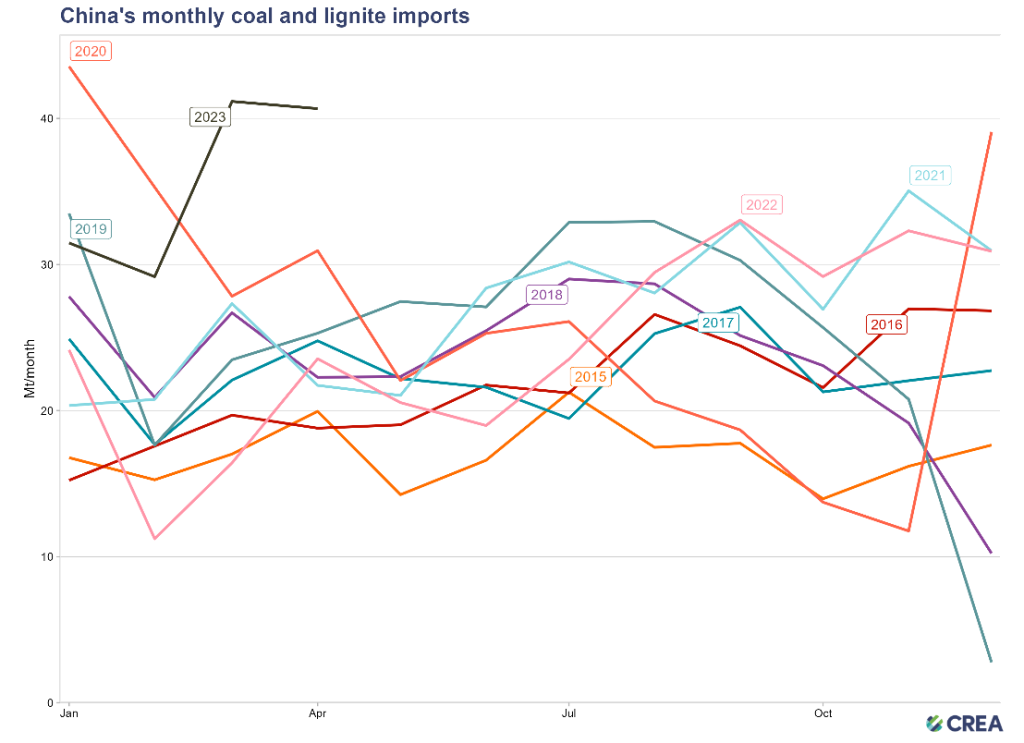

A new perplexing trend has emerged this year in China’s coal market. The country’s coal imports reached a new record for March and April this year. This seems paradoxical because domestic coal supply has increased sharply recently. This article uses data to identify the drivers of the increase in imports, and the implications for China’s energy security policies.

In the first four months of the year, China’s coal imports increased no less than 89% year-on-year. The increase continued in April with a 73% increase year-on-year. This seems paradoxical because domestic coal supply has increased sharply recently, growing 10.5% in 2022 and 5.5% in the first quarter of 2023. At the same time, total coal consumption increased by 4.3% in 2022 and 3.6% in the first quarter of 2023. Thermal power generation, the main user of imported coal, increased 1.4% year-on-year in 2022 and 1.7% in the first quarter of 2023.

Various explanations have been offered: increase in coal consumption, resumption of imports from Australia, resumption of exports from Indonesia and restocking demand. We will use data to examine each one of these factors.

As noted above, coal consumption and thermal power generation did increase in the first quarter of 2023. However, total seaborne coal deliveries, including deliveries of both domestic and imported coal, increased 7%, according to shipment tracking data from Kpler. This indicates increased demand, but cannot account for the brunt of the 89% increase in imports.

Imports from Australia did increase, but they only made up of 19% of total imports in the first four months of 2023, and cannot therefore explain much of the increase.

Most of the increase in imports came from Indonesia, along with Russia and Mongolia. Indonesia banned coal exports for the entire month of January 2022, affecting China’s imports both in January and February 2022, and therefore the year-on-year increases for the same months in 2023. The restrictions on exports from Indonesia only lasted until the end of January however so they cannot explain the year-on-year increase in March and April. Furthermore, China’s coal imports in March–April also increased in comparison to 2021 when there were no restrictions on Indonesia’s exports.

Can restocking demand account for the growth in imports? In 2022, total coal consumption was 3.03 billion tonnes standard coal, while production was 3.2 billion tonnes and imports approximately 200 million tonnes standard coal. This means that production and imports significantly exceeded consumption, which should have allowed stockpiles to be rebuilt to levels well exceeding 30 days of consumption. Stockpiles at surveyed power plants, at coal mines and at key Bohai ports did increase by 6%, 26.7% and 7.5%, respectively. This increase in supply should have quenched the restocking demand before the beginning of 2023.

All of the factors mentioned above undoubtedly contributed to the increase in imports, but something else was going on, too.

Seaborne coal deliveries of domestic coal from Chinese ports to coastal coal users fell by 21% year-on-year, based on Kpler data. Imports from Australia, Indonesia and Russia, the three main seaborne exporters to China, increased correspondingly. Therefore, there was a major shift from domestic to imported coal among coastal users.

Since the coal shortage of autumn 2021, expanding coal mining and increasing coal production has been a key energy policy priority, under the policy of ensuring coal supply. In late 2020 and early 2021, coal supply had fallen behind the rapid growth in coal consumption. In the first half of 2021, coal consumption increased 10.7% year-on-year while coal production only increased 6.4% and imports fell 19.7%. The sum of domestic production and imports increased 4.1%, far behind the growth in demand, which led to a shortfall in supply and depletion of inventories.

At the same time, global fossil fuel prices increased as Russia cut back gas supply to Europe and global demand started to rebound as pandemic controls were relaxed.

The increase in coal production was a necessary response to this situation, once it had emerged. The pressure to increase production rapidly led to new issues, however.

First, the expansion of domestic coal supply has increased costs. The producer price index (PPI) for coal mining and washing increased 45% in 2021 and 17% in 2022. This obviously put upward pressure on domestic prices.

Second, a mismatch has emerged in coal quality between what is produced and what users need. This is evidenced by the increase in price differential between 4500 kcal and 5500 kcal coal and tight supply of higher calorific value coal.

To fulfil the output targets and delivery contracts, miners have prioritised quantity over quality, exploiting lower quality coal reserves to hit the quota, or reducing the coal washing they usually carry out to increase the quality of their mined coal. This was seen for example in a coal market survey report by analysts at CITIC Futures, who in February visited eight coal mines in Inner Mongolia, Shaanxi and Shanxi. According to statistics from the Coal Industry Association, the raw coal washing rate in China has decreased from the peak of 74.1% in 2020 to 69.7% in 2022.

Last August, the state planning agency NDRC (National Development and Reform Commission) released a notice on ensuring the quality of coal under mid- and long-term contracts for coal used in power generation, in response to a recent “decline in the calorific value of coal purchased by power companies”.

In January 2023, a China Electricity Council official identified a “clear decline in coal quality” as a problem associated with long-term coal contracts, as well as deliveries of coal that don’t meet the quality specified in contracts.

Cinda Securities Research and Development Center also noted in a recent report that since the policy of ensuring coal supply was announced, the growth rate of physical coal consumption for electricity has been significantly faster than the growth rate of thermal power generation. The proportion of standard coal consumption in thermal power generation has continued to decrease, so the increase reflects a clear decline in the average calorific value of domestic coal. Cinda Securities points out that the main mining areas in northern Shanxi have depleted their reserves of high-quality thermal coal and have shifted entirely to mining lower-quality coal seams. The proportion of low calorific value coal in imported coal has also significantly increased, and the quality of imported coal has also declined noticeably.

The rapid expansion of coal production has changed the structure of China’s coal mining industry, as coal production growth has come mainly from smaller producers. In 2022, total coal output grew 10.5% according to the Statistical Communique while the output of the top 10 miners grew 6.5%, and in the first quarter of 2023, coal output by all medium and large-scale coal miners grew 5.5% while that of the top 10 miners grew 3.4%. During both periods, top 10 miners contributed one third of the growth in output while producing 51% of total output.

The increase in imports has therefore been caused by a combination of increased cost and declined quality of domestic coal, despite the expansion of supply, together with increased supply of imported coal.

The past two years have highlighted China’s exposure to the fluctuations in prices and supply in the seaborne coal market. This exposure will remain for the foreseeable future. In 2022, new coal power construction was accelerated significantly, and most of this new capacity is concentrated in coastal provinces. The relative competitiveness of imported and domestic coal in the seaborne market has major implications for import dependency and exposure to price volatility.

The quality and cost issues with domestic coal production don’t change the importance of energy security as a goal, but they can change the assessment of what’s the best way to pursue energy security. Further acceleration of solar, wind, nuclear and other domestic clean energy production can alleviate the pressure on the coal mining industry to increase output and maintain coal quality while reducing costs in order to compete with imported coal. Increasingly, the most economic way to pursue energy security is to rely on domestically produced clean energy.

| This article was originally published here on Energy New Media (能源新媒) with the title 煤炭产量和进口量为何双双破纪录增长?This is the English translation. |