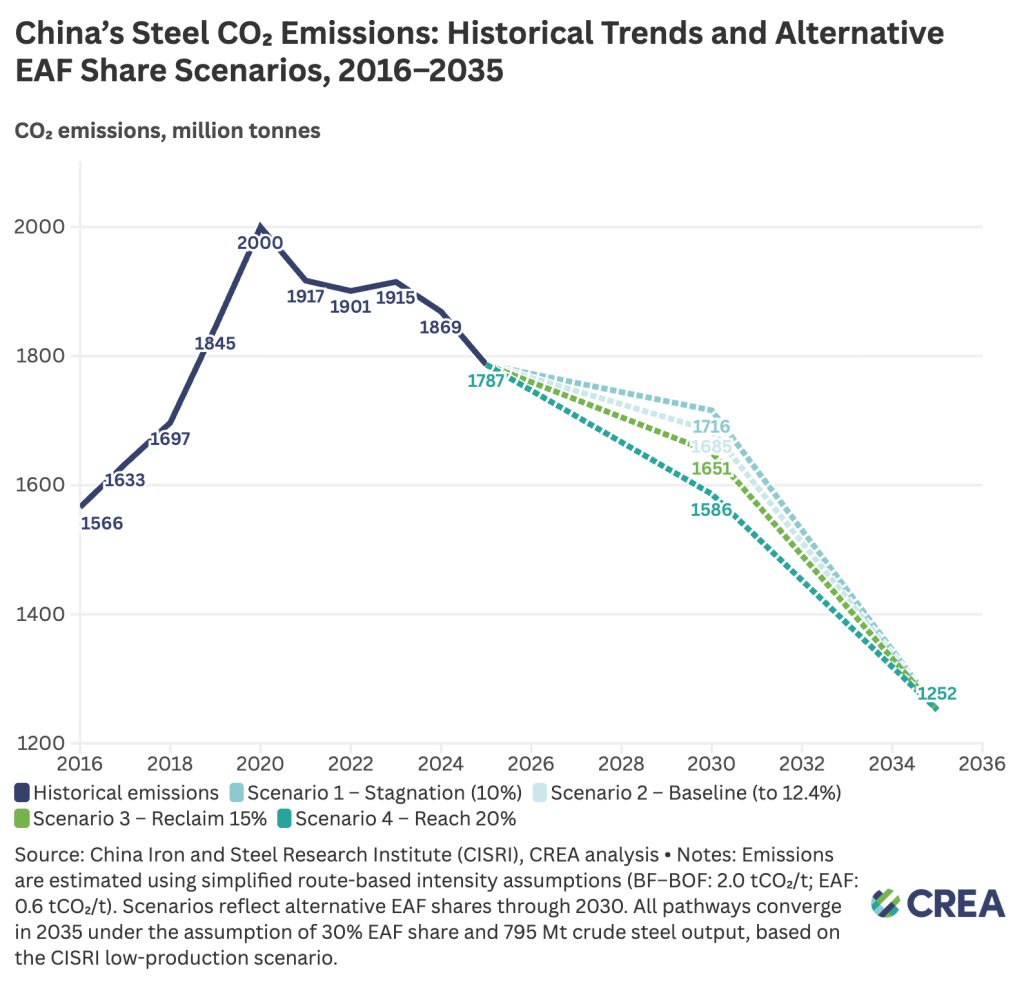

- Steel sector decarbonisation could significantly outperform national benchmarks. Under a prioritised EAF transition, steel sector emissions, which peaked in 2020, could go on to fall to nearly 37% below peak levels by 2035, greatly outpacing China’s updated Nationally Determined Contribution (NDC) target of a 7–10% drop for economy-wide net emissions.

- Persistent overcapacity and weak domestic demand have sharply eroded profitability in China’s steel sector, while industry liabilities rose by over 1 trillion CNY (+20%) between 2020 and 2025. A prioritised EAF pathway of at least 20% by 2030 could support recovered profits of up to CNY 220 billion and reduce the asset-liability ratio to roughly 60–62%, shifting the sector to a more stable footing.

- China’s share in the global steel trade surged from 13.3% to 29.2% between 2020 and 2025, intensifying its exposure to trade frictions. Enhancing the share of green steel will be crucial to strengthening the sector’s global competitiveness, especially amid tightening carbon-related trade measures, such as the EU’s Carbon Border Adjustment Mechanism (CBAM).

Figure — China’s green steel transition: Policy ambition versus stalled EAF progress, 2019–2030

Figure — China’s steel CO₂ emissions: Historical trends and alternative EAF share scenarios, 2016-2035

China’s steel sector can strengthen its credibility in climate commitments, financial liability, and global trade in the following ways:

- Align climate, industrial, and trade policies to strengthen green competitiveness.

- Accelerate blast furnace phase-down to ease supply pressures, improve market conditions, and directly reduce the sector’s total emissions.

- Raise the EAF share to 20% by 2030, alongside stronger economic incentives to accelerate structural adjustment in the sector.

- Tighten financial support for inefficient steelmakers and operationalise exit mechanisms.