Russia’s full-scale invasion of Ukraine and the ensuing energy crisis almost immediately underscored the European Union’s energy security vulnerabilities. The EU’s heavy reliance on fossil fuels, mainly those imported from a single supplier willing to exploit its position for political ends, revealed an urgent need for diversification in energy imports.

The invasion also became pivotal to the EU’s energy policy as Member States swiftly reduced their dependence on Russian coal, oil, and petroleum products. Despite these efforts, Russian liquefied natural gas (LNG) imports into the EU have surged significantly since the invasion. This influx not only grants Russia considerable political leverage over EU Member States but also funds their invasion of Ukraine.

In light of these developments, the EU, which previously committed to eliminating Russian fossil fuels, must uphold its pledge by reducing Russian fossil fuel imports and ultimately severing ties with Russia. This would halt the flow of funds fueling Russia’s war on Ukraine and diminish the country’s sway over the EU.

In 2021, 46% of the EU’s fossil gas imports came from Russia. However, since the full-scale invasion of Ukraine, this share has fallen significantly, to 24% in 2022 and 16% in 2023, partly due to supply disruptions and coercive tactics, which have also prompted the EU to find alternatives for fossil gas, a crucial step for diversifying supply but which led to a surge in extra LNG imports amidst the full-scale invasion.

In 2022, annual imports of liquefied natural gas (LNG) into the EU increased significantly by 63%, reaching 126 bcm. Imports from Russia, including transshipment, also saw a notable rise of 36% year-on-year, amounting to 20 bcm, which accounted for 15% of the EU’s total LNG imports.

For the past two years, there have been unsuccessful attempts to push politicians to ban Russian LNG imports. The situation has hit a stalemate, with importing Member States willing to reject Russian gas if EU-wide sanctions are applied, overruling concerns about potential gas shortages. A Russian LNG price cap policy could slash export earnings 60% on 2023 levels and leverages Russia’s huge reliance on Western owned or insured LNG tankers to force down the price of its gas exports.

Petras Katinas, Energy Analyst and author

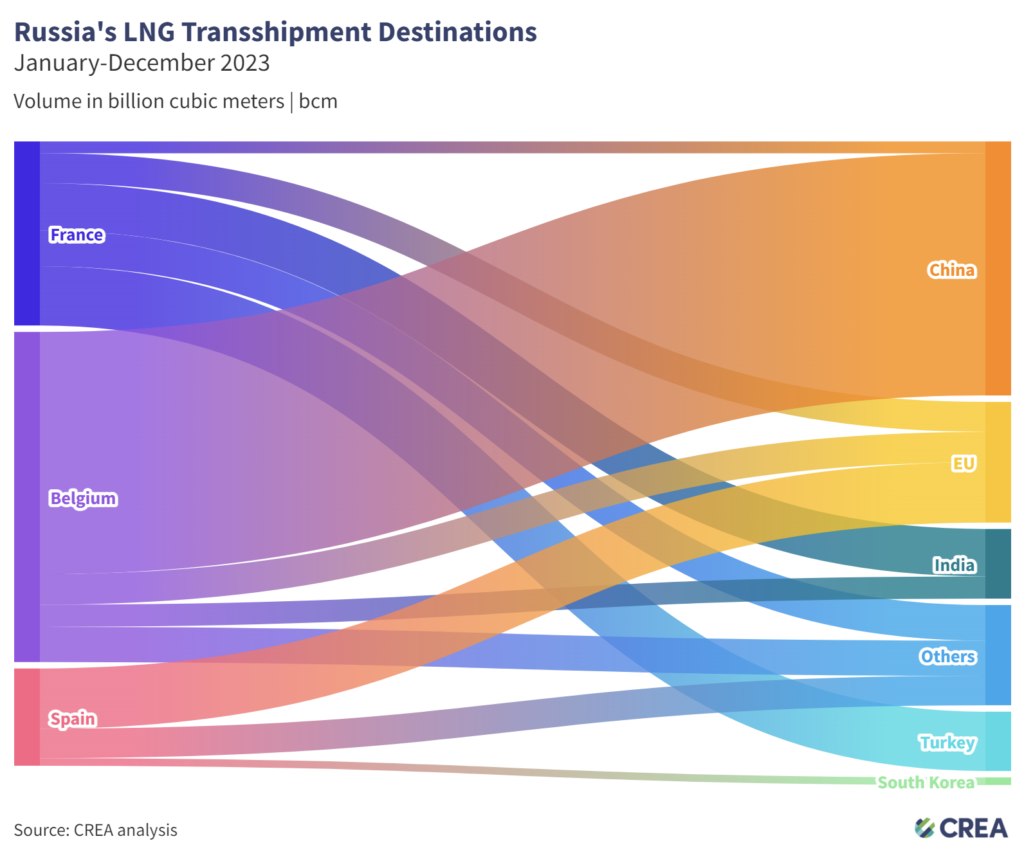

A portion of Russian LNG imported into the EU also bypassed its gas system and was transshipped to other global destinations. While most transshipped gas did not enter the EU gas system, it enabled Russia’s access to global markets, particularly in the Asia-Pacific region. CREA analysis found that 22% (4.4 bcm) of the EU’s Russian LNG imports were transshipped globally, with 8% (1.6 bcm) going to EU Member States in 2023.

Price cap

The continued reliance on G7+ services for LNG exports provides Ukraine’s allies significant leverage in regulating Russian LNG prices and introducing a price cap. Russian LNG exporters would be compelled to sell at the capped price or at a discounted rate to access insurance services offered by G7+. Such a proposition would ensure a consistent flow of LNG to importing countries, prevent abrupt spikes in natural gas prices, and diminish Russia’s revenues from this commodity.

An LNG price cap policy at the price cap level of 17 EUR/MWh, which exceeds Russia’s estimated average production cost, would also serve as a deterrent against them significantly reducing exports by keeping exports flowing.

According to CREA’s calculations based on 2023 values, applying the suggested price cap globally would have cut Russia’s total LNG export revenues by 60%, equivalent to EUR 10 bn, while only enforcing it within the EU would have reduced Russia’s total LNG export revenues by 29%, resulting in a drop of EUR 5 bn.

Key findings

- In 2023, 13% of the EU’s LNG imports by volume were from Russia. This amounted to 17.25 bcm, excluding transshipments to non-EU Member States.

- Imports of Russian LNG accounted for 5% of EU gas consumption, showing the bloc’s relatively low reliance on it. Russia, however, is heavily reliant on the EU market, which was the destination for half of all its LNG exports in 2023.

- In 2023, Russia’s Yamal LNG project exported 26 bcm of LNG, 72% of which was destined for Europe. 86% of exports from the Portovaya and Vysotsk facilities (4.5 bcm) went to Europe.

- In 2023, G7+ countries retained their dominance in shipping Russian LNG. Carriers owned or insured in G7+ countries transported 93% (EUR 15.5 bn) of Russian LNG globally.

- Implementing a global LNG price cap level of 17 EUR/MWh would have slashed Russia’s revenues by 60% in 2023, leading to a drop of EUR 10 bn in their total LNG export revenues. Alternatively, if only the EU imposed a price cap, Russia’s total LNG export revenues in 2023 would have decreased by 29% — a loss of EUR 5 bn.