Russian seaborne oil revenues decline for the fourth straight month, but crude oil prices hover above the price cap

By Isaac Levi, Europe-Russia Policy & Energy Analysis Team Lead; Petras Katinas, Energy Analyst; Panda Rushwood, Data Scientist; and Vaibhav Raghunandan, Europe-Russia Analyst and Research Writer

Key findings

- Russia’s monthly fossil fuel export revenues fell by 10% (EUR 70 mn per day) in January 2024 compared to the prior month. Russia’s revenues from fossil fuel exports have been falling steadily since September 2023.

- France’s LNG imports from Russia rose 50% month-on-month despite a drop in total LNG imports. At the same time, gas flows from France to other EU countries increased by 17%, with jumps in exports to Germany (+165%) and Spain (+108%).

- While Turkey’s overall imports of oil products dropped, those from Russia rose 7%. The country’s natural gas imports from Russia also rose by 14% in January due to a surge in demand.

- India’s monthly imports of Russian crude oil dropped for a second straight month. While the country’s total crude import volumes dropped 14%, those specifically from Russia witnessed a steep 19% decline, partly linked to tighter enforcement of sanctions by the US. India has sought to replace this deficit with Iraqi crude.

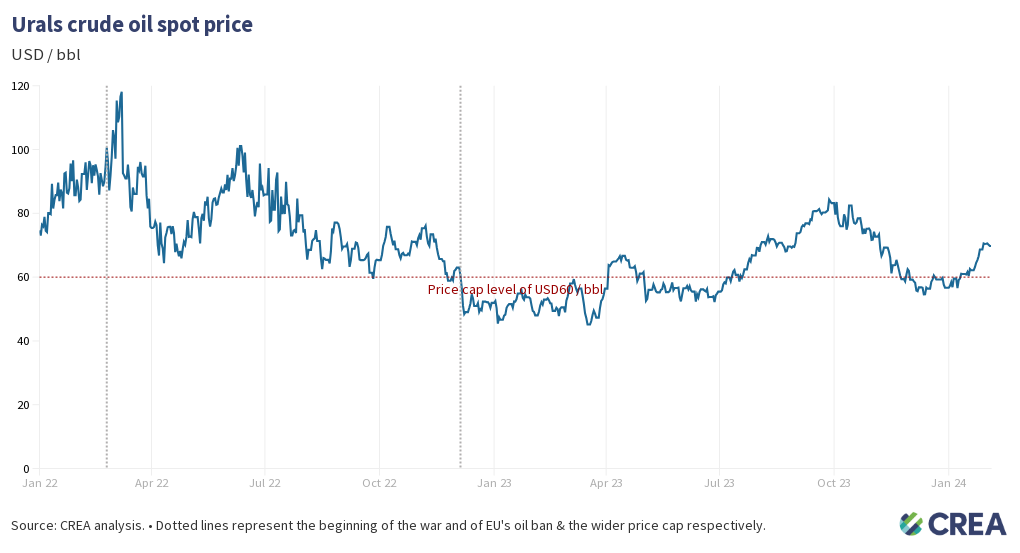

- The average price of Urals and East Siberia Pacific Ocean (ESPO) both rose — 7% and 3% respectively — for the first time in two months. While Urals prices fluctuated around the price cap level (60 USD) for the entire month, ESPO prices remained far above it consistently.

- A price cap of USD 30 per barrel would have slashed Russia’s revenue by EUR 41 bn (25%) since the sanctions were imposed in December 2022 until the end of January 2024. This month alone would have seen a reduction of EUR 2.77 bn or 25 % with a USD 30 per barrel price cap.

- From introducing oil sanctions until the end of January 2024, thorough enforcement of the price cap would have slashed Russia’s revenues by 9% (EUR 14.2 bn). In January alone, full enforcement of the price cap would have cut revenues by 7% (approximately EUR 0.8 bn).

Trends in total export revenue

- In January 2024, Russia’s monthly fossil fuel export revenues saw a month-on-month drop of 10% (EUR 70 mn per day).

- Monthly revenues from crude oil pipelines dropped by 4% (EUR 6 mn per day), while revenues from seaborne crude oil increased 5% (EUR 9 mn per day).

- There was a month-on-month drop of 17% (EUR 38 mn per day) in seaborne oil products.

- Russia’s revenues from LNG exports decreased by 23% (EUR 12 mn per day). At the same time, export revenues from fossil gas via pipeline increased by 23% (21 mn per day).

- Russian revenues from coal exports fell by 26% (EUR 12 mn per day).

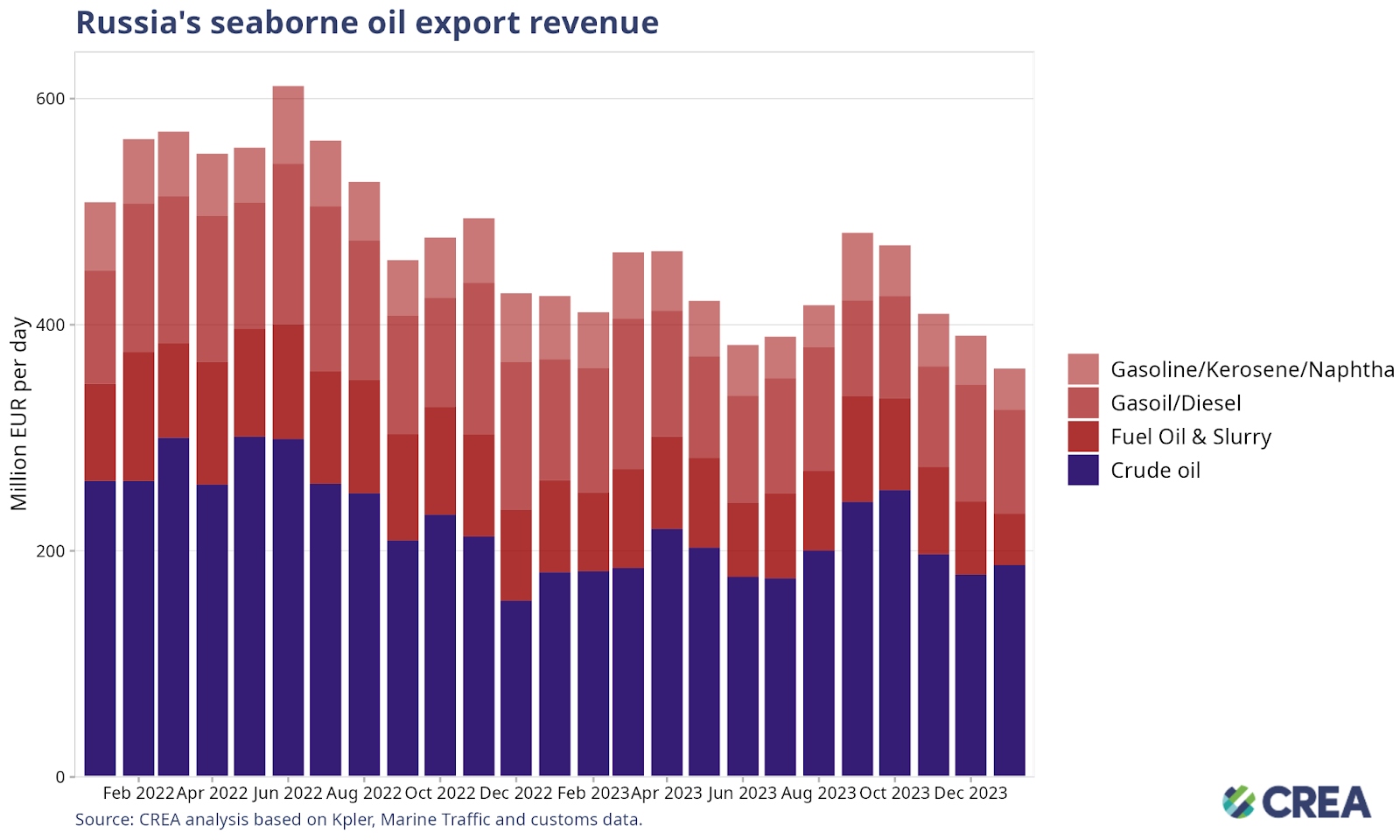

- Russia’s seaborne oil export revenues declined by 7% (EUR 29 mn per day) in January. There was a month-on-month 5% surge in seaborne crude oil export earnings (EUR 9 mn per day).

- In January there was a 29% (EUR 19 mn per day) decrease in Russian earnings from fuel oil and slurry exports.

- Russia’s export earnings from gasoil and diesel decreased by 11% (EUR 12 mn per day).

- Export revenues from gasoline, kerosene, and naphtha decreased by 16% (EUR 7 mn per day).

Who is buying Russia’s fossil fuels?

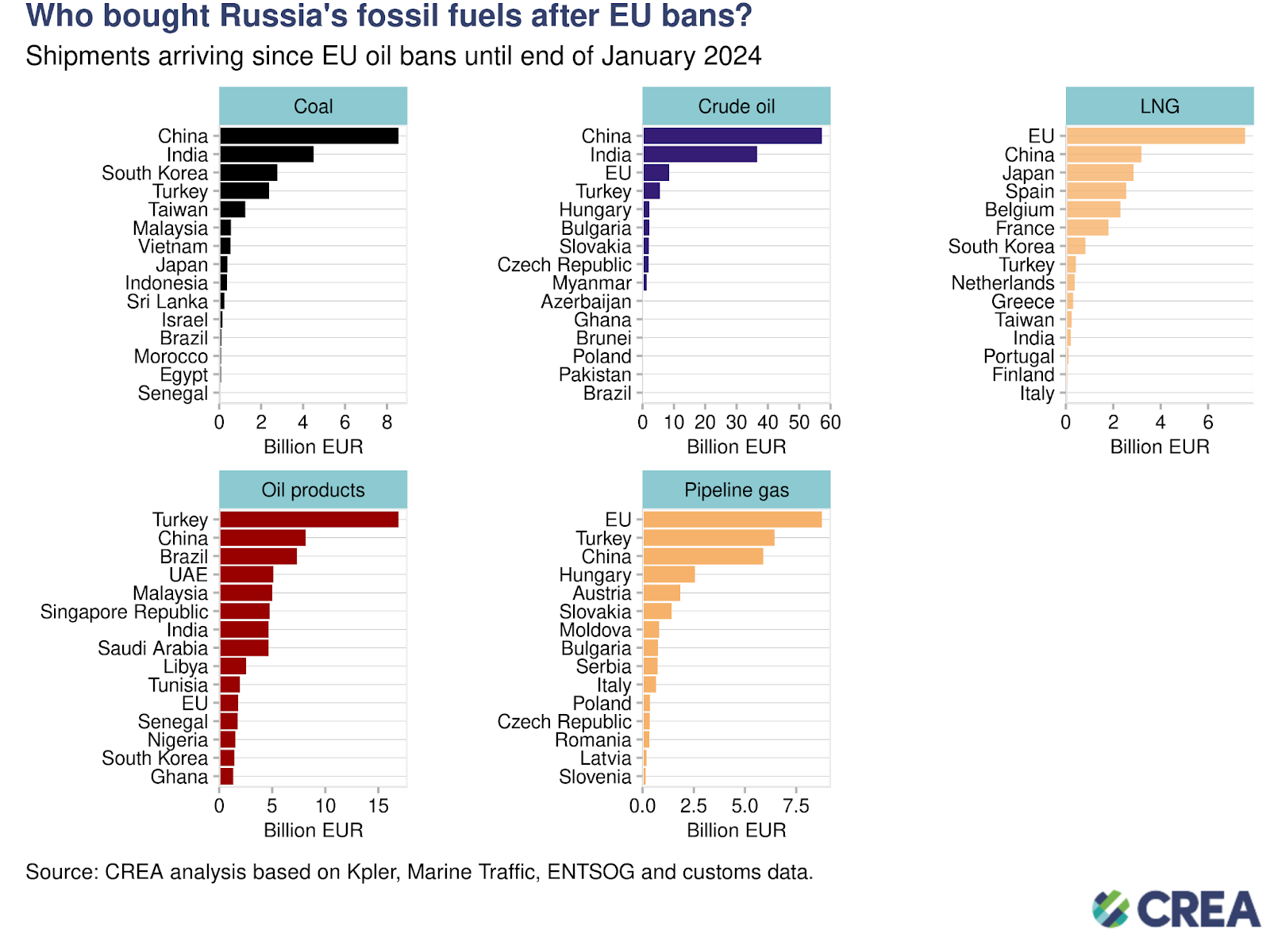

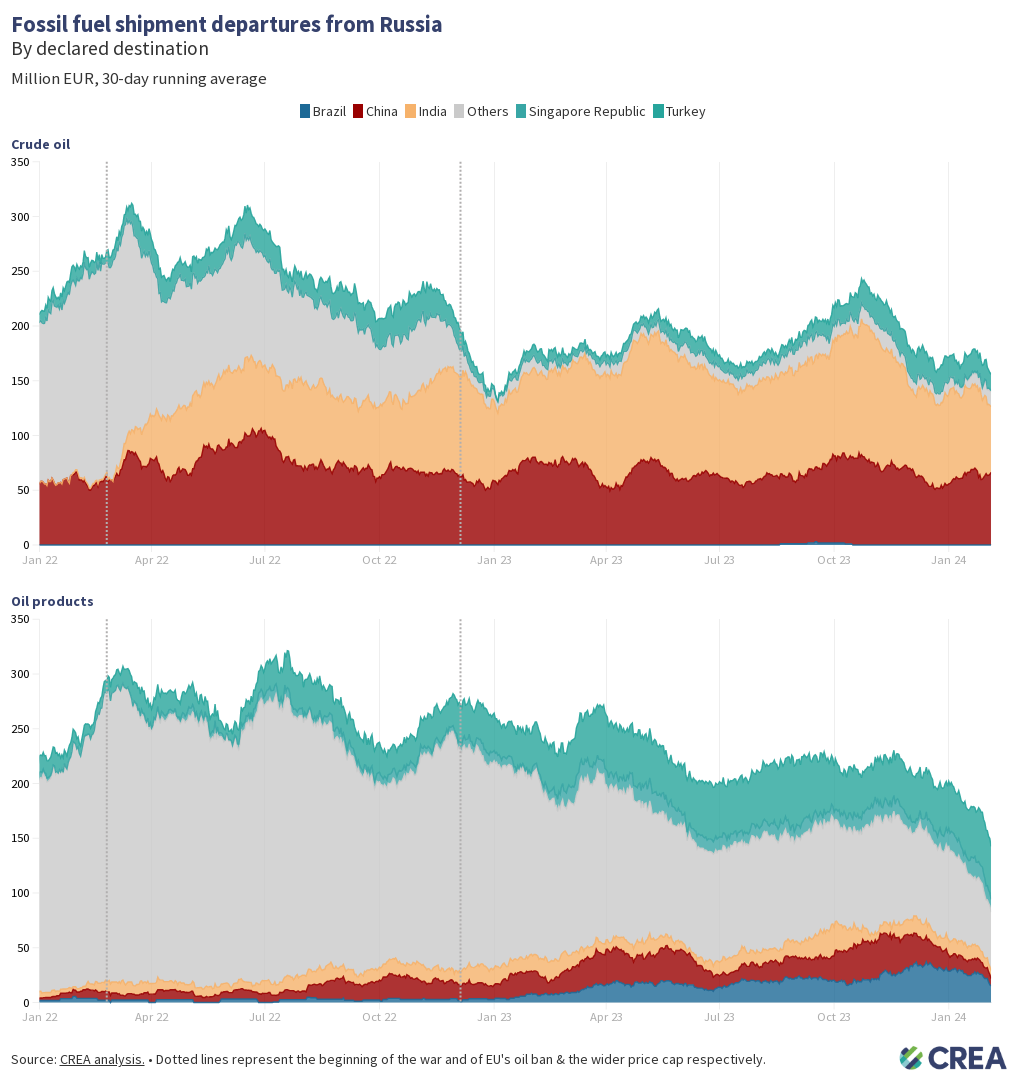

- Coal: China has imported 39% of all Russian coal exports since 5 December 2022. They are followed by India (20%) and South Korea (13%).

- Crude oil: China is the largest buyer of Russian crude oil, purchasing 52%, followed by India (33%), the EU (8%), and Turkey (5%) since the EU’s ban on crude oil from Russia on 5 December 2022. Oil via pipeline is only partially sanctioned. The EU’s crude oil imports have arrived via sea to Bulgaria and via pipeline for the Czech Republic, Slovakia, and Hungary.

- LNG: The EU was the largest buyer, purchasing 50% of Russia’s LNG exports, followed by China (21%) and Japan (19%). No sanctions are imposed on Russian LNG shipments to the EU.

- Oil products: Turkey, the largest buyer, has purchased 24% of Russia’s oil products, followed by China (12%) and Brazil (10%). The EU’s sanctions on seaborne Russian oil products were implemented on 5 February 2023.

- Pipeline gas: The EU was the largest buyer, purchasing 39% of Russia’s pipeline gas, followed by Turkey (29%) and China (26%). No sanctions are imposed on Russian pipeline gas imports into the EU.

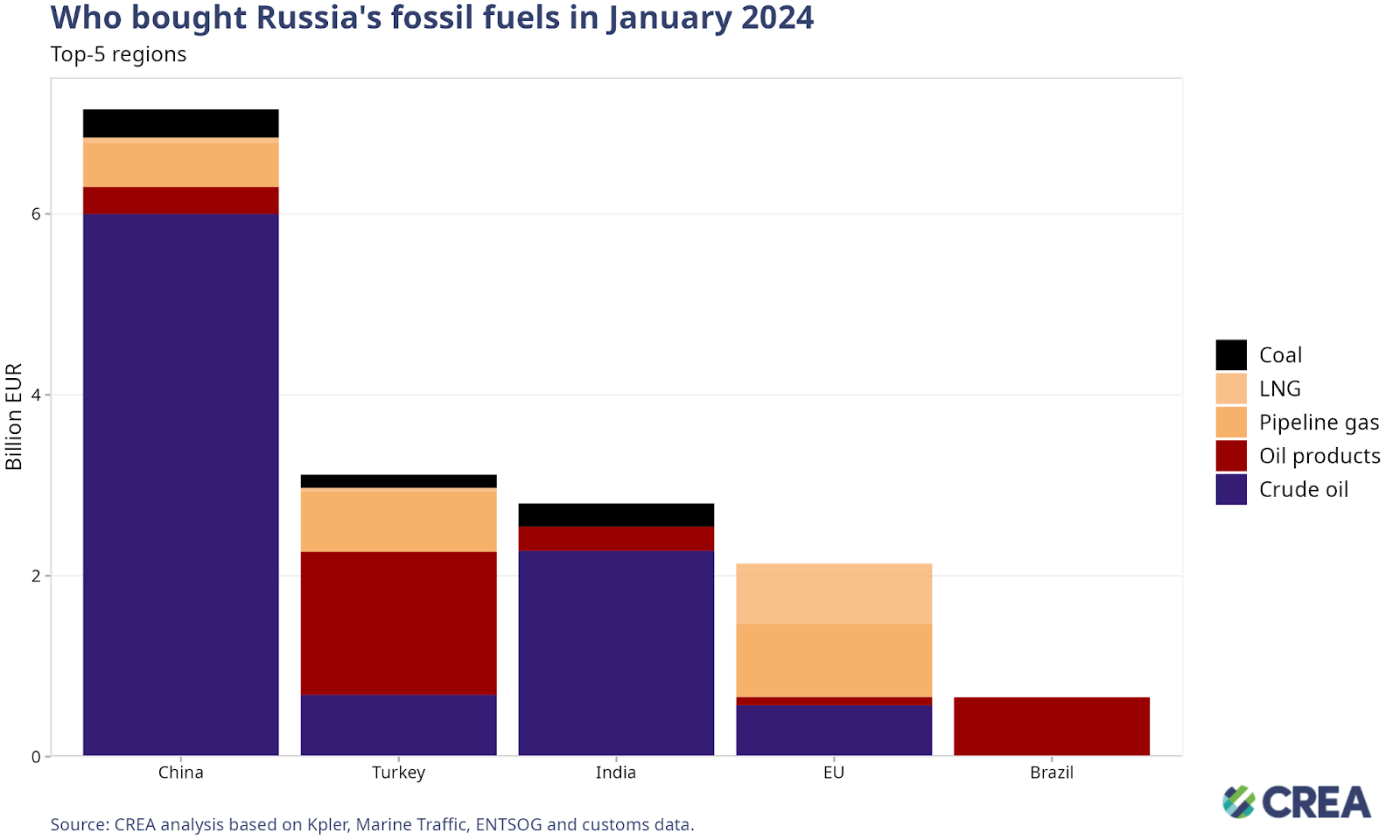

- China was the largest importer of Russian fossil fuels in January, accounting for 33% (EUR 7.1 bn) of total imports. Turkey recorded the second highest imports, accounting for 20% (EUR 3.1 bn), while India was third with an 18% (EUR 2.8 bn) import share. The EU and Brazil contributed 13% (EUR 2.1 bn) and 4% (EUR 0.7 bn) to Russian fossil fuel exports, respectively.

- 84% (EUR 5.9 bn) of China’s total imports were crude oil. Oil products, pipeline gas, and coal comprised 4% (EUR 0.3 bn), 7% (EUR 0.48 bn) and 4% (EUR 0.31 bn), respectively.

- Although China’s total crude oil imports saw an 11% month-on-month decrease, there was a 7% increase in monthly imports of Russian seaborne crude oil. ESPO-grade crude oil is the primary product imported from Russia. Despite a 19% decrease in total monthly oil product imports, flows from Russia saw a steeper decline of 26%.

- Turkey’s total imports from Russia consisted of oil products (51% worth EUR 1.6 bn), crude oil (22% worth EUR 0.7 bn), pipeline gas (22% worth EUR 0.7 bn), and coal (5% worth EUR 0.15 bn).

- In January, Turkey’s overall imports of petroleum products dropped by 4%, but imports from Russia increased by 7%. Turkey was the largest global importer of oil products from Russia in January. Conversely, Turkey’s crude oil imports from Russia decreased by 17%, contributing to an overall 27% decrease in total crude oil imports.

- Turkey’s natural gas imports from Russia saw a 14% month-on-month increase in January. This surge correlates with a seasonal rise of 14% in natural gas consumption, as January is a period of peak seasonal demand in Turkey.

- Crude oil accounted for 82% (EUR 2.3 bn) of India’s total fossil fuel imports from Russia. Oil products accounted for 10% (EUR 0.3 bn), and coal accounted for 9% (EUR 0.2 bn) of their total imports in December.

- India’s monthly volume of crude oil imports decreased by 14%, with imports of Russian crude oil declining by 19%. India’s crude oil imports from Russia fell for a second consecutive month. Despite this decline, India remains the top buyer of seaborne Russian crude.

- The EU’s total imports of fossil fuels from Russia comprised 38% (EUR 0.8 bn) of pipeline gas, 31% (EUR 0.7 bn) of LNG, 27% (EUR 0.6 bn) of crude oil, and 4% (EUR 0.09 bn) of oil products.

- In January, Brazil’s Russian fossil fuel imports comprised oil products valued at EUR 0.7 bn. The volume of petroleum products from Russia decreased by 12%, while total monthly imports increased by 24%. Despite the decrease, Russian oil products still accounted for 32% of Brazil’s total imported refined products.

- Landlocked Central and Eastern European countries and some Southern European countries received Russian fossil gas via pipeline through Ukraine and TurkStream in January 2024. Crude oil was obtained via the Druzhba oil pipeline. The EU has not banned fossil gas and crude oil via pipelines.

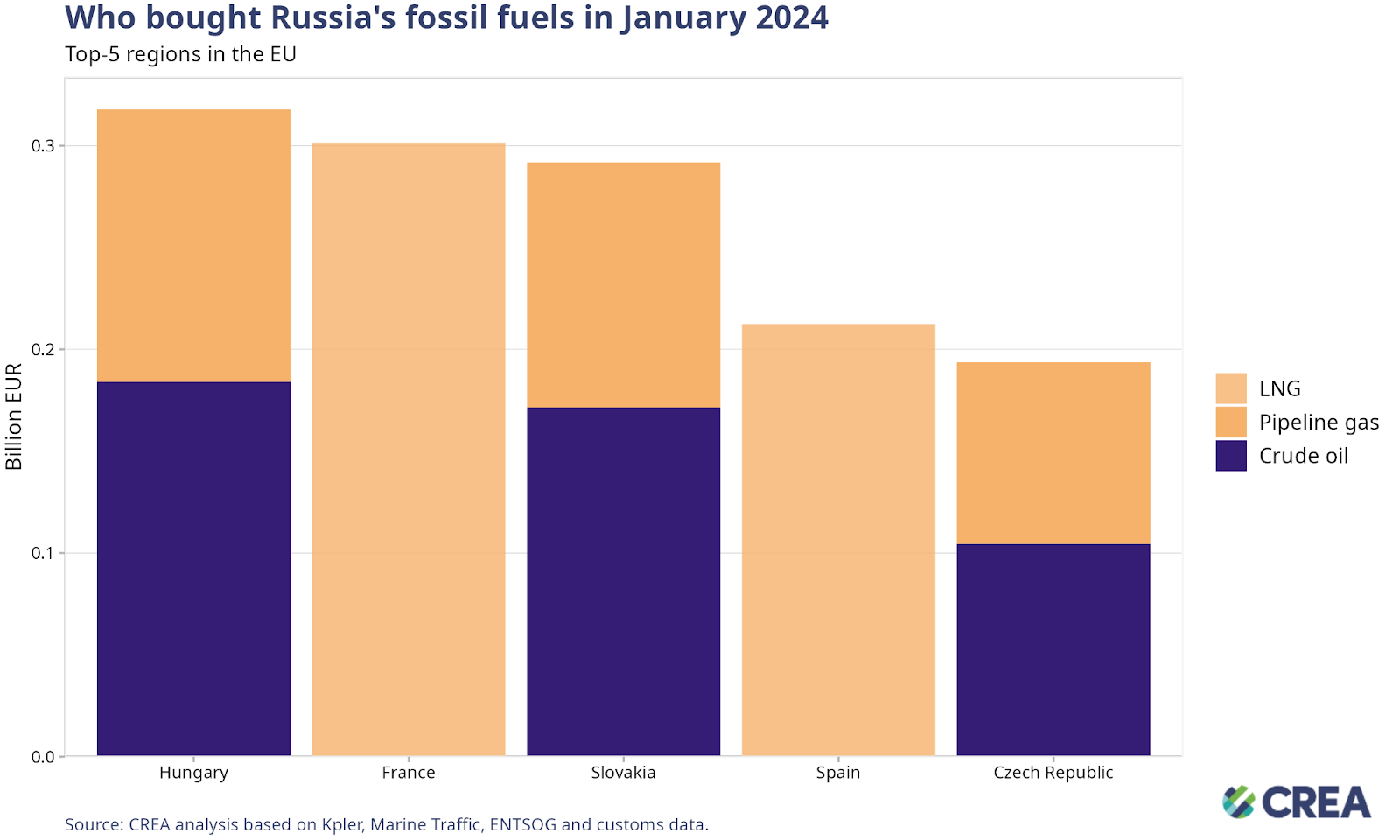

- Hungary was the largest importer of Russian fossil fuels within the EU in January, importing fossil fuels worth EUR 317 mn. Imports comprised crude oil and gas, delivered via pipelines, valued at EUR 184 mn and EUR 133 mn, respectively. Imported pipeline gas from Russia in fact fell 18% in volume terms in January compared to the prior month. However, Hungary increased its gas consumption in January which can be explained by the rise in gas withdrawals from the Underground Gas Storage (UGS), which saw a 40% increase in January compared to the previous month.

- France’s total imports from Russia, amounting to EUR 301 million, consisted entirely of LNG. Despite the total volume of LNG imports to France decreasing by 8%, overall imports, specifically from Russia, surged by 50%. This notable increase can be attributed to heightened seasonal gas consumption, especially in the public distribution sector, which saw an 18% month-on-month increase. Additionally, there was a rise in France’s monthly gas exports, which were up by 17%. Notably, there was a significant increase in gas flows from France to Germany (+165%) and Spain (+108%).

- Slovakia imported crude oil and pipeline gas from Russia valued at EUR 184 mn and EUR 133 mn, respectively. Gas volumes from Russia to Slovakia decreased by 7%. Notably, Slovakia sends more than 50% of its gas imports to Austria.

- Spain imported EUR 212 mn worth of LNG from Russia. The monthly volume of LNG imports to Spain increased by 28%, while imports from Russia remained at the same level as the previous month. The rise was due to increased gas consumption, primarily driven by industrial usage.

- The Czech Republic was the EU’s fifth-largest importer of Russian fossil fuels, importing EUR 104 mn of crude oil and EUR 0.89 mn of pipeline gas.

- In January, the port of Sikka in India was the foremost destination for Russian fossil fuels. The port imported EUR 705 mn worth of Russian fossil fuels of which 62% (EUR 403 mn) was crude oil and 38% (EUR 267 mn) was oil products.

- The port of Singapore was the second-highest importer of Russian fossil fuels, of which 93% (EUR 483 mn) were oil products, and 7% (EUR 0.38 mn) were crude oil.

- China’s port of Dongying was the third-largest importer of Russian fossil fuels (EUR 378 mn), of which 96% (EUR 364 mn) was crude oil, and the remaining imports were oil products (EUR 0.14 mn).

- The port of Mersin in Turkey was the fourth highest destination, importing Russian fossil fuels valued at EUR 339 mn. Oil products accounted for 95% (EUR 324 mn), and coal for 5% (EUR 0.15 mn).

- Dongjiakou in China was the fifth largest port importing Russian fossil fuels valued at EUR 297 mn. Crude oil accounted for 90% (EUR 269 mn), LNG 9 % (EUR 0.27 mn), and coal for a minor EUR 0.01 mn.

How are oil prices changing?

- In January, the average Urals Europe cost and freight (CFR) spot price was USD 64.45 per barrel, a 7% increase compared to December.

- The prices for the East Siberia Pacific Ocean (ESPO) and Sokol blends, primarily associated with Asian markets, rose 3% in January — the first surge in two months. The average price for ESPO was USD 75.37 per barrel in January.

- Urals prices fluctuated around the specified price cap level (60 USD) for the entire month, and ESPO prices remained far above the price cap.

- Throughout this period, vessels owned or insured by the G7 and European countries continued to load Russian oil in all Russian port regions. These cases call for further investigation for breach of sanctions.

Russia remains highly reliant on the European and G7 shipping industry

- In January, 50% of Russian oil and its products were transported by tankers subject to the oil price cap. The remainder was shipped by ‘shadow’ tankers and was not subject to the price cap policy.

- 64% of Russian crude oil was transported by ‘shadow’ tankers, while tankers owned or insured in countries implementing the price cap accounted for 36%.

- ‘Shadow’ tankers transporting oil products, chemicals, and LPG handled 37% of the total volume of products. The remaining volume was shipped by tankers subject to the price cap policy.

- Tankers in the Pacific region were loaded with Russian oil at ports like Kozmino in Russia, where the ESPO pipeline ends and is connected to a refinery. Here, the ESPO crude oil grade is exported at prices exceeding the cap.

- Russia’s reliance on EU/G7 owned or insured vessels provides the Price Cap Coalition with adequate leverage to lower the price cap and implement better monitoring and enforcement that would considerably lower Russia’s oil export revenues.

How can Ukraine’s allies tighten the screws?

- Russia’s fossil fuel export revenues have fallen since sanctions were implemented, showing their impact on lowering Putin’s ability to fund the war. However, much more should be done to limit Russia’s export earnings and constrict the Kremlin’s war chest. This includes lowering the oil price cap, increasing monitoring and enforcement of sanctions, and banning unsanctioned fossil fuels such as LNG and pipeline fuels that are legally allowed into the EU.

- Measures must be taken by sanctioning countries to prevent Russia’s growth in ‘shadow’ tankers immune to the oil price cap policy. Sanction-imposing countries should ban the sale of old tankers to registered owners in countries that do not implement the oil price cap policy. This would help limit the growth of the ‘shadow’ tankers we have observed since Russia invaded Ukraine.

- A price cap of USD 30 per barrel (still well above Russia’s production cost that averages USD 15 per barrel) would have slashed Russia’s revenue by EUR 41 bn (25%) since the sanctions were imposed in December 2022 until the end of January 2024. This month alone would have seen a reduction of EUR 2.77 bn or 25% with a USD 30 per barrel price cap.

- Lowering the price cap would be deflationary, reducing Russia’s oil export prices and inducing more production from Russia to make up for the drop in revenue.

- Since introducing sanctions until the end of January, thorough enforcement of the price cap would have slashed Russia’s revenues by 9% (EUR 14.2 bn). In January alone, full enforcement of the price cap would have slashed revenues by 7% (approximately EUR 0.8 bn).

- Enforcement agencies overseeing the sanctions must take proactive measures against violating entities, including insurers registered in price-cap coalition countries, shippers, and vessel owners.

- Despite clear evidence of violation, there must be more information on enforcement agencies implementing penalties against shippers, insurers, or vessel owners in the public domain. Penalties against violating entities increase the perceived risk of being caught.

- The Office of Foreign Assets Control (OFAC) should continue sanctioning vessels that look to have violated the price cap policy. Other enforcement agencies, such as the Office of Financial Sanctions Implementation (OSFI), should ramp up investigations of entities that appear to have violated sanctions.

- Penalties for those guilty of violating the price cap must be significantly harsher. Current penalties include a 90-day ban of vessels from securing maritime services after violating the price cap, a mere slap on the wrist. Vessels should be fined and banned in perpetuity if found guilty of violating sanctions.

- The lack of proper monitoring and enforcement and rising oil prices have increased Russia’s export revenues to fund its war against Ukraine.

Relevant reports:

- Gas addicted Europe trades one energy risk for another

- UK imports EUR 660 of oil produced from Russian crude

- UK insurance responsible for transporting EUR 46.4 bn of Russian oil

- EU CO2 from fossil fuels drop 8% to reach lowest levels in 60 years

- India will be the biggest driver of oil demand growth between 2023-30

| The monthly update on Russian fossil fuel exports and sanctions was prepared by Isaac Levi, Europe-Russia Policy & Energy Analysis Team Lead, CREA; Petras Katinas, Energy Analyst; Panda Rushwood, Data Scientist; and Vaibhav Raghunandan, Europe-Russia Analyst and Research Writer. |

| Note on methodology: Update 2023-10-19 – We now use Kpler to estimate seaborne exports from Russia and other countries. This change increases our tracker’s estimate of exports from Russia to the world by EUR 77.8 bn (+18% increase) and the exports to the EU by EUR 12.4 bn (+2.8% increase). We have also changed how we receive protection and indemnity (P&I) insurance information about ships to additionally attain data from known P&I providers directly as well as from Equasis. This is to make sure that we have recorded the correct start date for a ship’s insurance. Find out more details on the changes in our methodology that are explained in our article about the migration from automatic identification system (AIS) data providers to the Kpler dataset. |