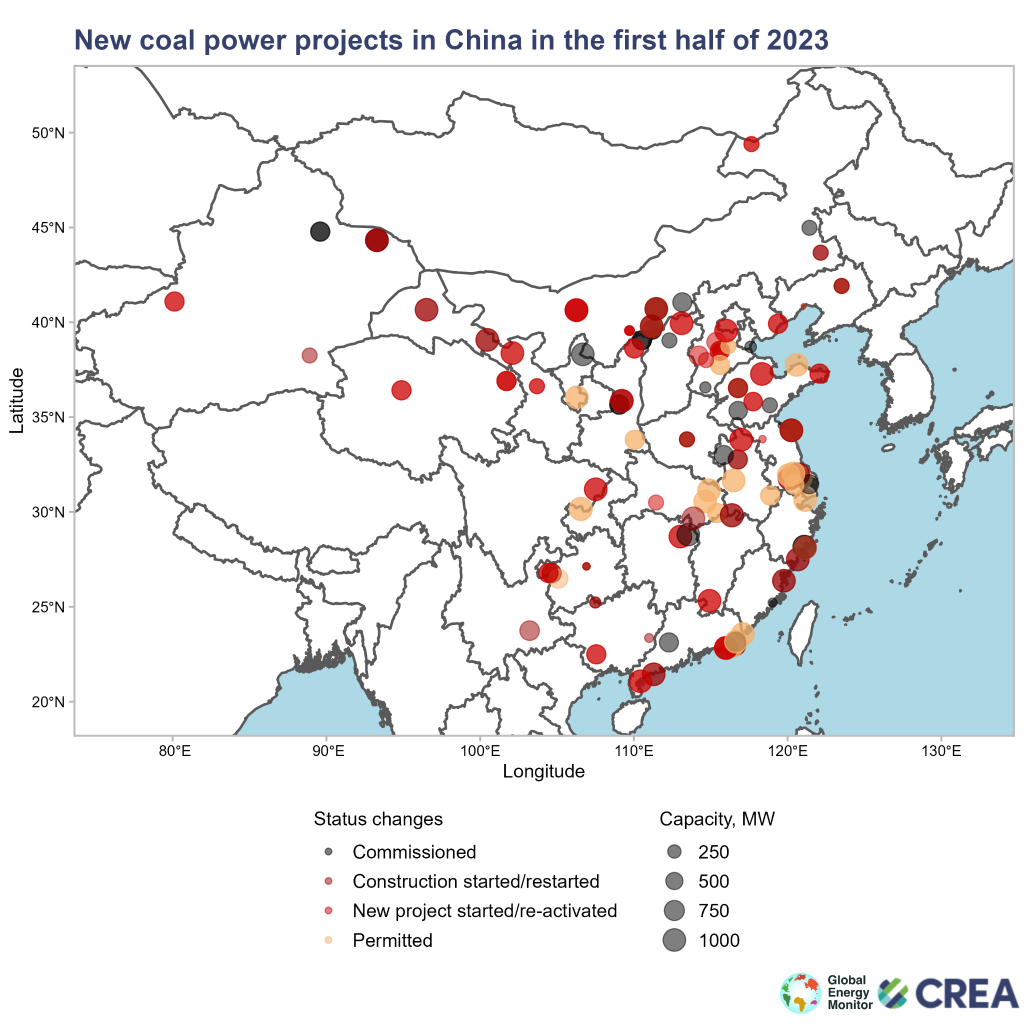

Coal power continues to expand in China, despite the government’s pledges and goals. In the first half of 2023, construction was started on 37 gigawatts (GW) of new coal power capacity, 52 GW was permitted, while 41 GW of new projects were announced and 8 GW of previously shelved projects were revived. Of the permitted projects, 10 GW of capacity has already moved to construction.

Permitting continued apace in the second quarter and in some provinces, newly permitted power plants are moving rapidly into construction, while in others, developers might be securing permits “just in case” and not hurrying to break ground. Of plants permitted in 2022, about half (52 GW) had started construction by summer 2023.

After the permitting spree of the past year, China now has 243 GW of coal-fired capacity currently permitted and under construction.

If the permitting rush is not stopped until projects that are currently announced or in pre-permit stages have gained permits as well, there will be a total of 392 GW of new coal-fired power capacity in the pipeline.

Unless permitting is stopped immediately, China won’t be able to reduce coal-fired power capacity during the 15th five-year plan without subsequent cancellations of already permitted projects or massive early retirement of existing plants.

Key findings

- The coal power plant permitting spree that started in summer 2022 has continued in the first half of 2023 and into July. From January to June, construction was started on 37 GW (gigawatts) of new coal power capacity, 52 GW was permitted of which 10 GW already moved into construction, while 41 GW of new projects were announced and 8 GW of previously shelved projects were revived. All of these parts of the project pipeline are currently running at a pace of more than one coal power plant per week.

- Most of the new projects don’t meet the central government’s requirements for permitting new coal: the provinces building most new coal aren’t using it to “support” a correspondingly large buildout of clean energy; the majority of projects are in provinces that have no shortage of generating capacity to meet demand peaks; and most new project locations already have more than enough coal power to “support” existing and planned wind and solar capacity. This shows that there is no effective enforcement of the policies limiting new project permitting.

- 152 GW has been permitted and 169 GW announced since the start of the current spree in early 2022. This means that China is accelerating the additions of new coal power capacity during the current five-year plan period (2021–25) compared to either of the preceding two five-year plan periods.

- China now has 243 GW of coal power under construction and permitted. When projects currently announced or in the preparation stage but not yet permitted are included, this number rises to 392 GW. This means that coal power capacity could increase by 23% to 33% from 2022 levels, implying either a massive increase in coal power generation and emissions or a massive drop in plant utilization, implying financial losses and potentially asset stranding.

- Unless permitting is stopped immediately, China won’t be able to reduce coal-fired power capacity during the 15th five-year plan (2026–30) without subsequent cancellations of already permitted projects or massive early retirement of existing plants.

Policy recommendations

- Strictly control new coal power capacity and reject or revoke permits to projects that are not necessary for “supporting grid stability” or “supporting the integration of variable renewable energy”.

- Accelerate investment in clean power generation to fully meet growth in electricity demand and stop increasing bulk power generation from coal. Decarbonisation requires substantial changes in network infrastructure, market mechanisms, regulatory framework, and planning processes, which require central government facilitation.

- Increase investment in electricity storage, flexibility and transmission within grid regions. Create a level playing field for different storage, demand response and generation technologies for meeting peak demand, and enable clean flexibility technologies to scale up. While many technologies, such as pumped hydro, lithium-ion battery and demand-side technologies, are as mature as coal power and ready for wider adoption, current power systems and policy frameworks still lead developers to default to coal.

- Strengthen energy efficiency requirements for A/C units and for new buildings, and introduce a program of large-scale energy efficiency improvements for existing buildings.

| About the data The changes in coal power project status analyzed for this briefing are based on the latest July 2023 update of Global Energy Monitor’s Global Coal Plant Tracker (GCPT) and the historical 2014–2023 information available upon request. The permitting dates and related statuses were amended for five projects in the July 2023 data: Changshu-1 power station (Units 7–9: 2023-06-30), Huaneng Taicang power station (Phase III, Units 5–6: 2022-10-28), Ligang power station (Phase V, Units 1–2: 2023-06-30), Lu’an power station (Phase III, Units 5–6: 2023-02-23), and Wangting power station (Units 7–8: 2023-06-30). The GCPT is an online database that identifies and maps every known coal-fired generating unit and every new unit proposed since January 1, 2010 (30 MW and larger). The tracker uses footnoted wiki pages to document each plant and is updated biannually. GCPT is the most detailed dataset available on the global coal power fleet, and has provided biannual updates on coal-fired generating capacity since 2015. |