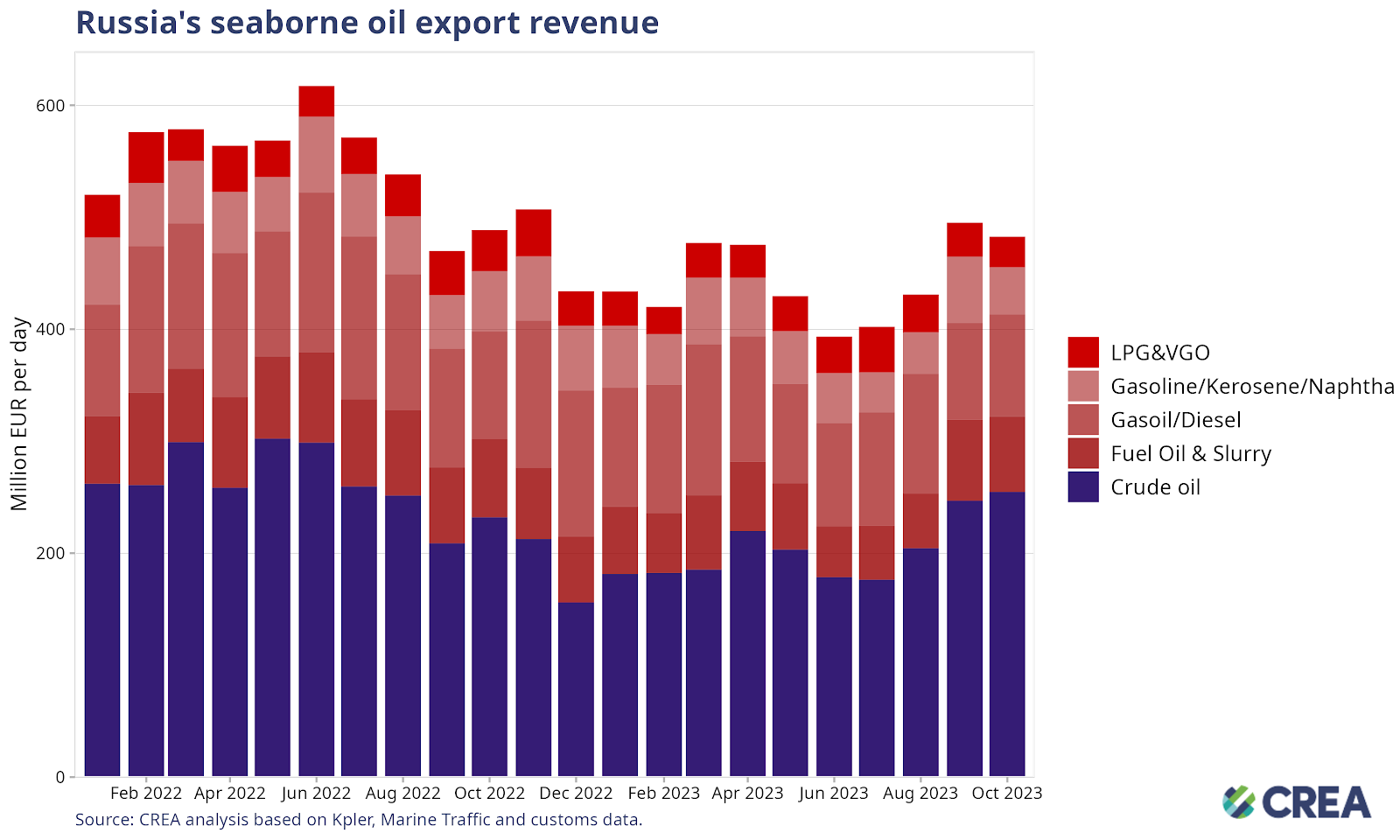

Despite a 2% month-on-month decline, Russia’s export revenues for October were the second-highest for 2023, with a notable rise in seaborne and pipeline crude.

By Isaac Levi, Europe-Russia Policy & Energy Analysis Team Lead; Vaibhav Raghunandan, Europe-Russia Analyst and Research Writer; Petras Katinas, Energy Analyst; and Panda Rushwood, Data Scientist

Key findings

- Compared to September, Russia’s monthly export revenue from fossil fuels marginally declined in October by EUR 16 mn per day (-2%).

- Seaborne oil products saw the most significant decline — amounting to EUR 19 mn per day (-7%) — primarily due to restrictions on the export of these products.

- Seaborne and pipeline crude oil, on the other hand, rose by EUR 7 mn per day (+3%) and by EUR 5 mn per day (+4%), respectively.

- The 10% (4mn per day) increase in monthly revenues of LNG can be attributed to a growth in exports to Asia (8%) and Europe (27%).

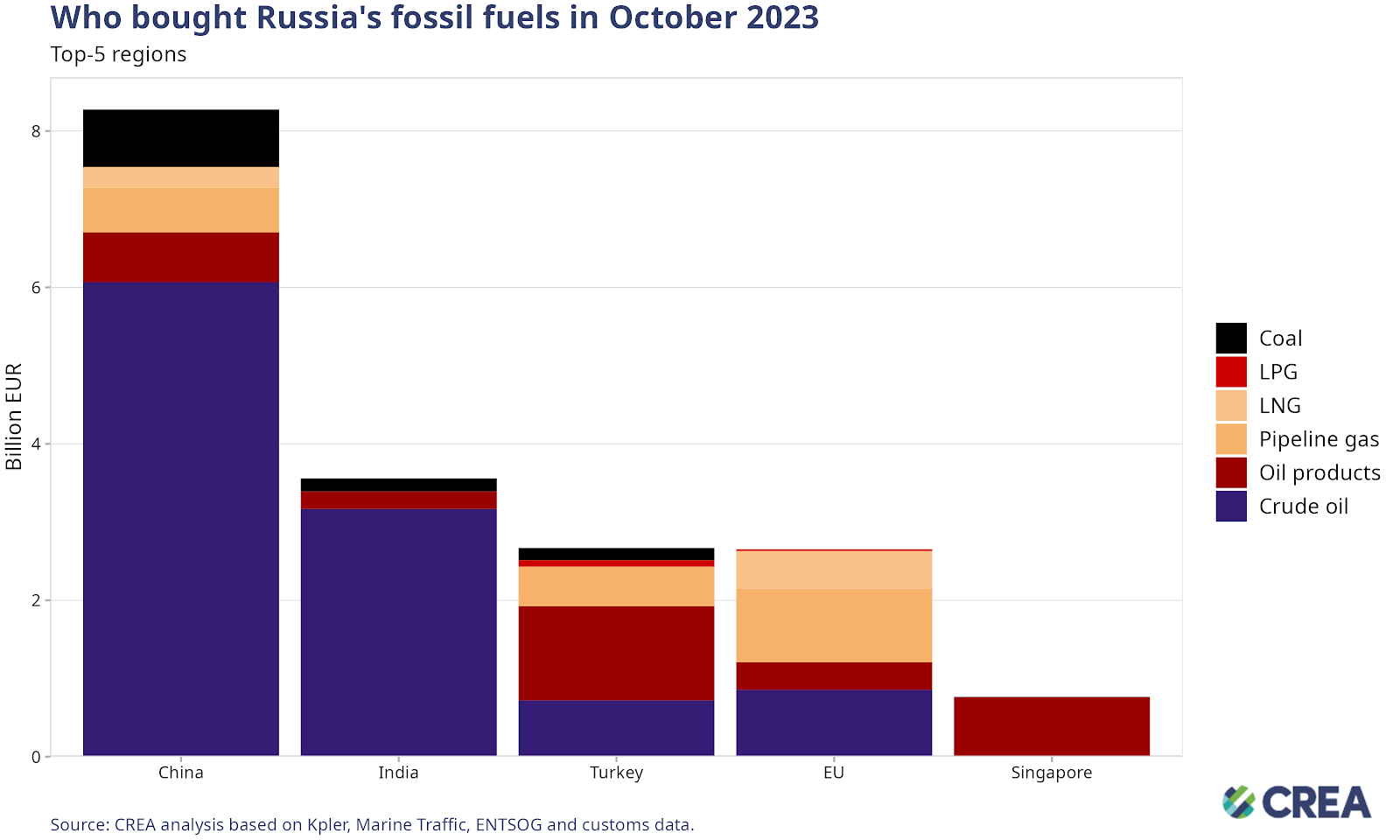

- China was the largest importer of Russian fossil fuels, followed by India, Turkey, the EU, and Singapore.

- Month-on-month revenue from Russian crude oil exports to China saw a marginal 4% increase, with a notable portion of the imports from the Eastern Siberia–Pacific Ocean (ESPO) oil blend.

- Russian monthly revenues from seaborne crude oil to India increased by 17% — around EUR 500 mn.

- In October, 48% of Russian crude oil and oil products were transported by tankers subject to the oil price cap policy. The rest (52%) were shipped by “shadow” tankers, which are not subject to the price cap policy.

- Setting the cap for crude oil at USD 30 per barrel could have slashed Russian revenues by 52% (EUR 7.82 bn) in October alone. If this cap had been set since the sanctions against Russian oil were imposed in December 2022, Russia’s oil export revenues could have been slashed by nearly half — EUR 59 bn (-49%). Reducing the price cap would be deflationary and force Russia to produce more oil to compensate for the drop in price.

Trends in total revenue

- Compared to September, Russia’s October export revenues fell marginally by 2% (EUR 16 mn per day).

- While month-on-month revenues from seaborne oil products decreased by EUR 19 mn per day (-7%), Russia’s monthly revenues from seaborne crude oil exports saw an increase of EUR 7 mn per day (+3%). Revenues from pipeline oil rose by EUR 5 mn per day (+4%). This was a third consecutive month of growth in revenue from both pipeline and seaborne crude oil. .

- Monthly revenue from LPG (Liquified Petroleum Gas) and VGO (Vacuum Gas Oil) increased by EUR 0.8 mn per day (+41%) compared to September.

- Month-on-month revenues from fossil gas exports via pipeline increased by 8 mn per day (+13%).

- Russia’s monthly revenue from LNG rose by EUR 4 mn per day (+10%), a shift that can be attributed to a 9% increase in export volume in October. Russia’s monthly exports to Asia increased by 8%, and there was a notable 27% surge in exports to Europe.

- Month-on-month coal exports fell by EUR 22 mn per day (32%) in October, the sixth consecutive month of declining revenues.

- In October, Russia’s oil export revenues declined by EUR 12 mn per day (-3%). The decrease can be attributed to Russia’s decision to curtail exports of its oil products.

- In comparison to September, monthly seaborne crude oil export earnings rose by EUR 7 mn per day (+3%). In October, export revenue from gasoil and diesel rose by EUR 5 mn per day (+5%). However, export volumes of gasoil and diesel moved in opposite directions. Diesel exports remained at the same level as September — the lowest exported over the last three years, mainly due to Russia’s partial ban on Russian oil products. Conversely, monthly gasoil exports witnessed a 17% increase and marked the third-highest export volume in the past three years.

- Russia’s export value of gasoline, kerosene and naphtha decreased by EUR 17 mn per day (-29%) compared to September. This can be attributed to Russian refineries reducing crude oil processing volumes in October.

- Month-on-month earnings from fuel oil and slurry decreased by 5 mn per day (-7%).

- Russia’s month-on-month seaborne export earnings from LPG and VGO fell by 10% (EUR 3 mn per day).

Who is buying Russia’s fossil fuels?

- Monthly revenue from crude oil exports to China increased by 4%, amounting to EUR 190 mn per day. This rise was evident in volume, with a notable portion of the imports comprising the ESPO blend. China’s import of seaborne Russian crude oil was second only to that from Saudi Arabia.

- Russia’s month-on-month revenues from seaborne crude oil to India increased by 17% (EUR 500 mn). In October, Russian seaborne crude oil exports to India remained broadly consistent, witnessing a decrease of less than one percent compared to September. Russia was the largest exporter to India, and Russian seaborne crude oil made up roughly 34% of their overall crude imports. Notably, Russian exports to India primarily included the Urals blend.

- Despite Turkey being the largest importer of Russian oil products, Russia’s monthly revenues from oil products decreased by EUR 270 mn (-19%) compared to September. In comparison, month-on-month revenues from crude oil increased by EUR 131 mn (+22%). Turkey imports mainly Urals blend, fuel oil, diesel, and gasoil from Russia

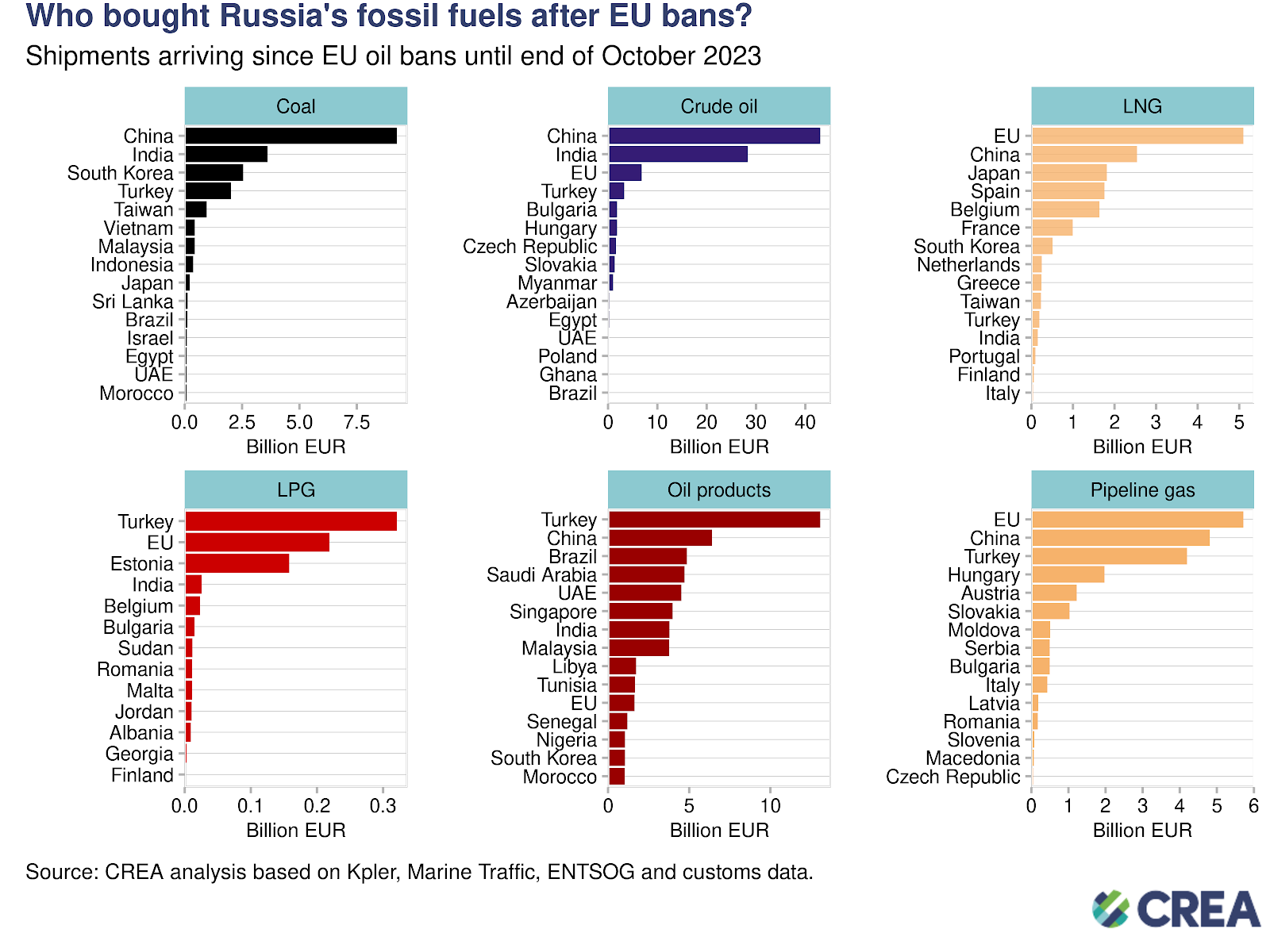

- Coal: Purchasing 45% of Russia’s coal exports, China became the largest buyer since the EU banned Russian imports on December 5, 2023. This is followed by India (18%) and South Korea (12%).

- Crude oil: China was the largest buyer (purchasing 52% of Russia’s crude oil exports, followed by India (34%), the EU (8%) and Turkey (4%). Since December 5, 2022, EU imports of crude oil have arrived via sea to Bulgaria and via pipeline for the Czech Republic, Slovakia and Hungary.

- LNG: The EU was the largest buyer (purchasing 48% of Russia’s LNG exports), followed by China (24%) and Japan (17%). No sanctions are imposed on Russian LNG shipments to the EU.

- LPG: Turkey was the largest buyer (purchasing 52% of Russia’s LPG exports), closely followed by the EU (36%). No sanctions are imposed by the EU on LPG imports from Russia.

- Oil products: Since the EU’s import ban on Russian crude oil, Turkey is the largest buyer (purchasing 24% of Russia’s oil products), followed by China (12%). While the EU’s sanctions on seaborne Russian oil products were implemented on 5 February 2023, oil via pipeline is only partially sanctioned.

- Pipeline gas: The EU was the largest buyer (purchasing 26% of Russia’s pipeline gas), followed by China (22%)). No sanctions are imposed on Russian gas via pipeline into the EU.

- Accounting for 46% of total imports, China was the biggest importer of Russian fossil fuels in October. India was second, importing 20% of Russia’s fossil fuels and Turkey (15%) was third. Meanwhile, the EU and Singapore contributed 15% and 4% to total Russian fossil fuel imports for the same period, respectively.

- Seventy-three percent of China’s total imports of Russian fossil fuels was crude oil. Coal (9%) was the second highest. A diverse range of oil products accounted for 7% of their imports. LNG and pipeline gas collectively accounted for the remaining 10% of China’s total Russian fossil fuel imports.

- India was the second-largest importer of fossil fuels from Russia in October. Crude oil accounted for 89% of India’s total fossil fuel imports from Russia. In October, oil products accounted for 6%, and coal accounted for 5% of their total imports.

- In October, 45% of Turkey’s imports from Russia were diverse oil products. Crude Oil contributed 27% of Turkey’s total imports, while pipeline gas and coal contributed 19% and 6%, respectively.

- In October, 35% of the EU’s purchases of Russian fossil fuels consisted of pipeline gas. Crude oil accounted for 32%, while LNG constituted 18%. In October, oil products and liquefied petroleum gas (LPG) made up 13% and 1% of the EU’s Russian fossil fuel imports, respectively.

- In October, Singapore was the fifth-largest importer of Russian fossil fuels globally, with 99% of their imports being oil products.

- Landlocked Central and Eastern European countries received Russian natural gas via pipeline through Ukraine and TurkStream. Crude oil was obtained via the Druzhba oil pipeline. The EU has not banned Russian natural gas and crude oil via the Druzhba South branch.

- In October, Hungary was the top importer of Russian fossil fuel within the EU. Its primary imports comprised crude oil and natural gas, delivered via pipelines valued at EUR 281 mn and EUR 257 mn, respectively. Analysis suggests that despite a rise in monthly gas consumption — which includes an increase in gas-fired power generation — gas imports have been declining. Hungary’s month-on-month fossil gas imports decreased by 11%. Total fossil fuel imports into Hungary from Russia also declined by 11% in the same period.

- Slovakia, like Hungary, imported EUR 200 mn worth of crude oil and 137 mn worth of fossil gas from Russia.

- Having been exempted from the ban on Russian imports, Bulgaria imported EUR 192 mn worth of crude oil, EUR 11 oil products and EUR 85 mn worth of gas via pipeline in October. All Russian oil transported to Bulgaria ultimately finds its way to the Neftochim Burgas refinery, the largest refinery in the Balkan peninsula, owned by the Russian company Lukoil. CREA’s investigation has found that Burgas is capitalising on the exemptions granted to Bulgaria by buying discounted Russian crude and selling refined products into the EU and the global market. Since the implementation of the EU’s import ban on Russian crude oil, Burgas imported Russian crude oil worth over EUR 1.1 bn in tax revenues to the Kremlin.

- In October, Austria imported fossil gas amounting to EUR 262 mn from Russia. Fossil gas imports showed a remarkable month-on-month increase of 142%, contributing to a 36% rise in total gas imports. CREA’s data based on ENTSOG (European Network of Transmission System Operators for Gas) indicates that the increase can be attributed to a 27% reduction in hydroelectric power generation. In comparison, gas-based power generation rose by 60%.

- The Czech Republic was the fifth largest importer of Russian fossil fuels within the EU. Their imports primarily comprised crude oil (EUR 192 mn) and pipeline gas (EUR 38 mn).

- The port of Sikka in India was the foremost destination for Russian fossil fuel imports in October, with monthly import volumes estimated at EUR 1 bn. These imports were predominantly composed of crude oil (EUR 0.84 bn) and oil products (EUR 0.15 bn).

- Vadinar in India was the second largest importer of Russian fossil fuels, particularly crude oil. Imports of crude oil exceeded a substantial monthly total of EUR 0.8 bn.

- Singapore (Singapore), Aliaga (Turkey), and Dongjiakou (China) rounded off the top ports importing Russian fossil fuels in October.

How are oil prices changing?

- Urals crude prices have stayed above the oil price cap (60 USD) since the middle of July. In October, the average price for the Russian Urals was USD 76.5 per barrel and decreased by 2% compared with September.

- The prices for the East Siberia–Pacific Ocean (ESPO) and Sokol blends, primarily associated with Asian markets, saw a 1.2% drop from September. These prices consistently remained above the specified price cap level for the entire month.

- Throughout this period, vessels owned or insured by G7 and European countries persisted in loading Russian oil at all ports within Russia. These occurrences serve as compelling evidence of violations against the price cap policy.

Russia remains highly reliant on European and G7 shipping industry

- In October, 48% of Russian oil and its products were transported by tankers subject to the oil price cap policy. The remainder was shipped by “shadow” tankers that are not subject to the price cap policy.

- Sixty-one percent of Russian crude oil was transported by “shadow” tankers, while ships owned or insured in countries implementing the price cap accounted for 38% of all crude oil exports. Tankers subject to the price cap policy transporting oil products, chemicals, and LPG handled 63% of the total volume of products. The remaining volume was transported via “shadow” tankers.

- This month, 59% of Russia’s total oil exports were shipped from Russian Baltic Sea ports. Additionally, 20% were exported through Black Sea ports, while 20% originated from Pacific ports. The remaining 1% came from ports in the Arctic.

- The proportion of tankers utilising vessels insured or owned by countries implementing price caps to transport fossil fuels from Russia’s Baltic (51%) and Black Sea ports (57%) is significantly higher than in the Pacific ports (23%). The remaining volume was transported by “shadow” tankers.

- Tankers in the Pacific region were loaded with Russian oil at ports like Kozmino, where the ESPO pipeline ends and is connected to the refinery. Here, the ESPO crude oil grade is exported at prices that exceed the cap, observed in customs data.

- Russia’s reliance on EU/G7 owned or insured vessels provides the coalition with adequate leverage to lower the price cap, implement better monitoring and enforcement, and considerably lower Russia’s oil export revenues.

How can Ukraine’s allies tighten the screws?

- Fossil fuel exports from Russia have fallen since sanctions were implemented, showing the impact they have had on lowering Putin’s ability to fund the war. However, much more should be done to limit Russia’s export earnings and constrict the Kremlin’s war chest. This includes measures like lowering the oil price cap, increased monitoring and enforcement of sanctions and banning unsanctioned fossil fuels such as LNG, LPG and pipeline fuels that are legally allowed into the EU.

- Additionally, measures must be taken to prevent Russia’s ability to ship its oil without relying on Western-owned or insured vessels and circumventing the price cap policy, including a ban on the sale of old tankers that are used to transport Russian oil.

- A price cap of USD 30 per barrel (still well above Russia’s production cost that averages USD 15 per barrel) would have slashed Russia’s revenue by EUR 59 bn (49%) since the sanctions were imposed until the end of October. This month alone would have seen a reduction of EUR 7.82 bn or 52% with a USD 30 price cap per barrel.

- Lowering the price cap would be deflationary, reducing Russia’s oil export prices and inducing more production from Russia to make up for the drop in revenue.

- A thorough enforcement of the price cap would have slashed Russia’s oil export revenue by 25% (approximately EUR 3.75 bn), even accounting for the rise in prices of Russian oil.

- Enforcement agencies overseeing the sanctions must take proactive measures against violating entities, including insurers registered in Price Cap Coalition countries, shippers and vessel owners.

- Despite clear evidence of violation, there is very little information on enforcement agencies implementing penalties against shippers, insurers or vessel owners in the public domain. Penalties against violating entities increase the perceived risk of being caught.

- Penalties for those found guilty of violating the price cap must be significantly harsher. Current penalties include a 90-day ban of vessels from securing maritime services after violating the price cap, a mere slap on the wrist. Vessels should be fined and banned in perpetuity if they are found guilty of violating sanctions.

- The lack of proper monitoring and enforcement and increasing oil prices have increased Russia’s export revenues to fund its war against Ukraine.

Relevant reports:

- Putin rakes in extra €1B for his war chest via Bulgaria sanctions loophole

- Shedding light on “shadow” tankers: Who transports Russia’s oil 18 months into the invasion?

- EU Targets ‘Shadow Fleet’ That Carries Russian Oil

- Belgium, France, Spain must halt their Kremlin gas deals

| The monthly update on Russian fossil fuel exports and sanctions was prepared by Isaac Levi, Europe-Russia Policy & Energy Analysis Team Lead, CREA; and Panda Rushwood, Data Scientist, CREA. |

| Note on methodology: From 2023‑04‑03, our monthly analysis values are no longer seasonally corrected, which may lead to some disparities between the preceding and following reports. We have also adjusted our time frame to show totals since the start of 2023 rather than the start of the invasion. Dates featured are the date the arrival of the shipment was captured by our algorithm. 80% of arrivals for shipments are found within 4 days of the arrival port call in the specific port. For our oil products and chemicals commodity group, please note this contains a wider range of items than just those specified in the current sanctions, as of 2023‑02‑05. More information at: https://energyandcleanair.org/ |