China currently produces more than 1 billion tons of crude steel annually, which is more than half of the world’s steel production. The dominance of the coal-based blast furnaces-basic oxygen furnace (BF–BOF) method in the Chinese steel sector, along with its large scale, presents significant challenges for decarbonisation efforts. Coal is burned to strip oxygen from the iron ore and this process generates substantial carbon emissions. The low carbon transition of the Chinese steel sector is essential for China’s carbon neutrality target by 2060, as well as for decarbonising the global steel sector. Deep decarbonisation would require substantial investments in zero-emission steelmaking technologies, as well as the early retirement of carbon-intensive facilities yet the sector’s persistent overcapacity and thin profitability is complicating the transition to cleaner steelmaking methods.

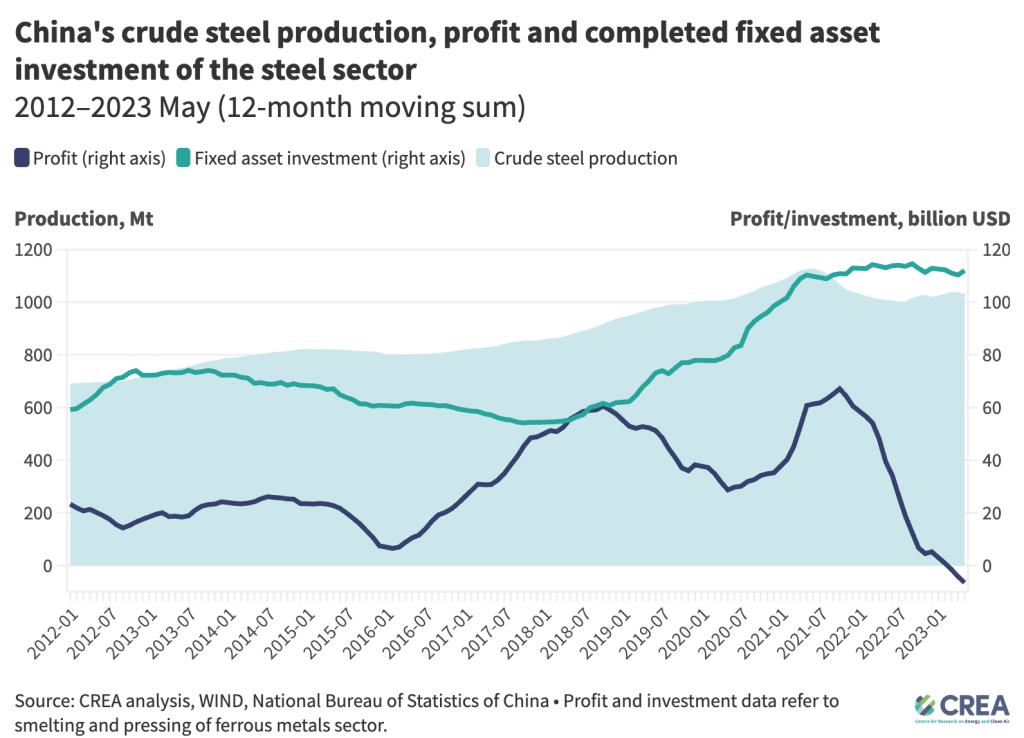

The Center for Research on Energy and Clean Air (CREA)’s latest briefing on the steel sector in China reveals that China’s crude steel output has declined since 2021 due to output control by the government and the decline in downstream demand. However, new investments in iron and steelmaking capacity have so far not adjusted to the new reality. The expansion of the Chinese steel industry demonstrates a close correlation with the nation’s economic development. Excessive investments have persistently inundated the industry, transforming the customary cyclical and short-term overcapacity situation into a protracted and persistent overcapacity issue, referred to as structural overcapacity.

The consequences of this overcapacity significantly impact the sector’s profitability because steel firms find it challenging to operate sustainably at levels below approximately 80% capacity utilisation.

There is an urgent need to align investments in new production capacity in the steel sector with the goal of peaking and reducing CO2 emissions before 2025.

Key findings

- Chinese steel firms are making significant investments in new, coal-based steelmaking capacity. Companies received approvals from provincial governments for 384.3 million tonnes per annum (Mtpa) of new ironmaking capacity, and 425.9 Mtpa new steelmaking capacity from 2017 until the first half of 2023. On average, approximately 30 Mtpa steelmaking capacity was approved every six months, which is almost equal to the total steel capacity of Germany. These new approvals are under the capacity replacement policy, which requires a larger quantity of existing capacity to be retired for all new capacity that is added.

- Approximately 90% of crude steel production in China is using coal-based blast furnace–basic oxygen furnace (BF–BOF) routes, wherein coal is used to extract oxygen from iron ore in BF. This method generates significant carbon emissions, thereby contributing substantially to the high carbon emission intensity in China’s steel sector. However, new iron and steel capacity is continuously dominated by the BF–BOF route. Blast furnaces (BF) account for about 99% of the new ironmaking capacity and basic oxygen furnaces (BOF) account for 70% of the new steelmaking capacity approved in 2017–2023 H1. That is to say, at least one-quarter of China’s existing steelmaking capacity has been renewed to further lock in carbon intensive production during their 40-year lifespan.

- In spite of the ‘dual carbon’ goal pledge announced in 2020, during 2021–2023 H1 there was a total 119.8 Mtpa BF and 76.6 Mtpa BOF approved. To meet the 2060 carbon neutrality goal requires early retirement of carbon-intensive steelmaking facilities. Therefore, the new BF–BOF approved after 2020 alone would result in nearly USD 100 billion (CNY 700 billion) in stranded assets.

- We also saw promising progress on shifting investments into facilities that are less carbon-intensive. New proposed electric arc furnace (EAF) projects significantly increased in 2021–2023 H1, with a total capacity of 52.5 Mtpa approved. EAF steelmaking is promoted under the latest capacity replacement policy. The share of EAF in the newly announced steelmaking capacity grew to 30-40% from 2021. Several non-BF projects with a total capacity of 4.7 Mtpa, applying incremental technology or zero-emission technology in the ironmaking process also received approval.

- By 2025, nearly all new permitted iron and steel projects will commence operations. Through these replacements, approximately 40% of China’s iron and steelmaking capacity will be renewed. China’s steel capacity replacement policy requires steel firms to present both “exit” capacity and “addition” capacity in the capacity replacement application. The exit capacity needs to be larger or equal to the addition capacity, which could ensure a net capacity reduction. However, in practice, effective operating capacity might increase, worsening the excess supply in the market. This is because some of the “exit” iron and steelmaking facilities have remained idle for years, and even though they are not a part of currently effective operating capacity, steel companies use these idle capacities as allocation to apply for new capacity approvals under the capacity replacement policy. In this case, when the new facilities commerce operation, the effective operating capacity will exhibit a net increase.

- The majority, specifically 69%, of the new iron and steel projects development are spearheaded by private steel enterprises, followed by regional state-owned enterprises and central state-owned enterprises, accounting for 26% and 5%, respectively.

Policy recommendations

- Include the steel sector in China’s emissions trading system (ETS) within the 14th five-year-plan period, and the emissions trading system should shift from an intensity-based allocation to an absolute cap.

- Limit new investments in blast furnace capacity and speed up the adoption of electric arc furnaces and hydrogen-based steelmaking technology, to peak CO2 emissions from the iron and steel sector before 2025.