- Russia’s fossil fuel export earnings hit the lowest monthly value since the beginning of the invasion.

- Russia’s fossil fuel export revenues fell for the third consecutive month to EUR 591 mn per day in June 2023, 8% lower than May and 18% below April levels.

- The largest drop in Russia’s fossil fuel export value was in seaborne crude oil, falling EUR 24 mn per day (-12%) in June compared to May 2023.

- Russian fossil fuel exports to China are down 15% in value terms for June 2023 compared to May, whilst falling by 24% to India compared to the prior month.

- Russia’s oil export revenues fell to EUR 397 mn per day in June 2023, 7% lower than May and 16% below April levels. Russia’s oil export earnings hit the lowest monthly value in June 2023 since the beginning of their invasion of Ukraine.

- Crude oil export earnings were down 12% or dropped EUR 24 mn per day in June compared to the prior month.

- Crude oil exports to India fell 29% in June compared to May 2023 and crude oil exports to China were at the same levels in value terms . Oil product exports to China fell 63% in June compared to May 2023.

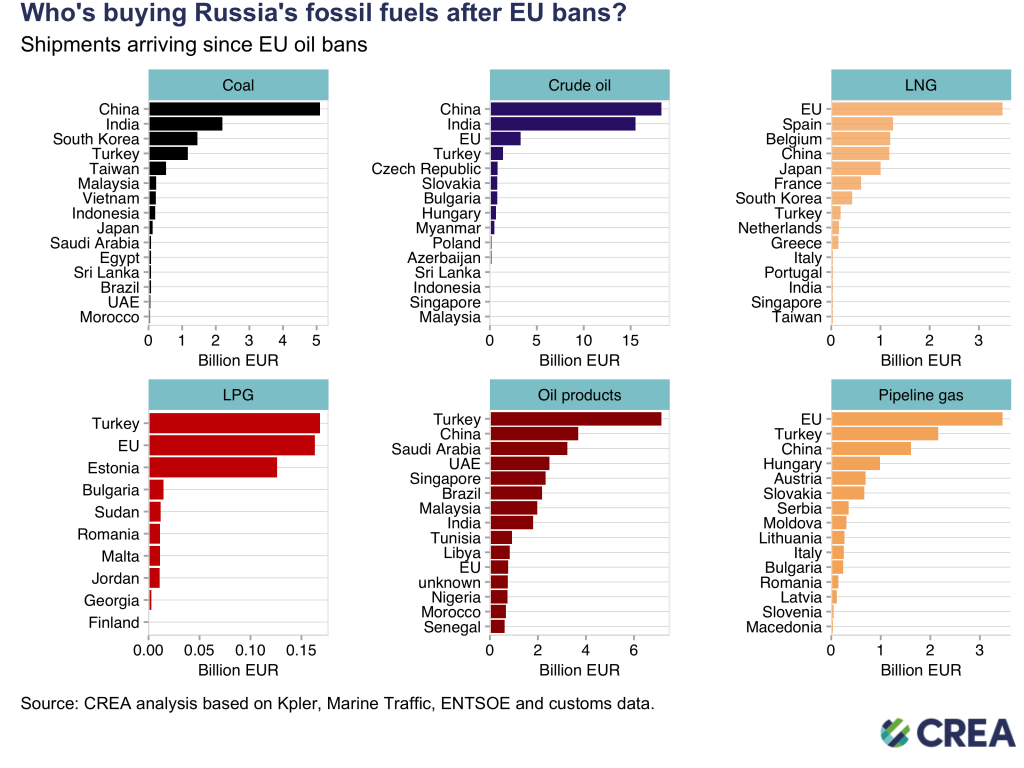

- Coal: since the EU import ban on Russian crude oil was implemented (5th December 2022), China was the largest buyer (purchasing 44% of Russia’s coal exports), followed by India (19%) and South Korea (12%).

- Crude oil: China was the largest buyer (purchasing 43% of Russia’s crude oil exports), followed by India (36%), the EU (8%) and Turkey (3%). EU imports of crude oil since the 5th December 2022 arrived via sea to Bulgaria and via pipeline for the Czech Republic, Slovakia, Hungary, Poland and Germany. Bulgaria has received an exemption to the Russian oil import ban and pipeline oil into the EU is also non-sanctioned.

- LNG: since the 5th December 2022, the EU was the largest buyer (purchasing 35% of Russia’s LNG exports), followed by China (12%) and Japan (10%). No sanctions are imposed on Russian LNG shipments to the EU.

- LPG: Turkey was the largest buyer (purchasing 33% of Russia’s LPG exports), closely followed by the EU (32%).

- Oil products: since the EU import ban on Russian crude oil was implemented, Turkey was the largest buyer (purchasing 24% of Russia’s oil products), followed by China (12%) and Saudi Arabia (11%). EU sanctions on seaborne Russian oil products were implemented on the 5th February 2023, oil via pipeline is only partially sanctioned.

- Pipeline gas: The EU was the largest buyer (purchasing 31% of Russia’s pipeline gas), closely followed by Turkey (19%) and China (14%). No sanctions are imposed on Russian gas via pipeline into the EU.

- In June, China was the largest importer of Russian fossil fuels importing mostly crude oil but also coal, oil products, LNG & pipeline gas.

- India was the second largest importer of Russian fossil fuels, purchasing mostly crude oil but also oil products and coal.

- Turkey imported mostly oil products but also purchased crude oil, pipeline gas, coal and LPG.

- The EU was the fourth largest buyer of Russian fossil fuels in June, buying crude oil (via pipeline or via sea into Bulgaria), pipeline gas, LNG, oil products via pipeline and LPG.

- Saudi Arabia was the fifth largest importer, purchasing oil products, crude oil and coal.

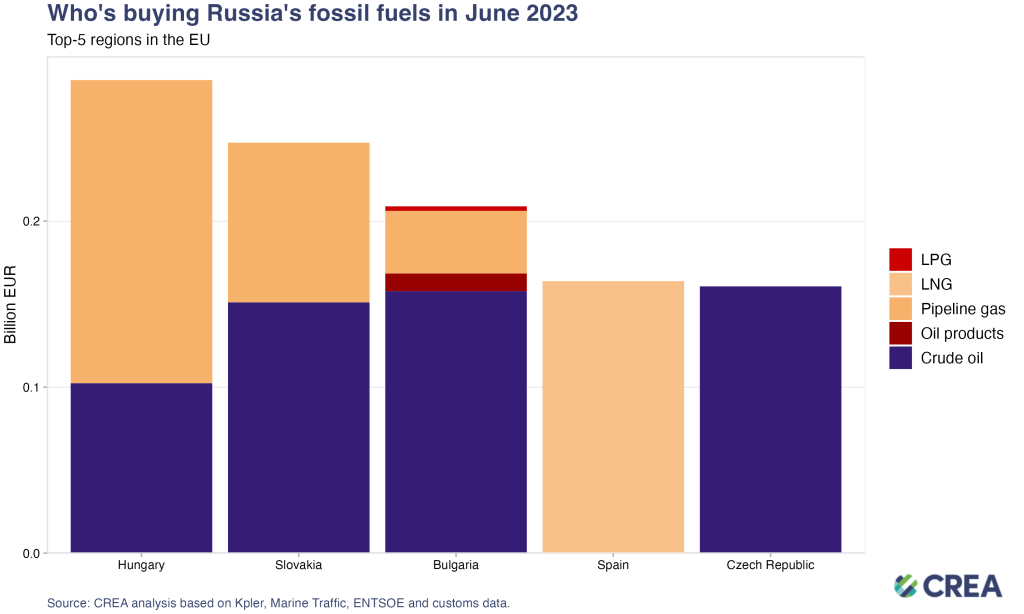

- The largest EU importers of Russian fossil fuels in June 2023 were Hungary, Slovakia, Bulgaria, Spain and Czech Republic.

- Sikka port in India is the largest oil product export port to those sanction imposing countries, and the largest importing port in the world of seaborne crude oil from Russia. The port serves the Jamnagar refinery.

- The top ports importing Russian fossil fuels from Russia in June 2023 were Vadinar (India), Sikka (India), Yarimca-Izmit Port (Turkey), Fujairah (UAE)and Dongjiakou (China).

- Vadinar port supplies an oil refinery located nearby which is owned by Nayara Energy Limited, Rosneft (the second largest Russian state controlled company) possesses a 49.13% share of Nayara Energy Limited. Rosneft or other oil companies from Russia are free to transport crude oil to Vadinar, where it is refined and can be exported to sanction imposing countries legally as oil products from India. This refinery loophole should be addressed and imports from refineries that run on Russian crude oil should be banned by sanction imposing countries.

- Fossil fuel export earnings from Russia fall in June, shipments to India decrease in comparison to prior months. Fossil fuel exports from Russia have fallen since sanctions were implemented, showing the impact they have had at lowering Putin’s ability to fund the war. However, much more should be done to limit Russia’s export earnings and constrict the Kremlin’s warchest such as lowering the oil price cap, increasing monitoring & enforcement of sanctions and banning unsanctioned fossil fuels such as LNG, LPG and pipeline fuels that are legally allowed into the EU.

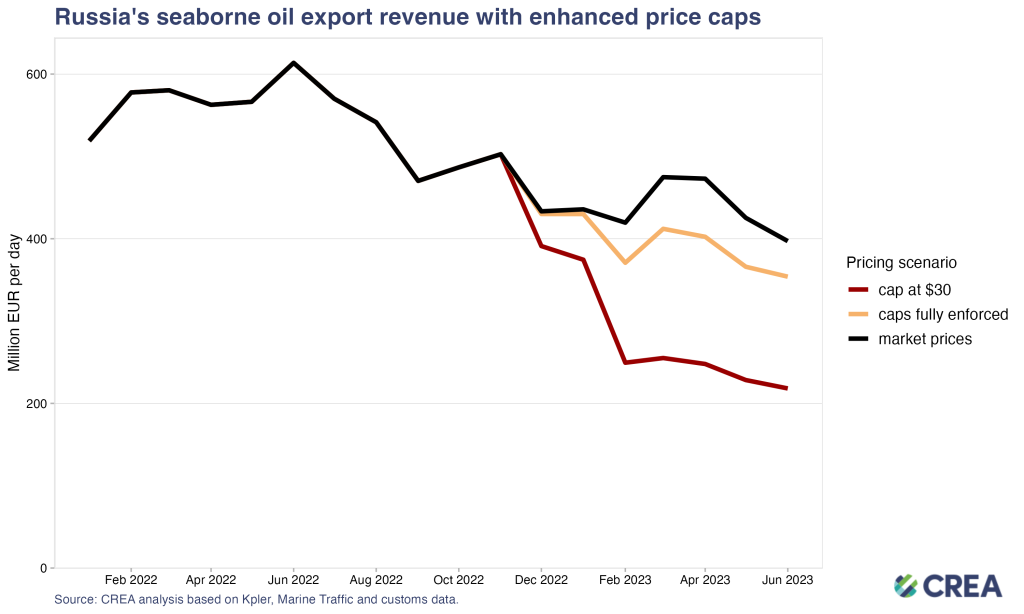

- Russian revenues could have been slashed by EUR 30 bln (46%) by setting the cap for crude oil at USD 30 per barrel (still well above Russia’s production costs, averaging USD 15).

- Lowering the cap would be deflationary, reducing Russia’s oil export prices & inducing more production from Russia to make up for the drop in revenue.

- Full enforcement at the caps current level would have cut Russia’s oil export revenue by approximately EUR 2 bln, or 12%, in April alone when prices were above the USD 60 per barrel.

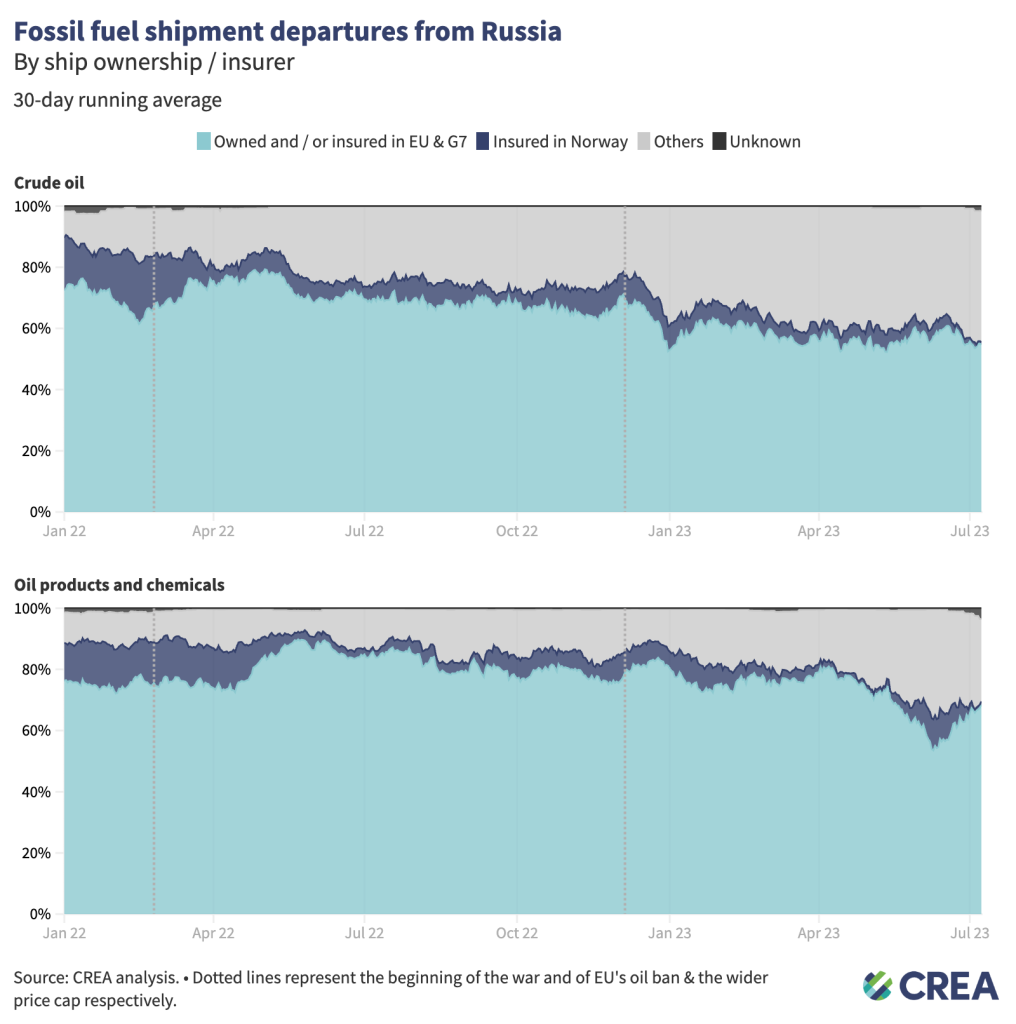

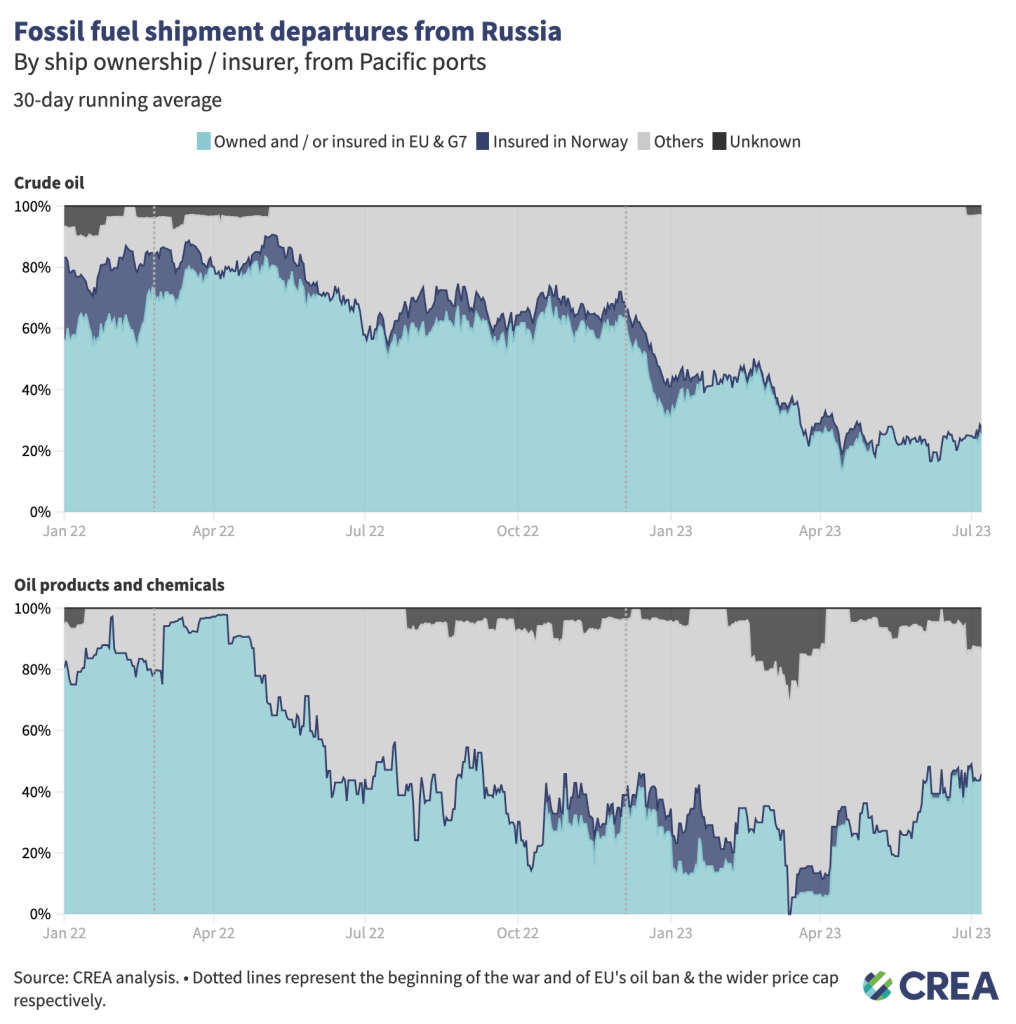

- The share of tankers covered by the price cap in crude oil shipments out of Russia stayed between 55% – 60% in June. For oil products & chemicals, the coverage of the price cap coalition has fallen slightly to around 65% in June from around 70% in May.

- The share of tankers using the price cap countries’ insurance or owned vessels to transport fossil fuels from Russia’s Baltic & Black sea ports is much higher than in Pacific ports.

- The high proportion of shipments transporting Russian oil with EU/G7 insurance and/or vessels outlines how strong a set of tools the price cap coalition has to force down Russia’s oil export revenues by lowering the price cap whilst implementing better monitoring & enforcement measures.

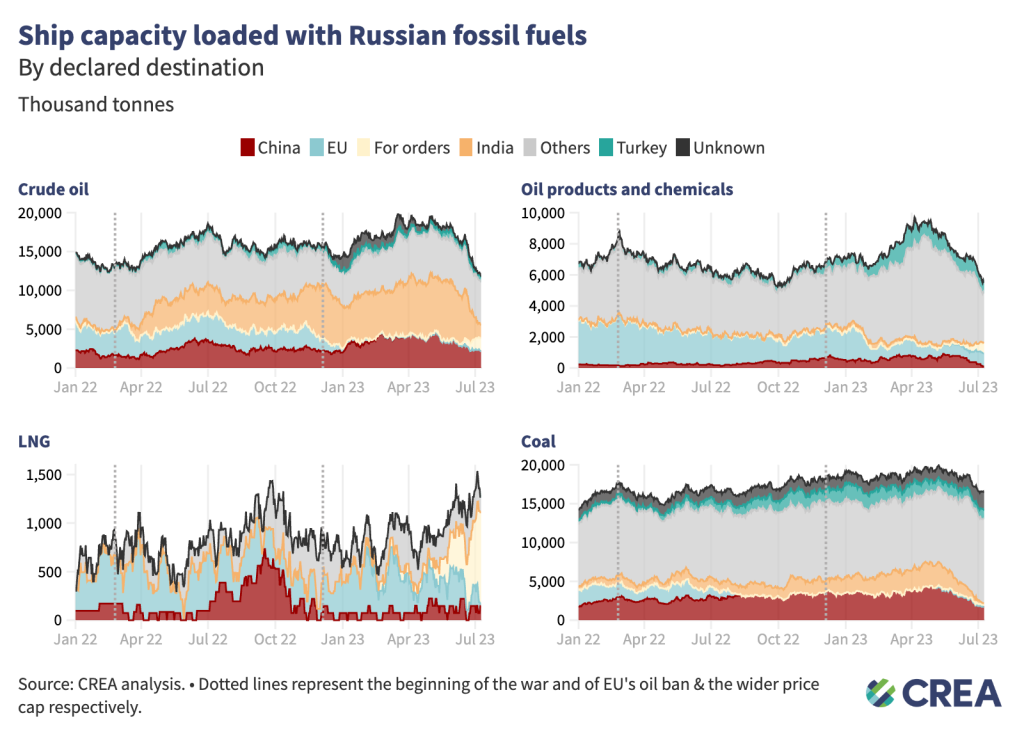

- The amount of crude and oil products loaded on water continues to reduce in June compared to May, shipments to China & India fell. The volume of outgoing crude oil and oil products & chemicals shipments has fallen in recent weeks, indicating falling export revenues. The amount of LNG loaded on water remains high and reaches a peak since before Russia’s invasion of Ukraine, signalling an ongoing glut.

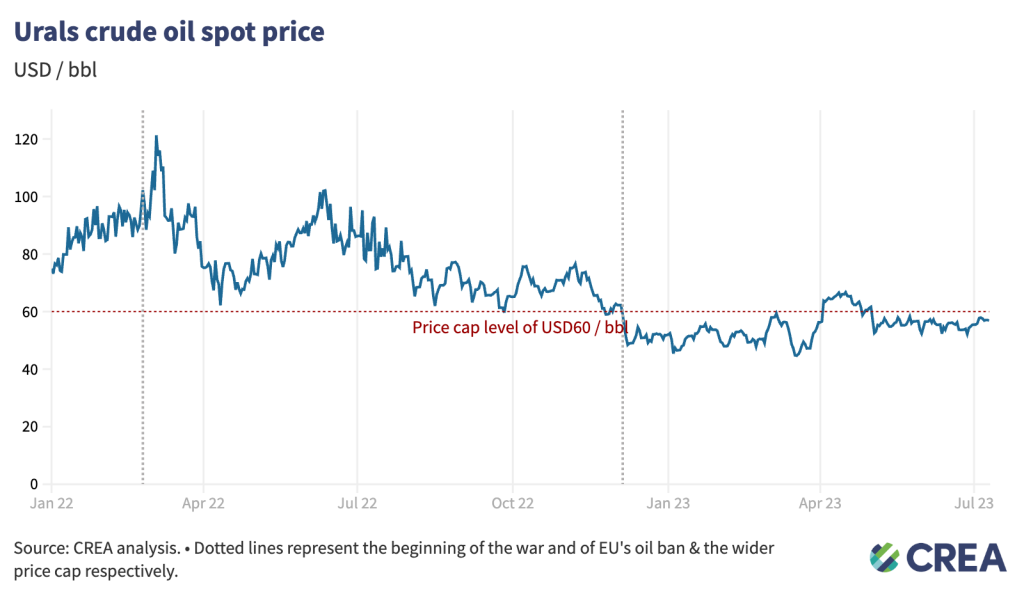

- Urals crude prices remained below the price cap level of USD 60 for the whole of June 2023, after staying stable since they fell in April from prices that were above the price cap level. The East Siberia–Pacific Ocean (ESPO) and Sokol prices, mainly applicable to Chinese and Japanese purchases, remain above the price cap level at around USD 63–68 whilst G7+ owned and / or insured tankers keep lifting Russian oil in Pacific ports.

Relevant reports:

The Russian oil laundromat fueling America’s driving season | Global Witness

| The monthly update on Russian fossil fuel exports and sanctions was prepared by Isaac Levi, Europe-Russia Policy & Energy Analysis Team Lead, CREA; and Hubert Thieriot, Lead Data Scientist, CREA. |

| Note on methodology: From 2023‑04‑03, our monthly snapshot values are no longer seasonally corrected, which may lead to some disparities between the preceding and following reports. We have also adjusted our time frame to show totals since the start of 2023 rather than the start of the invasion. Dates featured are the date the arrival of the shipment was captured by our algorithm. 80% of arrivals for shipments are found within 4 days of the arrival port call in the specific port. For our oil products and chemicals commodity group, please note this contains a wider range of items than just those specified in the current sanctions, as of 2023‑02‑05. More information at: https://energyandcleanair.org/ |