Russian exports of seaborne crude rose to highest volumes since May 2023, as revenues rose for second straight month

By Vaibhav Raghunandan, Europe-Russia Analyst and Research Writer; Petras Katinas, Energy Analyst; Data Scientist: Panda Rushwood; with contributions from Isaac Levi, Europe-Russia Policy & Energy Analysis Team Lead

Key findings

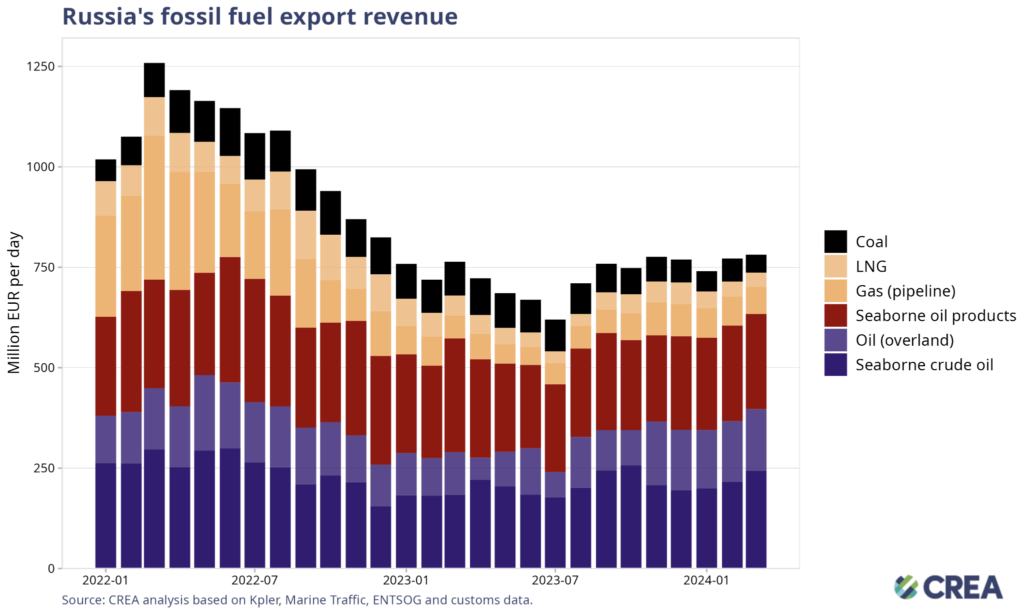

- Russia’s fossil fuel export revenues marginally rose by EUR 9.4 mn per day in March, due in part to a 13% (EUR 28 mn per day) month-on-month increase in export earnings from seaborne crude.

- Russian exports of seaborne crude hit a nine month high in March — and were the third highest volumes recorded since the EU/G7 sanctions and price cap.

- Russian revenues from coal exports fell by a massive 23% (EUR 13.1 mn per day) due in part to rising freight costs and cheaper coal alternatives for Asian markets — Russia’s main buyers since the sanctions.

- China’s imports of Russian Sokol crude hit an all time high (0.97 mn tonnes), as the country took on the Sokol shipments stranded after being turned away from India amidst tightened sanctions from The Office of Foreign Assets Control (OFAC).

- Russian revenues from crude exports to India rose by 48% in March, bucking a recent trend of declining imports. India’s crude oil imports from Russia had been impacted by ongoing issues with payments and OFAC sanctions for the last three months.

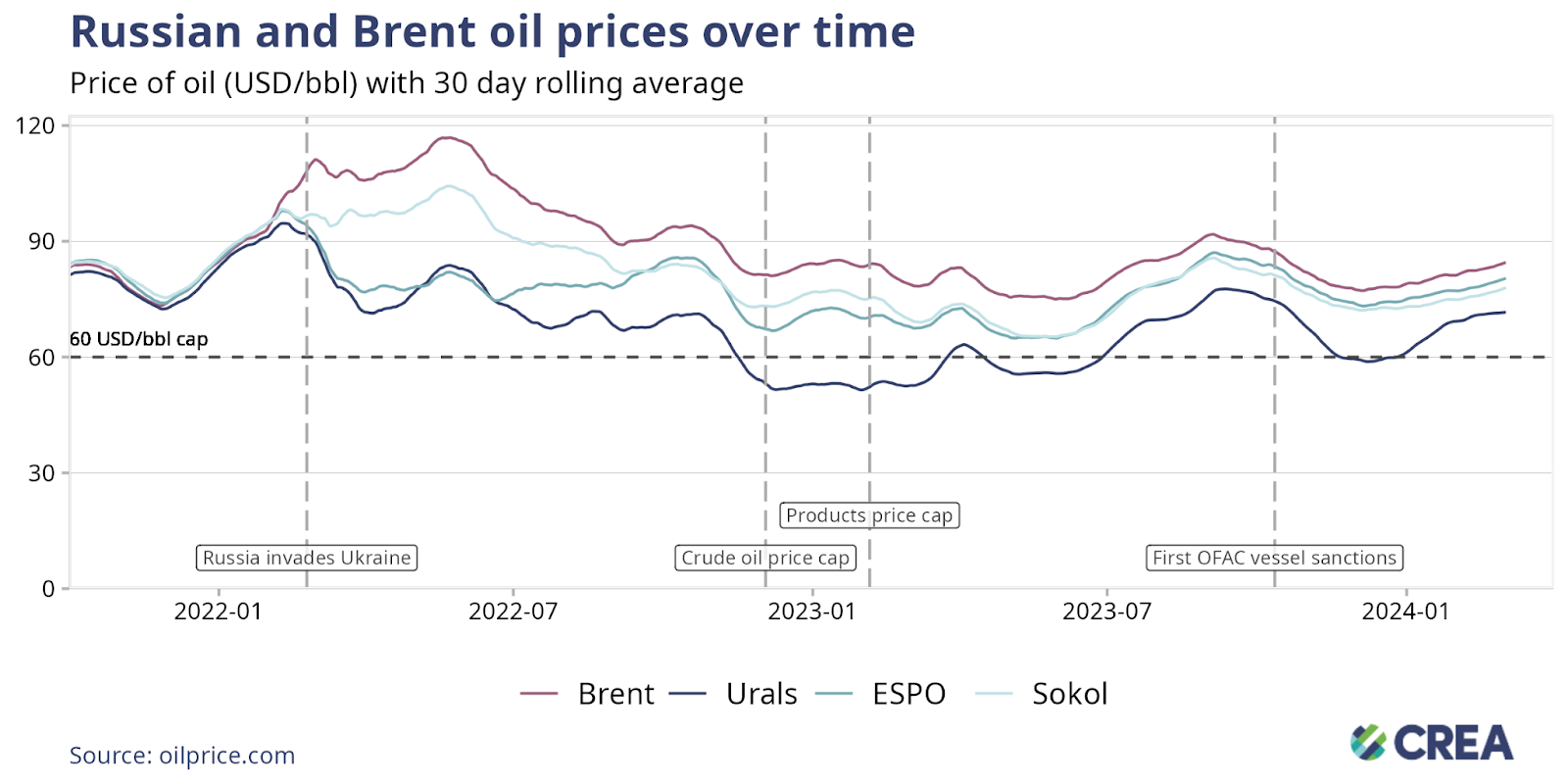

- In March, the average price of Urals and ESPO rose 5% and 4%, respectively. Both grades of oil are being traded significantly above the USD 60 per barrel price cap despite tankers owned or insured in price cap coalition countries continuing to transport these grades of Russian crude.

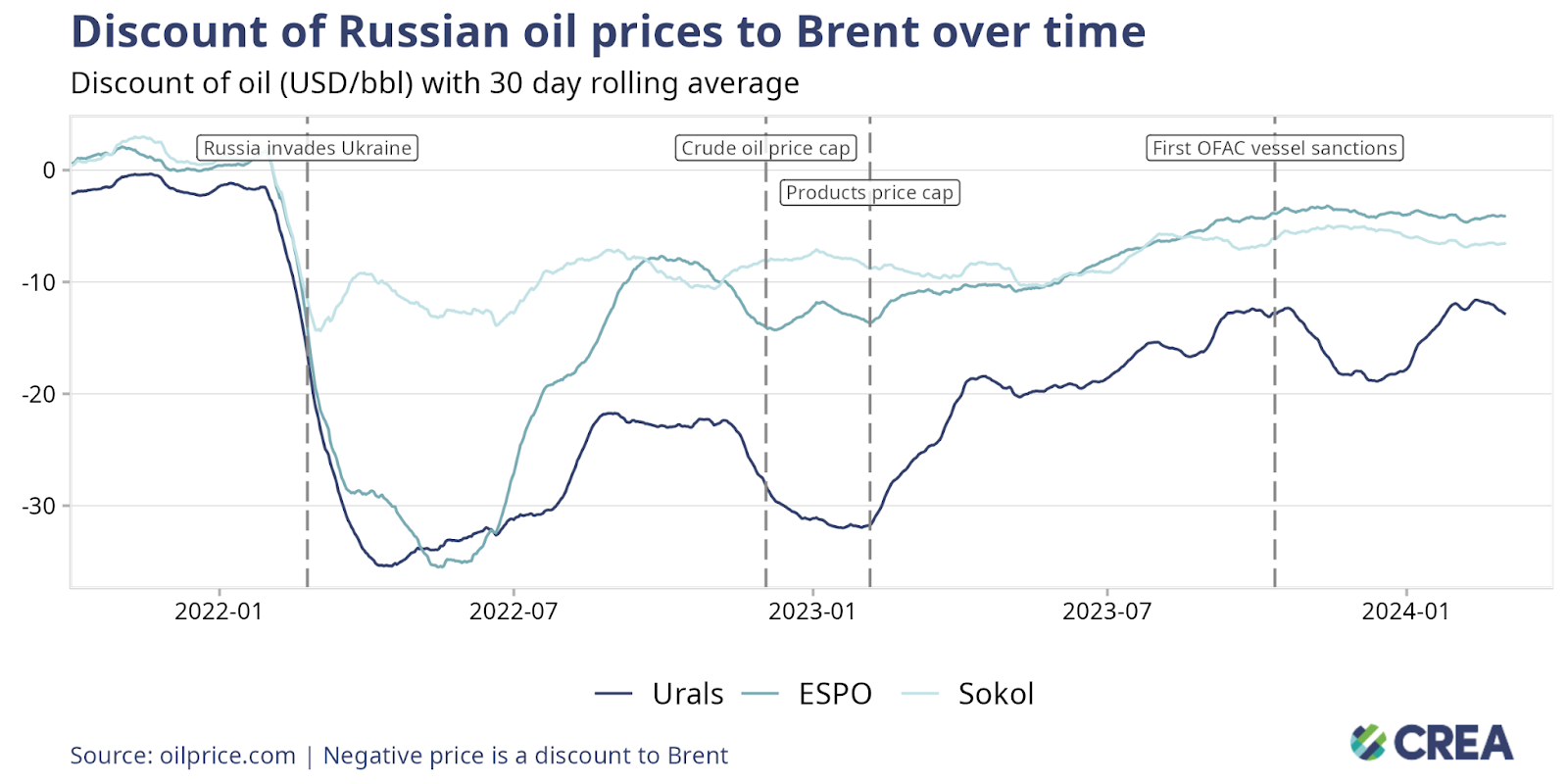

- The widened discount on Russian oil, due to OFAC sanctions in October 2023, has significantly narrowed over the past two months. The average discount on ESPO and Sokol blends was a mere USD 4.12 per barrel and USD 6.5 per barrel, respectively, in March.

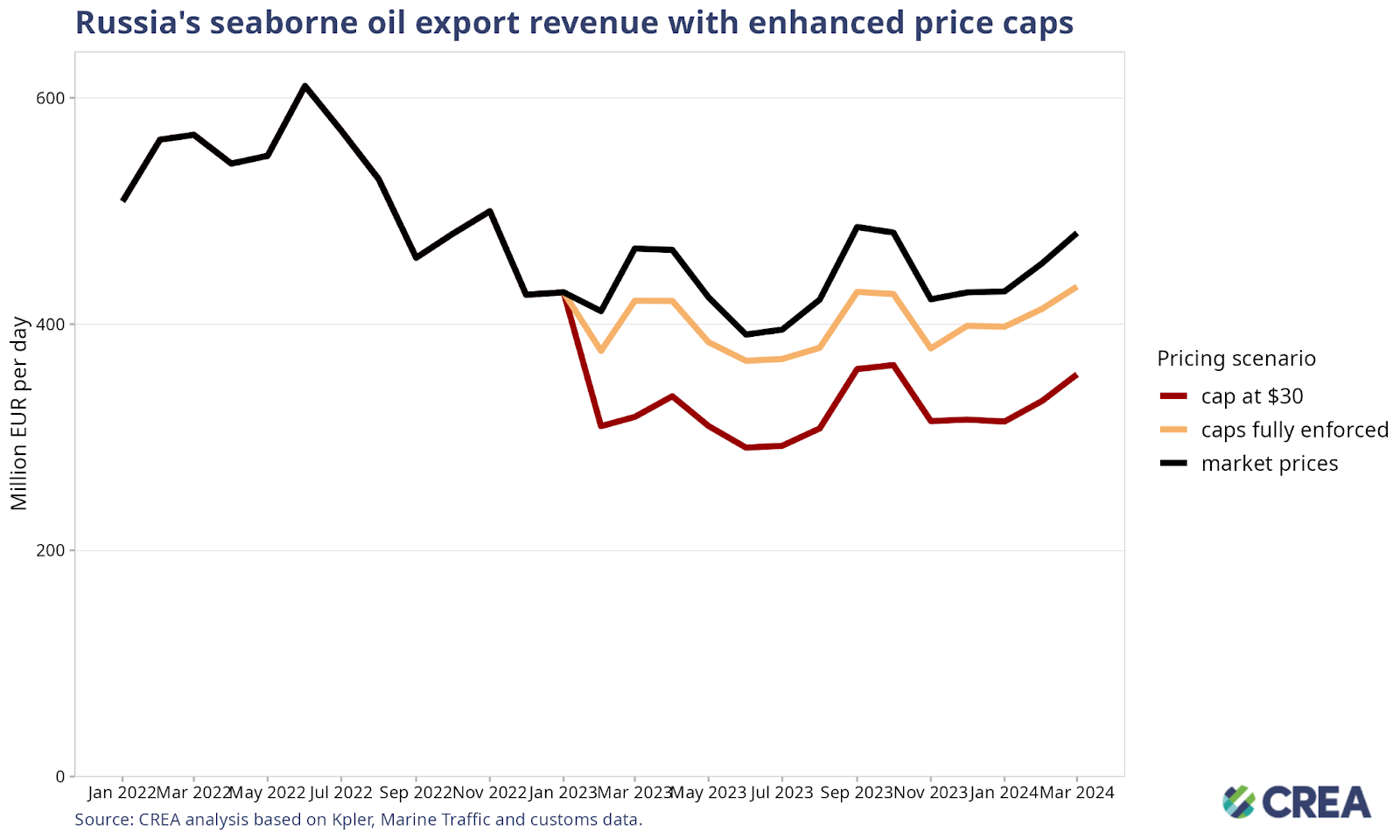

- A lower price cap of USD 30 per barrel would have slashed Russia’s revenue by EUR 50 bn (25%) since the sanctions were imposed in December 2022 until the end of March 2024. A USD 30 per barrel price cap would have slashed Russian revenues by EUR 3.88 bn (26%) in March alone.

Trends in total export revenue

- In March 2024, Russia’s monthly fossil fuel export revenues saw a month-on-month rise of 1% (EUR 9.4 mn per day).

- Monthly revenues from seaborne crude oil rose by 13% (EUR 28 mn per day) and the volumes of Russian exports increased by a similar 9%, reaching their highest level in nine months and third highest since the implementation of oil sanctions in December 2022. Increased Russian exports of crude oil are linked to refinery maintenance following Ukrainian drone attacks on Russian refineries, according to Russia’s First Deputy Energy Minister.

- While Russian revenues from crude oil via pipeline rose by a marginal 1% (EUR 2 mn per day), the volumes of exports saw a month-on-month 2% reduction.

- Revenues from exports of seaborne oil products decreased marginally (EUR 1 mn per day) in March.

- Russia’s revenues from LNG exports and pipeline gas decreased by 2% (EUR 0.75 mn per day) and 8% (EUR 5.5 mn per day), respectively. Revenues from LNG and pipeline gas dropped for a third consecutive month, partly due to reduced European demand.

- Russian revenues from coal exports fell by a massive 23% (EUR 13.1 mn per day) in March. Russian revenues from coal have been in decline since June 2023, and despite a small surge last month, the latest drop is linked to rising freight costs and cheaper coal alternatives for Asian markets — Russia’s main buyers since the sanctions.

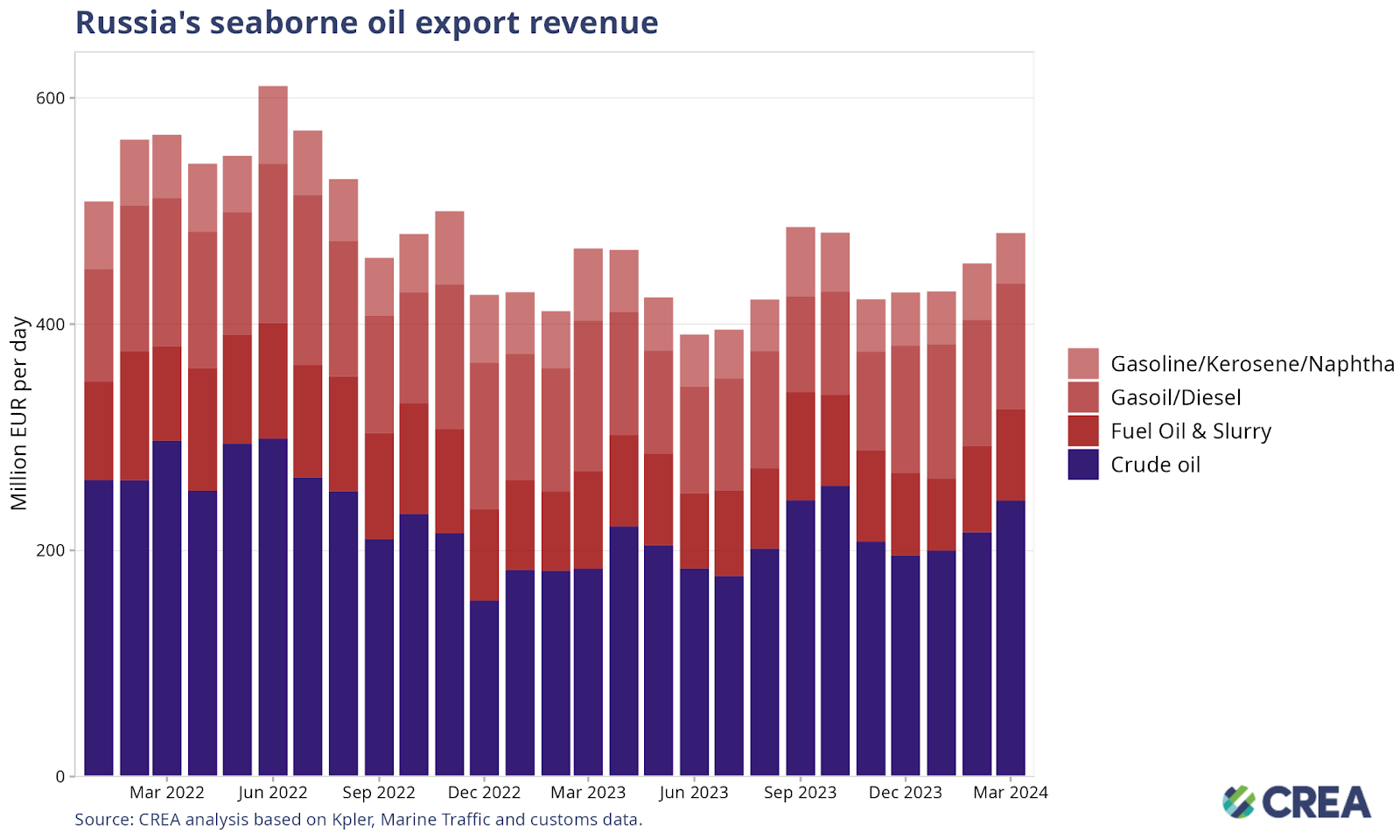

- Russia’s seaborne oil export revenues surged by 6% (EUR 27 mn per day) in March, due in part to a 13% (EUR 28 mn per day) month-on-month increase in export earnings from seaborne crude.

- In March, Russian earnings from fuel oil and slurry exports increased by 6% (EUR 5 mn per day).

- Russia’s export earnings from gasoil and diesel decreased by a marginal EUR 0.5 mn per day in March.

- Export revenues from gasoline, kerosene, and naphtha decreased by 11% (EUR 5.2 mn per day).

| Impact assessment of Ukrainian drone strikes on Russian refineries |

| It is crucial to note that the drone attacks target only oil refineries; thus, they do not directly impact Russian crude oil exports. Disruptions to transport and delivery mechanisms like pipelines, terminals, or carriers, may have impacted prices in a different, substantial way. Russian exports of petroleum products have remained the same in March compared to February. It could be attributed to rebuilding refining capacity, selling existing stocks, or prioritising exports over the domestic market, although the latter seems less probable. A lack of excess crude oil storage may mean that Russia will have to export more crude oil in the upcoming weeks, threatening the commitment to OPEC+ stating that it would cut exports in Q1 of 2024. Since late February, when the drone strikes began on Russian refineries, there has been a noticeable decline in the production of oil products in the Russian market. Data from Rosstat indicates a consistent decrease in output over the past five weeks. For instance, diesel production has fallen by 16%, from 839 thousand tonnes in the 10th week of 2024 to 754 thousand tonnes in the 15th week of 2024. Similarly, petrol production during the same period decreased by 9%, from 1,744 thousand tonnes to 1,585 thousand tonnes. However, despite these disruptions, there has been no significant impact on the retail prices of diesel and the primary grades of petrol (A-92, A-95, A-98) in the market. Nevertheless, Spimex (St. Petersburg International Mercantile Exchange) data shows that wholesale prices of these fuels were impacted. Due to the differences between wholesale and retail prices, we can assume that Russian authorities exert pressure on oil traders to maintain current price levels despite the production challenges caused by the attacks. |

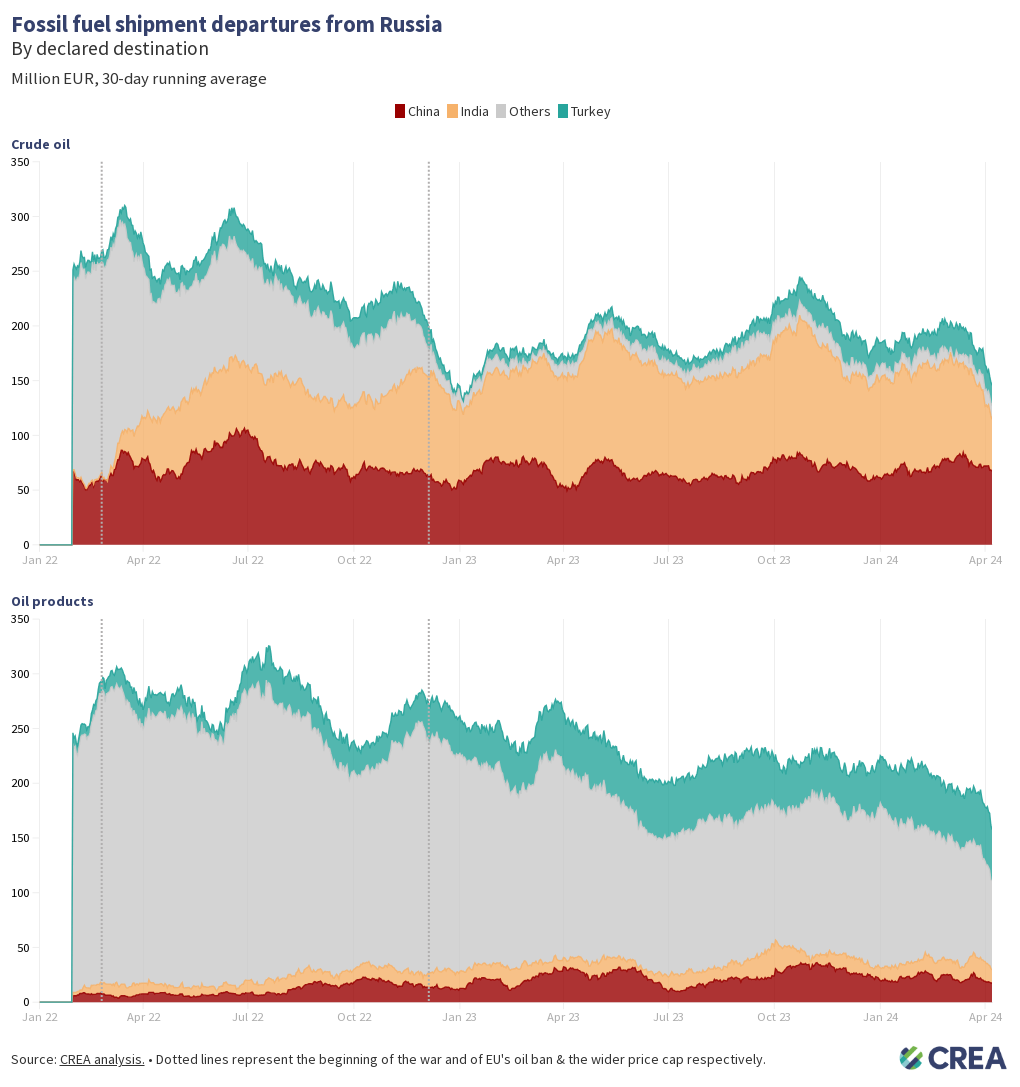

Who is buying Russia’s fossil fuels?

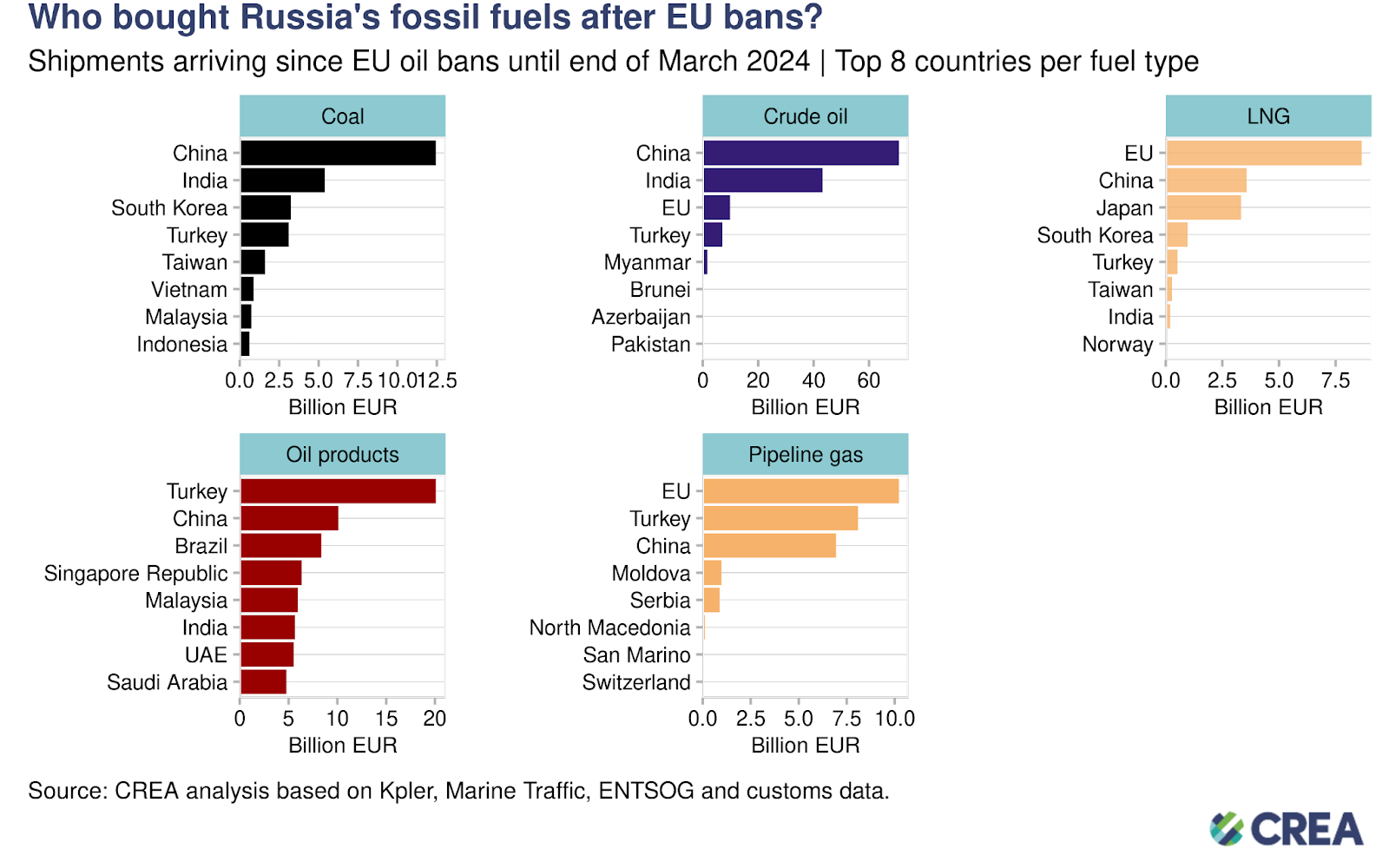

- Coal: China has purchased 42% of all Russian coal exports since 5 December 2022 until the end of March 2024. They are followed by India (18%) and South Korea (11%).

- Crude oil: Since the EU/G7 bans on 5 December 2022, China has bought 53% of Russia’s crude exports, followed by India (32%), the EU (7%), and Turkey (5%). Oil via pipeline is only partially sanctioned. The EU’s crude oil imports have arrived via sea to Bulgaria and via pipeline to the Czech Republic, Slovakia, and Hungary.

- LNG: The EU was the largest buyer, purchasing 49% of Russia’s LNG exports, followed by China (20%) and Japan (19%). No sanctions are imposed on Russian LNG shipments to the EU. As of 11 April 2024, the European Parliament has passed a law that allows Member States to ban Russian LNG imports, by preventing Russian firms from booking gas infrastructure capacity. However, no major importer has indicated that they will use this power to ban Russian LNG imports.

- Oil products: Turkey, the largest buyer, has purchased 25% of Russia’s oil product exports, followed by China (12%) and Brazil (10%). The EU’s sanctions on seaborne Russian oil products were implemented on 5 February 2023.

- Pipeline gas: The EU was the largest buyer, purchasing 38% of Russia’s pipeline gas, followed by Turkey (30%) and China (26%). No sanctions are imposed on Russian pipeline gas imports into the EU.

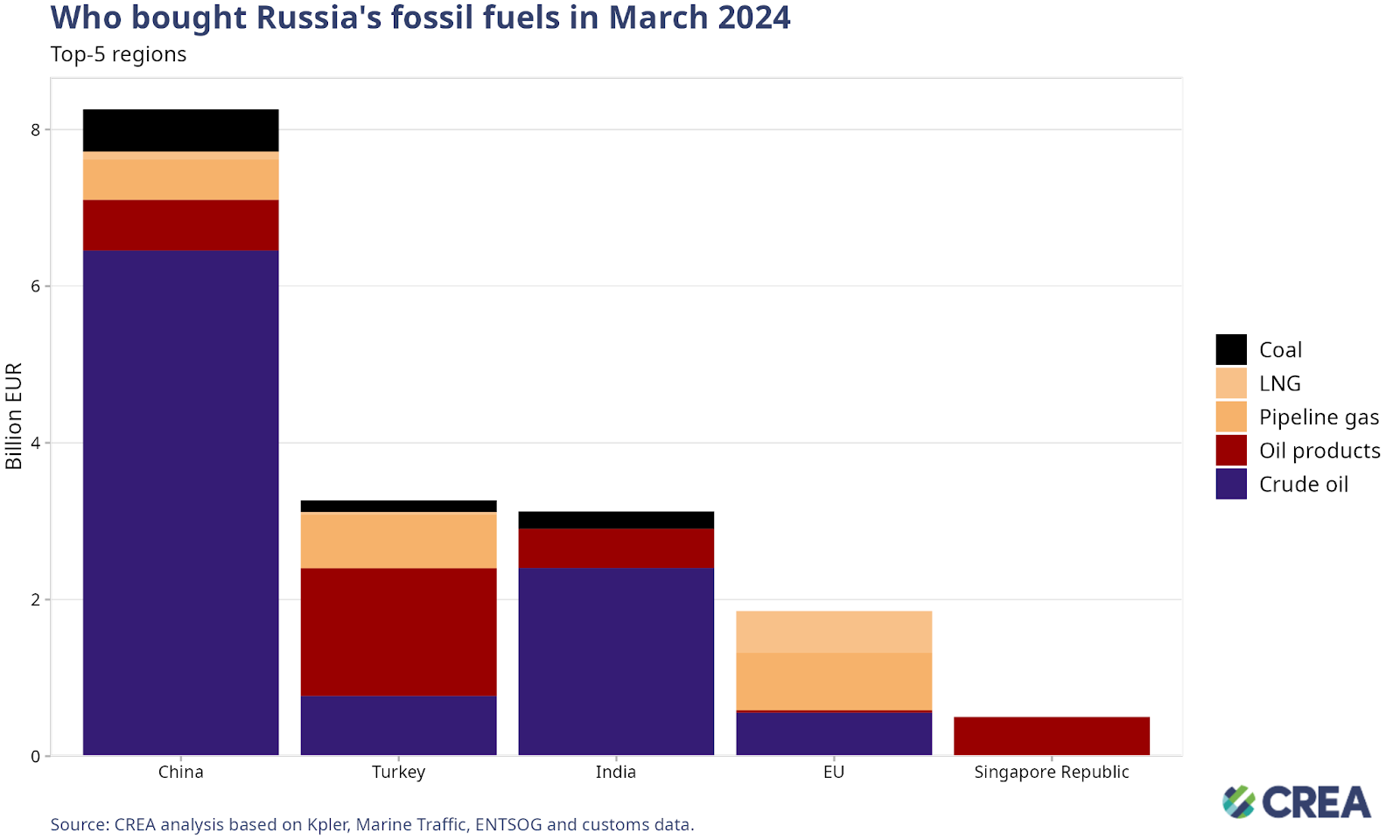

- China was the largest buyer of Russian fossil fuels in March, accounting for 49% of Russia’s total monthly exports, valued at EUR 8.2 bn.

- Turkey’s imports were the second highest, comprising 19% (EUR 3.2 bn) of the total, while India was third with an 18% (EUR 3.1 bn) import share. The EU and Singapore contributed 11% (EUR 1.8 bn) and 3% (EUR 0.5 bn) to Russia’s monthly exports, respectively.

- Crude oil comprised 78% (EUR 6.4 bn) of China’s total imports from Russia. Oil products, pipeline gas, and coal comprised 8% (EUR 0.64 bn), 6% (EUR 0.51 bn) and 7% (EUR 0.53 bn), respectively. China also imported EUR 0.10 bn of LNG from Russia in March.

- China’s total import volumes of crude oil rose 2% in March, but imports from Russia reduced by 3% (0.18 mn tonnes). Despite the decrease in volumes of Russian imports, revenues from crude saw an 8% (0.47 bn tonnes) increase — mainly due to China’s increased imports of the higher priced Sokol grade crude oil.

- This trend was far more visible in China’s imports of oil products. While China’s global imports of oil products rose 2%, imports from Russia reduced by a massive 24%.

- China’s imports of Sokol crude hit an all time high (0.97 mn tonnes), as the country took on the Sokol shipments stranded after being turned away from India amidst tightened OFAC sanctions.

- Half of Turkey’s total imports of fossil fuels from Russia consisted of oil products (EUR 1.6 bn). Crude oil (24% valued at EUR 0.77 bn) and pipeline gas (21% valued at EUR 0.68 bn) were the two other commodities majorly imported by Turkey in March. The remainder of their imports consisted of coal (EUR 0.15 bn) and LNG (EUR 0.03 bn).

- Turkey’s total import volumes of petroleum products rose 8% in March, mostly due to a massive 15% rise in the volume of imports from Russia. Turkey has been the largest importer of oil products from Russia since the EU/G7 ban on refined oil products in February 2023. Despite the operators of the Ceyhan port in Turkey announcing a shutting off of Russian imports last month, Russian oil has continued to flow into the port. In March, the port received 0.11 mn tonnes of oil products from Russia — the entirety of their imports for the month.

- Turkey’s crude oil imports from Russia rose by 8% in March, accounting for over two-thirds of their total crude imports for the month.

- Crude oil accounted for 77% (EUR 2.4 bn) of India’s total fossil fuel imports from Russia for the month. Oil products accounted for 16% (EUR 0.5 bn), and coal accounted for 7% (EUR 0.22 bn) of their total imports in March.

- Russian revenues from crude exports to India rose by 48% in March, bucking the trend over the past two months. India’s crude oil imports from Russia had been impacted by ongoing issues with payments and The Office of Foreign Assets Control (OFAC) sanctions for the last three months. In March, the country’s global import volumes of crude saw a sharp 13% spike, mirroring a similar 15% rise in imports from Russia.

- India’s imports of Russian crude (7.02 mn tonnes) in March were the highest volume since September 2023.

- The EU’s imports of fossil fuels from Russia consisted of pipeline gas (40% valued at EUR 0.73 bn), LNG (29% valued at EUR 0.53 bn), crude oil (30% worth EUR 0.55 bn), and oil products via pipeline (EUR 0.03 bn).

- In March, Singapore’s Russian fossil fuel imports consisted entirely of oil products valued at EUR 0.5 bn.

- Landlocked Central and Eastern European countries and some Southern European countries received Russian fossil gas via pipeline through Ukraine and TurkStream in March 2024. Crude oil was obtained via the Druzhba oil pipeline. The EU has not banned fossil gas and crude oil via pipelines.

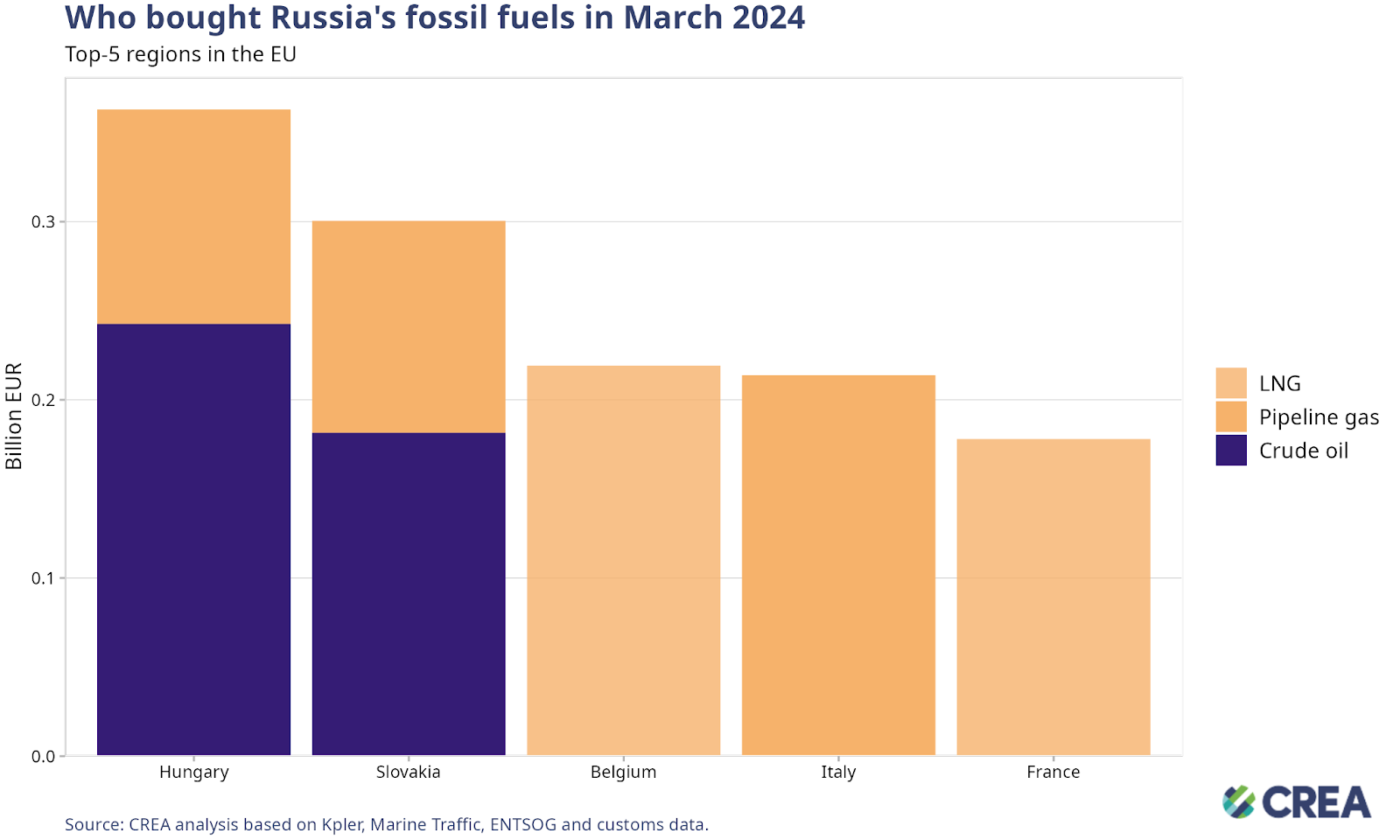

- Hungary was the largest importer of Russian fossil fuels within the EU in March, importing fossil fuels worth EUR 362 mn. Imports comprised of crude oil and gas, delivered via pipelines, valued at EUR 242 mn and EUR 120 mn, respectively. While there was a 9% month-on-month decrease in Hungary’s pipeline gas imports from Russia, crude oil imports rose for a second straight month — by 9% (EUR 16 mn).

- Slovakia’s imports of Russian fossil fuels dropped by a marginal 1% in March. While there was a 7% drop in their imports of pipeline crude, a 10% rise in imports of pipeline gas compensated for it.

- The entirety of Belgium’s imports of Russian fossil fuels in March consisted of LNG valued at EUR 219 mn. Russian LNG comprised 59% of Belgium’s total LNG imports in March. Belgium’s total volume of LNG imports rose by 36% in March mirroring a similar 41% rise in their imports from Russia. Belgium’s LNG re-exports dropped by 18% in March — almost the entirety of it directed towards Spain and China.

- Italy was the EU’s fourth-largest importer of Russian fossil fuels, importing EUR 213 mn of pipeline gas. Italy’s increased imports come at a time when the country has just shelved plans to introduce a tariff to ensure gas storage facilities remain full.

- In March, France was the EU’s fifth-largest importer of Russian fossil fuels. The entirety of their imports consisted of LNG valued at EUR 161 mn.

How are oil prices changing?

- In March, the average Urals Europe cost and freight (CFR) spot price saw a month-on-month 5% rise to stay significantly above the price cap at USD 76.59 per barrel.

- The prices for the East Siberia Pacific Ocean (ESPO) and Sokol blends of Russian crude oil, primarily associated with Asian markets, rose 4% in March. The average price for ESPO was USD 80.53 per barrel in March.

- The Urals grade of crude was traded at an average discount of USD 12.8 per barrel in comparison to Brent crude oil in March. The discount had dropped to USD 18.3 in November last year as a result of OFAC sanctions on certain vessels carrying Russian oil, but has since recovered.

- The discount on the ESPO grade and Sokol blends remained at a relatively modest USD 4.12 per barrel and USD 6.5 per barrel respectively.

- Throughout this period, vessels owned or insured by the G7 and European countries continued to load Russian oil in all Russian port regions. These cases call for further investigation for breach of sanctions.

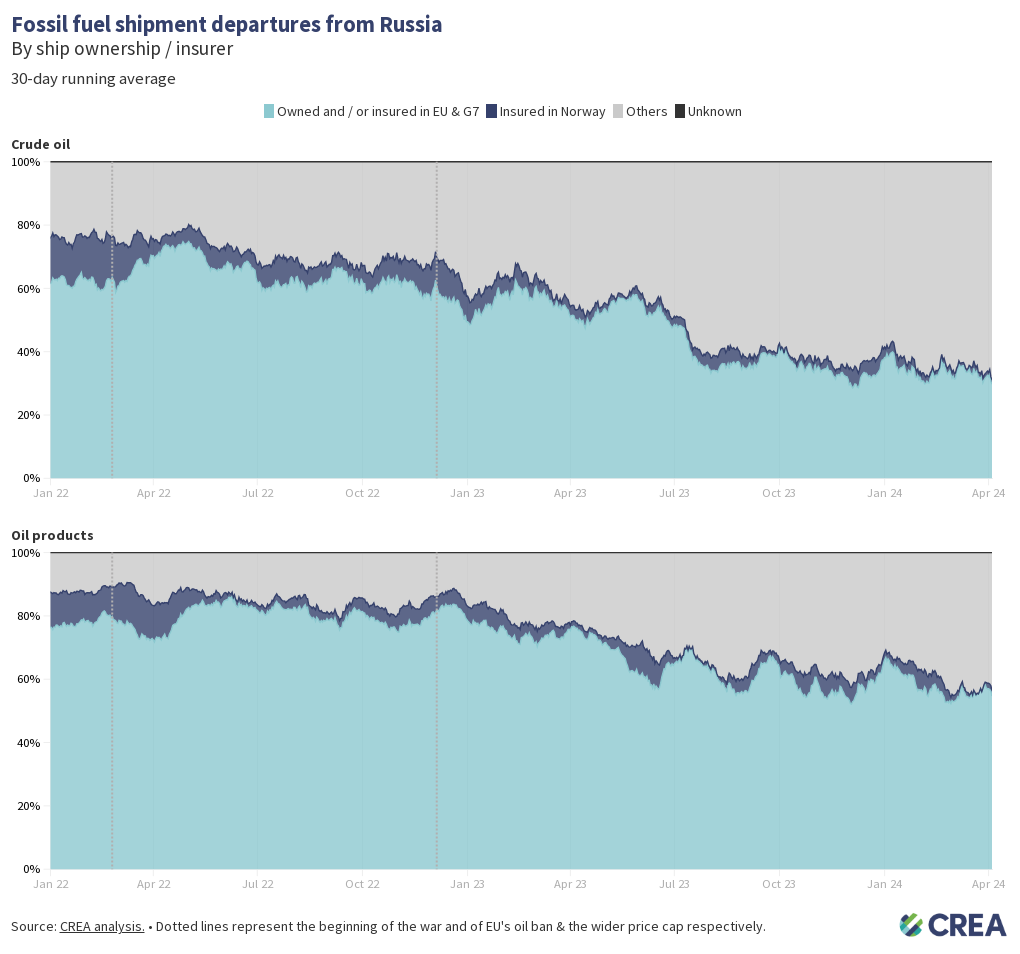

Russia remains highly reliant on the European and G7 shipping industry

- In March, 46% of Russian oil and its products were transported by tankers subject to the oil price cap. The remainder was shipped by ‘shadow’ tankers and was not subject to the price cap policy. A higher proportion of Russian crude oil was transported on ‘shadow’ tankers than oil products.

- 64% of Russian crude oil was transported by ‘shadow’ tankers, while tankers owned or insured in countries implementing the price cap accounted for 36%.

- ‘Shadow’ tankers transporting oil products handled 39% of Russia’s total volume of products. The remaining volume was shipped by tankers subject to the price cap policy.

- Tankers in the Pacific region were loaded with Russian oil at ports like Kozmino in Russia, where the ESPO pipeline ends and is connected to a Kozmino oil terminal. Here, the ESPO crude oil grade is exported at prices exceeding the cap.

- Russia’s reliance on EU/G7 owned or insured vessels provides the Price Cap Coalition with adequate leverage to lower the price cap and implement better monitoring and enforcement that would considerably lower Russia’s oil export revenues.

How can Ukraine’s allies tighten the screws?

- Russia’s fossil fuel export revenues have fallen since sanctions were implemented, showing their impact on Putin’s ability to fund the war. However, much more should be done to limit Russia’s export earnings and constrict the Kremlin’s war chest. This includes lowering the oil price cap, increasing monitoring and enforcement of sanctions, and banning unsanctioned fossil fuels such as LNG and pipeline fuels that are legally allowed into the EU.

- In addition to the EU implementing a full ban on Russian LNG — to ensure energy security and allow countries highly reliant on Russian LNG to phase out — a price cap on Russian LNG must be implemented. A global LNG price cap level of EUR 17/MWh would have slashed Russia’s revenues by 60% in 2023, that is EUR 10 bn of their total LNG export revenues. Alternatively, if only the EU imposed a price cap, Russia’s total LNG export revenues in 2023 would have decreased by 29% (EUR 5 bn).

- The implementation of an LNG price cap policy could utilise the leverage that G7/EU countries have in transporting Russian LNG. 93% of all Russian LNG exports in 2023 were carried on tankers that were owned or insured in G7/EU countries.

- Sanctioning countries must take measures to prevent Russia’s growth in ‘shadow’ tankers that are immune to the oil price cap policy. Sanction-imposing countries should ban the sale of old tankers to owners registered in countries that do not implement the oil price cap policy. This would help limit the increase of ‘shadow’ tankers observed since Russia invaded Ukraine.

- EU/G7 countries must plug the refining loophole, banning the importation of oil products produced from Russian crude oil. This would enhance the impact of the sanctions by disincentivizing third countries from importing large amounts of Russian crude and help cut Russian revenues. Banning the imports of oil products from refineries that process Russian crude oil would also lower the price of Russian oil as they would struggle to find buyers or expand their market.

- A lower price cap of USD 30 per barrel (still well above Russia’s production cost that averages USD 15 per barrel) would have slashed Russia’s revenue by EUR 50 bn (25%) since the sanctions were imposed in December 2022 until the end of March 2024. A USD 30 per barrel price cap would have slashed Russian revenues by EUR 3.88 bn (26%) in March alone.

- Lowering the price cap would be deflationary, reducing Russia’s oil export prices and inducing more production from Russia to make up for the drop in revenue.

- Since introducing sanctions until the end of March 2024, thorough enforcement of the price cap would have slashed Russia’s revenues by 9% (EUR 17.05 bn). In March alone, full enforcement of the price cap would have slashed revenues by 10% (approximately EUR 1.47 bn).

- Enforcement agencies overseeing the sanctions must take proactive measures against violating entities, including insurers registered in price cap coalition countries, shippers and vessel owners.

- Despite clear evidence of violations, there must be more enforcement by agencies implementing penalties against shippers, insurers, or vessel owners and this information must be shared in the public domain. Penalties against violating entities increase the perceived risk of being caught and serve as a deterrent.

- Penalties for those guilty of violating the price cap must be significantly harsher. Current penalties include a 90-day ban of vessels from securing maritime services after violating the price cap, a mere slap on the wrist. Vessels should be fined and banned in perpetuity if found guilty of violating sanctions.

- OFAC and the Office of Financial Sanctions Implementation (OFSI) must continue to sanction ‘shadow’ tankers as doing so hinders Russia’s ability to transport its oil above the price cap. CREA estimates that OFAC’s sanctioning of ‘shadow’ tankers has widened the discount that Russia offers buyers of its oil and cuts Russia’s crude oil export revenues by 5% (EUR 512 mn per month).

- The lack of proper monitoring and enforcement and rising oil prices have increased Russia’s export revenues to fund its war against Ukraine.

Relevant reports:

- Leveraging interdependence: An LNG Price Cap would have cut Russian revenues by 60% in 2023

- Russia’s ‘shadow’ tankers hit a wave of crises

- Russia and North Korea engage in oil for weapons trade

- France’s addiction to an unsustainable energy model

- France talks tough on Ukraine while gobbling up more Russian gas

| Note on methodology: Update 2023-10-19 – We now use Kpler to estimate seaborne exports from Russia and other countries. This change increases our tracker’s estimate of exports from Russia to the world by EUR 77.8 bn (+18% increase) and the exports to the EU by EUR 12.4 bn (+2.8% increase).We have also changed how we receive protection and indemnity (P&I) insurance information about ships to obtain data from known P&I providers directly and from Equasis. This ensures we have recorded the correct start date for a ship’s insurance.Find out more details on the changes in our methodology explained in our article about the migration from automatic identification system (AIS) data providers to the Kpler dataset.Data used for this monthly report is taken as a snapshot at the end of each month. Data on trades and shipments of oil are revised and verified by the data provider through the month. We subsequently update this verified data each month to ensure accuracy. This might mean that figures for the previous month change in our updated subsequent monthly reports. For consistency we do not amend the previous month’s report, and instead treat the latest one as the most accurate data for revenues and volumes. |